Easing headwinds clear the way to new highs

Key Takeaways:

- Three major headwinds have eased: Improving confidence in AI demand, lower oil prices, and reduced fears of additional Fed tightening have helped the S&P 500 break out of its three-month trading range and reach new highs.

- Earnings continue to support the bull market: Second-quarter earnings growth is tracking near 48%, and nearly 29% even after adjusting for investment-related gains at Alphabet and Amazon. Importantly, earnings strength is broadening beyond mega-cap technology companies.

- Economic resilience remains intact: Manufacturing activity accelerated to a four-year high despite July's oil-price spike, while slower wage growth and a cooling labor market suggest inflation pressures remain contained.

- New highs are not necessarily a warning sign: Historically, investing at all-time highs has produced returns comparable to, and often better than, investing on a typical trading day, helping reinforce the importance of staying invested rather than waiting for a better entry point.

Over the past three months, three key headwinds have kept the market rangebound: skepticism around the sustainability of AI spending, geopolitical risks tied to energy markets, and uncertainty surrounding Federal Reserve policy. Recent developments have helped ease at least two of those concerns, allowing earnings and economic fundamentals to reassert themselves as the primary drivers of stock prices. As a result, the S&P 500 has broken out of its summer consolidation and moved to new record highs. We examine what's behind August's strong start and what the market's breakout says about the durability of the current bull market.

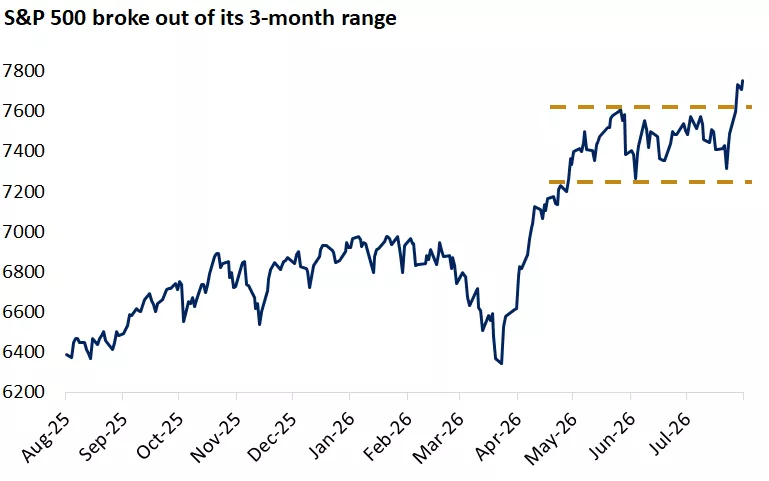

The graph shows the S&P 500 over the past year. After being in a range over the past three months, stocks broke out to new highs in August.

The graph shows the S&P 500 over the past year. After being in a range over the past three months, stocks broke out to new highs in August.

Big tech earnings show no signs of slowing AI demand

The most important debate facing markets in recent months, in our view, has been whether AI-related spending can continue at its current pace and ultimately generate sufficient returns. Investors have raised legitimate questions about capital spending sustainability, monetization timelines, emerging competition, and the possibility that AI adoption may fall short of increasingly elevated expectations. Those concerns contributed to a valuation reset across parts of the technology and semiconductor complex during the summer.

While some of these questions will likely continue to linger, recent earnings reports pushed back on many of the concerns. Large technology companies reported accelerating cloud revenue growth, rising AI demand, expanding order backlogs, and increasing visibility into future revenue streams. Perhaps most importantly, in our view, management teams are becoming more confident discussing not only the scale of their AI investments, but also the economic returns those investments are expected to generate.

Market reactions have reflected this distinction. Companies demonstrating accelerating revenue growth and a clearly articulated path to returns on invested capital have generally been rewarded. Microsoft, for example, added roughly $450 billion in market value following its earnings report, the largest single-day market capitalization gain ever recorded by a public company.

By contrast, companies continuing to ramp spending without a clear monetization path have received a more mixed response. Meta shares, for example, declined following earnings despite another quarter of strong growth, as investors debated whether accelerating investment spending would ultimately translate into sufficient returns. The differing market reactions suggest that the AI story is maturing rather than breaking. We believe investors are becoming more selective, but they are not abandoning the theme.

The bottom line: We believe recent earnings results helped renew confidence in the AI investment cycle. Accelerating cloud growth and expanding backlogs point to an AI cycle that remains intact. At the same time, the unwinding of crowded positioning and the valuation reset experienced earlier this year have helped create a better backdrop for tech. In our view, that combination leaves room for valuations to gradually expand as investors gain greater confidence in the durability and monetization of future AI-driven growth.

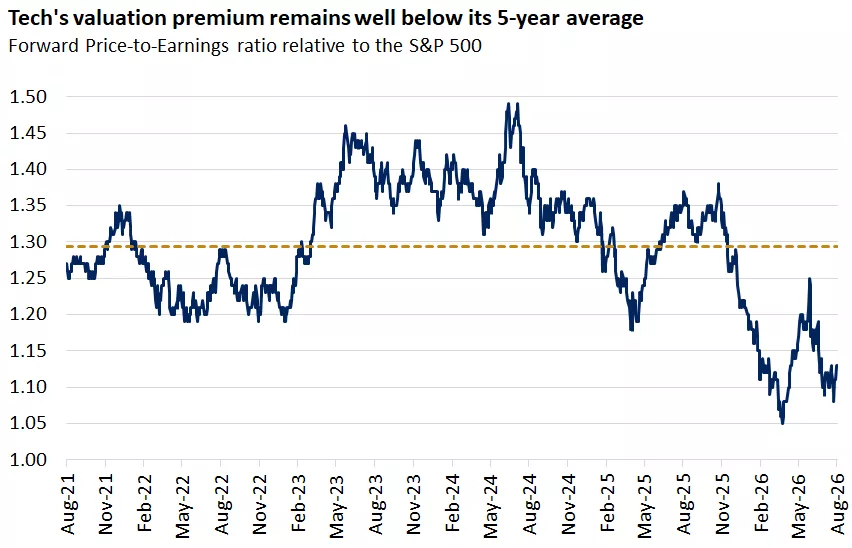

The graph shows that the forward price-to-earnings ratio of the tech sector relative to the broader S&P 500 is below its five-year average.

The graph shows that the forward price-to-earnings ratio of the tech sector relative to the broader S&P 500 is below its five-year average.

It's not just tech driving outsized S&P 500 profit growth

With more than 85% of S&P 500 companies having reported second-quarter results, earnings growth is tracking roughly 48%, more than double the 24% estimate at the start of earnings season and one of the strongest reporting periods outside of major post-recession recoveries. While consumer discretionary and communication services have contributed significantly to the upside surprise, profit growth is becoming increasingly broad-based, with six of the remaining nine sectors also delivering double-digit earnings growth.

Importantly, the strength extends beyond a handful of headline-grabbing results. Reported earnings growth was boosted by sizable investment-related gains at Alphabet and Amazon, primarily reflecting mark-to-market gains on strategic equity investments, including their Anthropic holdings. Excluding those non-operating gains, S&P 500 earnings growth would still be tracking close to 29%. That would represent an acceleration from the first quarter and the second consecutive quarter of earnings growth above 20%.

The bottom line: We believe the market's move to new highs is being confirmed by an exceptionally strong earnings season. Earnings growth is broadening beyond a narrow group of mega-cap technology companies, helping provide a healthier foundation for further gains and supporting our view that market leadership can continue to widen in the second half of the year.

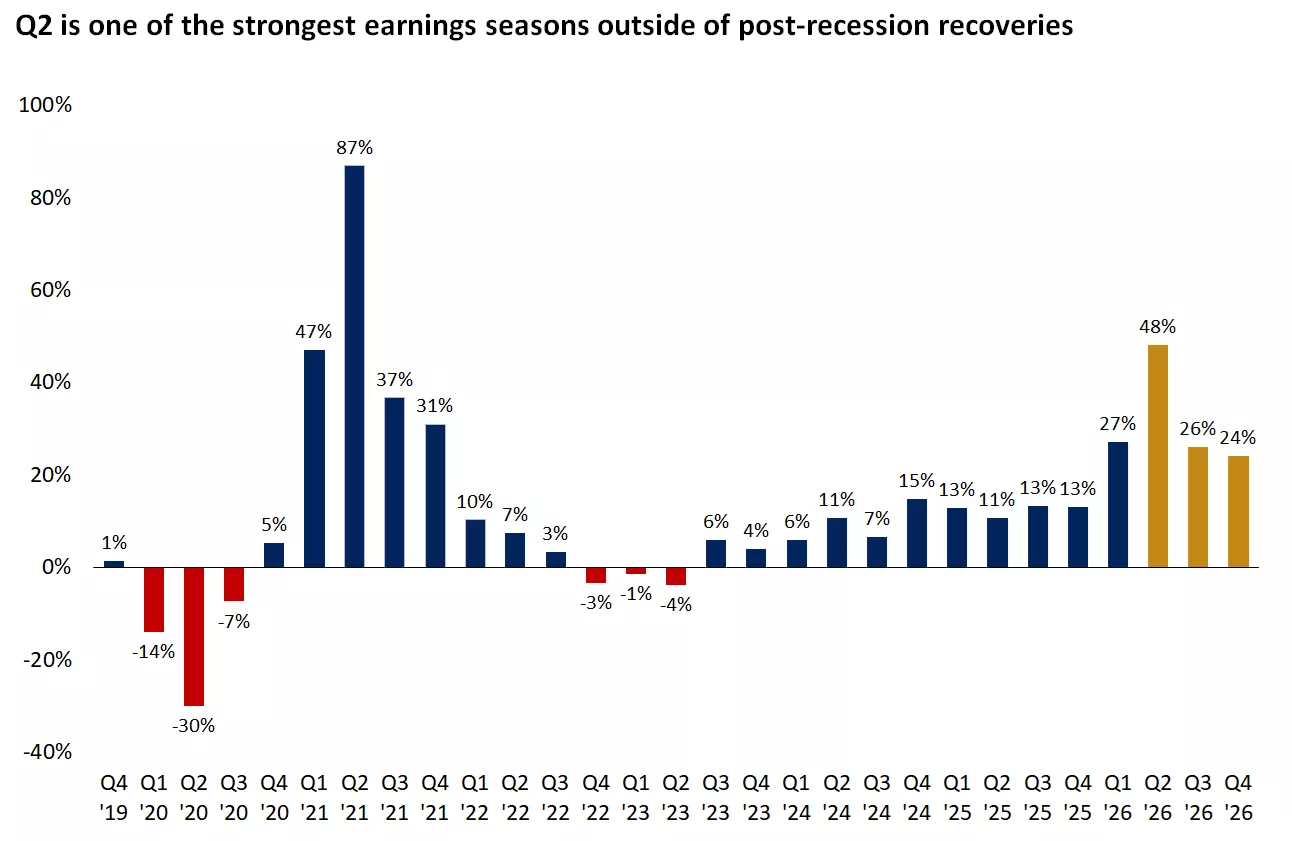

The graph shows that the second quarter earnings season is shaping up to be one of the strongest outside of post-recession recoveries.

The graph shows that the second quarter earnings season is shaping up to be one of the strongest outside of post-recession recoveries.

The economy proves resilient despite oil volatility

Geopolitical risks in the Middle East have not disappeared, but recent headlines have helped reduce fears of a major energy supply disruption. Reports of ongoing discussions surrounding access to the Strait of Hormuz have fueled hopes that tensions could de-escalate, prompting a reversal in oil prices. WTI crude has retraced a good portion of last month's surge as investors assign a lower probability to the most adverse outcomes. While negotiations remain fluid, markets appear to have become less sensitive to headlines and more focused on underlying fundamentals.

Even through July's oil price spike, the economy has continued to demonstrate resilience. Manufacturing activity accelerated last month, with the ISM Manufacturing Index rising to its highest level in more than four years as demand strengthened, production increased, and hiring improved. We think evidence of a strengthening industrial backdrop can also be seen in recent railroad earnings, a rebound in heavy truck sales, and Caterpillar's strong earnings results, which reflect both the ongoing AI infrastructure buildout and an accelerating manufacturing cycle.

The bottom line: The situation surrounding Iran and the Strait of Hormuz remains fluid, but the perceived risk of a major energy disruption has eased, in our view. Combined with resilient economic data and improving manufacturing activity, the reversal in oil prices has helped remove an important source of uncertainty that weighed on markets during much of the summer.

The graph shows that manufacturing activity as proxied by the ISM manufacturing PMI has been accelerating this year.

The graph shows that manufacturing activity as proxied by the ISM manufacturing PMI has been accelerating this year.

The labor market is not a source of inflation

July's employment report painted a picture of a labor market that is cooling rather than overheating. Payrolls declined by 23,000 jobs, well below expectations for an 80,000-job increase, while sizeable downward revisions to the prior two months suggest labor demand has been softer than previously believed. Meanwhile, the decline in the unemployment rate to 4.1% should not be interpreted as a sign of labor-market strength, in our view. Instead, it largely reflects a drop in labor force participation, which has fallen to its lowest level since 2021 amid slower immigration, an aging population and retirements.

Despite the weak headline figures, stocks rallied following the report in a classic "bad news is good news" reaction. The softer labor-market data, combined with the slowest pace of wage growth in nearly five years, helped alleviate inflation concerns. As a result, investors have scaled back expectations for Fed tightening, with bond markets now assigning less than a 50% probability of a rate hike in September. That said, we believe upcoming inflation data will likely play an even more important role in shaping expectations for the Fed's next move.

The bottom line: Uncertainty around the path of monetary policy remains, but additional rate hikes are far from inevitable, in our view. The latest jobs data reinforce our view that the labor market is stuck in the slow lane, characterized by low hiring and low firing. That environment may not feel particularly strong, but we see it as consistent with continued economic expansion, and it does not appear to be generating meaningful inflation pressure.

Is buying at all-time highs a risky proposition?

Over the past three months, markets have successfully absorbed several key headwinds, as strong earnings growth offset many of the risks that dominated investor conversations earlier this summer. Rather than triggering a broader correction, those concerns led to a healthy rotation beneath the surface. Financials, healthcare, and energy assumed leadership while growth sectors paused. More recently, strong tech earnings have sparked another rotation, with growth stocks helping propel the S&P 500 to fresh highs. We expect these shifts in leadership to continue.

Reaching an all-time high can leave investors wondering whether it is still a good time to put money to work. While pullbacks can occur at any time, history suggests that new highs have not typically been poor entry points. Average forward three-month returns have been slightly lower when investing at an all-time high, but the gap largely disappears over six months. Over one-, three-, and five-year horizons, average returns have actually been higher following all-time highs than when investing on a typical trading day. In our view, the lesson is that new highs often occur because fundamentals are improving, not because a market advance is ending. As a result, time in the market has historically mattered more than waiting for a perfect entry point.

The bottom line: We believe the durability of earnings growth remains the key pillar supporting markets. The economy continues to demonstrate resilience, manufacturing activity is accelerating, and market leadership is broadening. In this environment, we believe investors should avoid becoming overly concentrated in any single theme, keeping in mind their risk tolerance and investment goals. For cyclical exposure, we favor mid-caps, industrials, and international value-oriented investments. For AI exposure, we continue to prefer communication services and emerging market equities, while expecting leadership rotations both within and beyond technology as the bull market progresses.

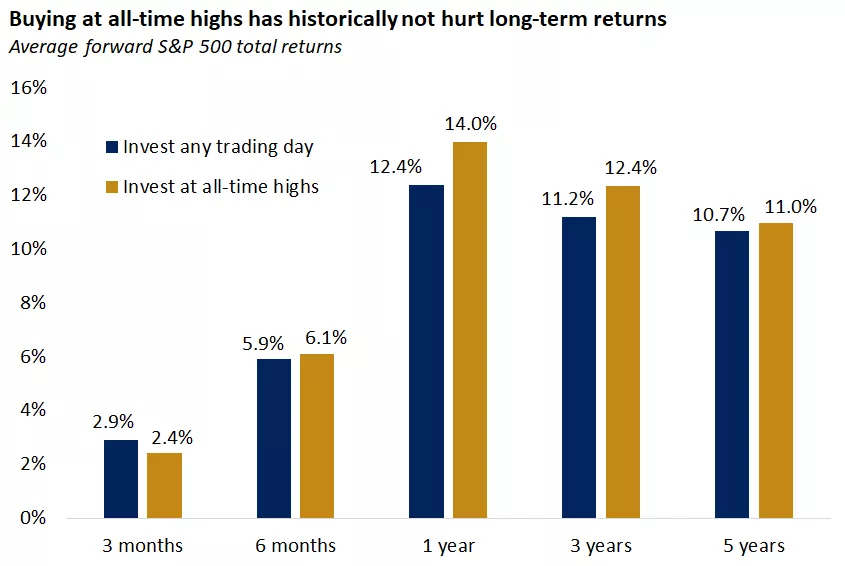

The graph shows forward S&P 500 returns of investing at all-time highs vs. any trading day. History suggests that new highs have not typically been poor entry points. Returns over 3- and 5-year periods are annualized.

The graph shows forward S&P 500 returns of investing at all-time highs vs. any trading day. History suggests that new highs have not typically been poor entry points. Returns over 3- and 5-year periods are annualized.

Angelo Kourkafas, CFA

Senior Global Investment Strategist

Sources for all data in commentary: Bloomberg, FactSet

Angelo Kourkafas

Angelo Kourkafas is responsible for analyzing market conditions, assessing economic trends and developing portfolio strategies and recommendations that help investors work toward their long-term financial goals.

He is a contributor to Edward Jones Market Insights and has been featured in The Wall Street Journal, CNBC, FORTUNE magazine, Marketwatch, U.S. News & World Report, The Observer and the Financial Post.

Angelo graduated magna cum laude with a bachelor’s degree in business administration from Athens University of Economics and Business in Greece and received an MBA with concentrations in finance and investments from Minnesota State University.

Previous weeks' weekly market wraps

7/31: Fed and tech earnings take center stage

Important Information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.