Uncertainty rarely signals an all-clear, and markets don't wait

What you need to know

- July delivered mixed market returns as investors navigated a range of crosscurrents in the economic, policy, and market backdrop.

- Uncertainty rarely signals "all clear" before markets move higher, as demonstrated by widespread 12-month gains, with multiple indexes hitting record highs along the way.

- Rather than position for a single economic or market outcome, prioritize broad diversification to participate in rotating opportunities.

- Amid solid economic momentum, we remain constructive on equities, favoring overweight allocations to a blend of U.S. stocks, emerging markets, and cyclical market segments.

Portfolio tip

Start portfolio reviews with the end in mind. A goals-based approach helps you create a diversified portfolio strategy to help you navigate markets today and stay on course as conditions shift.

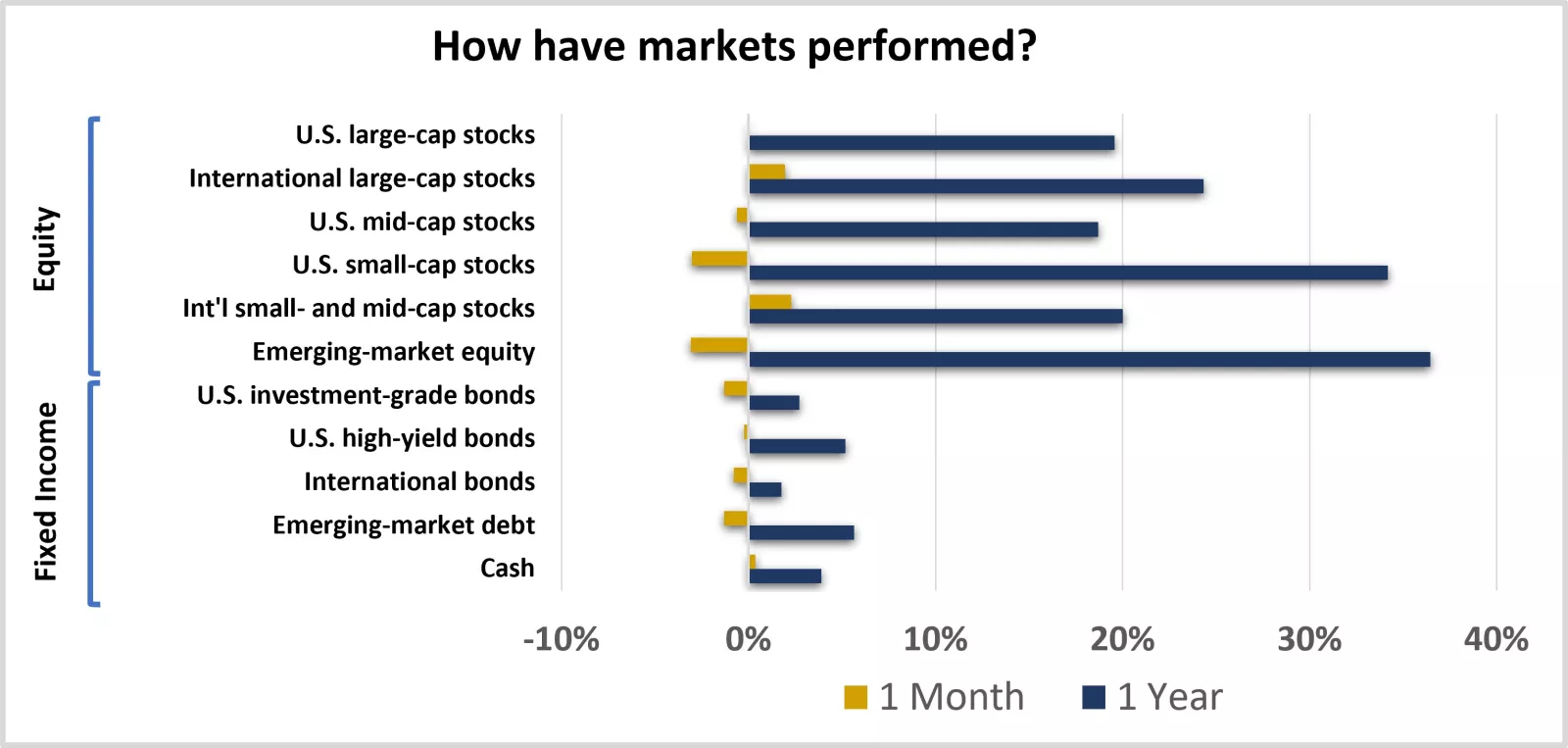

This chart shows the performance of equity and fixed-income markets over the previous month and year.

This chart shows the performance of equity and fixed-income markets over the previous month and year.

Where have we been?

July delivered mixed stock market returns as investors navigated a range of crosscurrents in the economic, policy, and market backdrop. On the one hand, economic data remained broadly constructive, indicating U.S. growth moderated but continued at a healthy pace, supported by solid consumer spending and steady labor markets. Corporate earnings also continued to demonstrate strength, helping underpin stock markets.

At the same time, risks tied to geopolitical developments, evolving trade policies, and the speed of investment in artificial intelligence clouded the outlook. In addition, higher energy prices, tariffs, and AI demand fueled concerns that inflationary pressures could persist, weighing on markets.

Tech-heavy market segments were among the hardest hit, but returns were not uniformly negative across asset classes and sectors. International developed-market stocks outperformed from an asset class perspective, delivering slightly positive returns. At the sector level, a combination of cyclical and defensive sectors also posted gains, with financials, energy, health care, and real estate among the strongest performers, demonstrating a broadening theme as leadership expanded beyond tech.

Interest rates moved higher, weighing on bond allocations. Interest rates have risen across the maturity spectrum this year, a trend that continued in July.

Persistent inflationary pressures and resilient economic growth have driven longer-term yields higher, with the 10-year Treasury yield moving from around 4.2% at the start of the year to around 4.75% in July. The shorter end of the maturity spectrum has reflected an increasing likelihood that the Fed may need to hike rates to combat inflation, lifting the 2-year yield from 3.5% to around 4.25% over the same period.

Higher yields weighed on fixed income markets, as rising interest rates typically result in lower bond prices. As a result, most bond asset classes fell in July, leaving cash to stand out as the only asset class to deliver a positive return.

Over the past year, resilient economic fundamentals have outweighed persistent uncertainty, with markets delivering solid gains across asset classes. Inflation pressures, shifting Federal Reserve policy expectations, tariffs, and geopolitical tensions have all tested investor sentiment over the past 12 months, creating a persistent wall of worries. Despite these concerns and periodic market weakness, returns over the period were broadly positive.

Resilient economic growth, healthy consumers, rising corporate earnings, and continued AI-driven investment provided a strong boost. The result has been solid, broad-based gains across stock and bond markets, with some markets hitting multiple record highs along the way, reinforcing the value of staying disciplined and diversified through changing market conditions.

What do we recommend going forward?

Even when things feel uncertain, stay diversified and keep the end goal in mind. While headlines continue to evolve, this year has reinforced a familiar lesson: uncertainty rarely provides an all-clear signal before markets move higher. Rather than positioning portfolios for a single economic or market outcome, start portfolio reviews with your goals in mind, then prioritize diversification to capture rotating opportunities.

Your objectives should shape your portfolio's stock and bond mix. From there, our strategic asset allocation guidance can help you build a diversified portfolio aligned with your desired outcomes. While diversification does not guarantee a profit or protect against loss in declining markets, spreading allocations across regions, market capitalizations, maturities, and credit qualities can help mitigate risk, reduce concentration in any single market or theme, and keep you aligned with your objectives as conditions shift.

Amid solid economic momentum, we remain constructive on equities, favoring overweight allocations to a blend of market segments. Geopolitics and evolving central bank monetary policies are likely to remain sources of periodic volatility, but pullbacks may offer an opportunity to buy quality investments at more attractive prices. We expect steady economic momentum, healthy consumer spending, rising corporate profits, and the transformative growth driven by the AI buildout to provide a favorable backdrop for stocks.

For investors looking to deploy excess cash or rebalance their portfolio, we believe a mix of opportunities awaits. Consider overweight allocations to:

- U.S. large- and mid-cap stocks. With companies in the S&P 500 on track to collectively grow earnings by more than 25% this year and U.S. economic growth demonstrating relative strength, the fundamentals for U.S. stocks appear solid. Overweighting U.S. large- and mid-cap stocks may help capture a balance of tech and cyclical opportunities, manage concentration risks, and maintain a focus on higher quality investments.

- Emerging-market stocks. Like U.S. large-cap stocks, emerging-market stocks lean toward technology, providing beneficial exposure to the AI theme, and overweighting the asset class may help geographically diversify a portfolio's AI-related allocations. We believe emerging market stocks offer exposure to strong earnings growth potential at relatively attractive prices, particularly following their recent pullback.

- International developed-market value-style stocks. We're currently underweight international developed-market stocks, relative to other regions, due partly to these markets' weaker economic growth prospects. However, value-style stocks in these markets have displayed strong momentum this year—outperforming their growth-style counterparts by nearly double. We expect their momentum to continue, and we believe their cyclical exposures help diversify tech allocations, particularly as sector leadership rotates.

- Industrials and communication services sectors. Within U.S. stock allocations, we favor industrials and communication services, two sectors we expect to benefit from solid economic growth and AI adoption. We believe industrial stocks will be supported by infrastructure spending, while communication services offer exposure to the AI theme at relatively attractive valuations.

Higher-for-longer rates may create opportunities for fixed income investors, despite our underweight view on bonds. Reflecting resilient economic growth and persistent inflationary pressures, we now expect the 10-year Treasury yield to remain broadly within a 4.5%-5.0% range through year-end, up from our previous forecast range of 4.0%-4.5%. While the Federal Reserve held the federal fund rate steady in July, it noted inflation risks, and markets have priced expectations for a rate hike by year end.

Rising rates have weighed on bond prices, but they have also improved forward-return potential, creating more attractive income opportunities for bond investors. In this environment, a diversified ladder of bond maturities may help capture higher yields while balancing reinvestment and interest rate risks amid ongoing inflation uncertainty. On the shorter end of the maturity spectrum, short-term bonds offer a meaningful yield advantage over cash-like options, providing an opportunity to enhance income while maintaining relatively limited interest rate sensitivity.

We’re here for you

Markets may not reward every asset class or sector allocation at the same time, but diversified portfolios are designed with this in mind, helping investors remain disciplined and prepared for shifting conditions. Consider reviewing your portfolio with your financial advisor through the lens of your ultimate goals, setting in place a diversified strategy that keeps the focus on what you aim to achieve.

If you don't have a financial advisor, we invite you to meet with an Edward Jones financial advisor to help ensure your portfolio is aligned with your goals, positioned for opportunities, and built to keep you on course toward the outcomes that matter most.

Strategic portfolio guidance

Defining your strategic investment allocations helps keep your portfolio aligned with your risk and return objectives, and we recommend taking a diversified approach. Our long-term strategic asset allocation guidance represents our view of balanced diversification for the fixed-income and equity portions of a well-diversified portfolio, based on our outlook for the economy and markets over the next 30 years. The exact weightings (neutral weights) to each asset class will depend on the broad allocation to equity and fixed-income investments that most closely aligns with your comfort with risk and financial goals.

Diversification does not ensure a profit or protect against loss in a declining market.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Opportunistic portfolio guidance

Our opportunistic portfolio guidance represents our timely investment advice based on current market conditions and a shorter-term outlook. We believe incorporating this guidance into a well-diversified portfolio may enhance your potential for greater returns without taking on unintentional risks, helping keep your portfolio aligned with your risk and return objectives. We recommend first considering our opportunistic asset allocation guidance to capture opportunities across asset classes. We then recommend considering opportunistic equity style, U.S. equity sector and U.S. investment-grade bond guidance for more supplemental portfolio positioning, if appropriate.

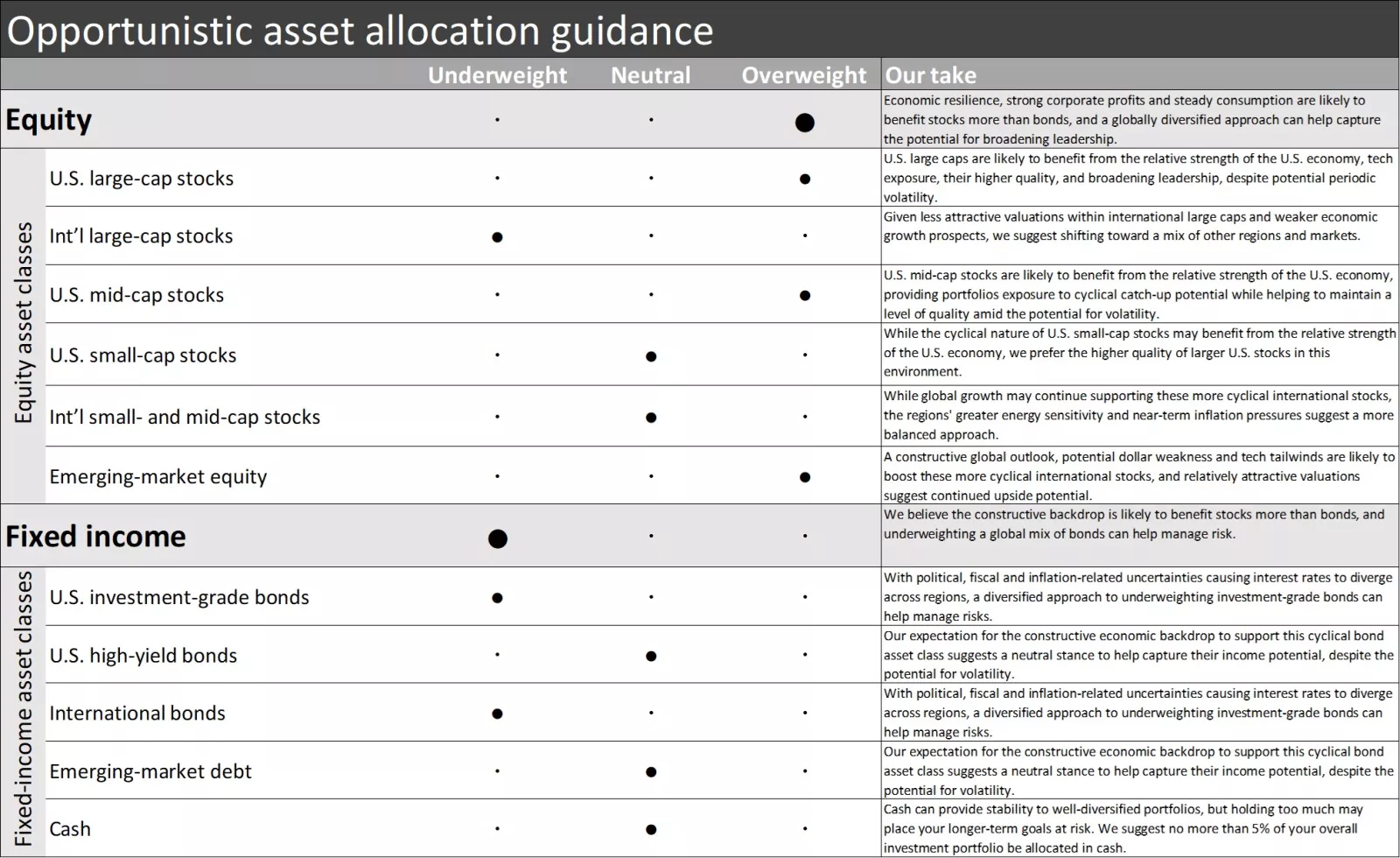

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks, U.S. mid-cap stocks and emerging-market equity; neutral for U.S. small-cap stocks and international small- and mid-cap stocks; underweight for international large-cap stocks.

Fixed income — underweight overall; neutral for U.S. high-yield bonds, emerging-market debt and cash; underweight for U.S. investment-grade bonds and international bonds.

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks, U.S. mid-cap stocks and emerging-market equity; neutral for U.S. small-cap stocks and international small- and mid-cap stocks; underweight for international large-cap stocks.

Fixed income — underweight overall; neutral for U.S. high-yield bonds, emerging-market debt and cash; underweight for U.S. investment-grade bonds and international bonds.

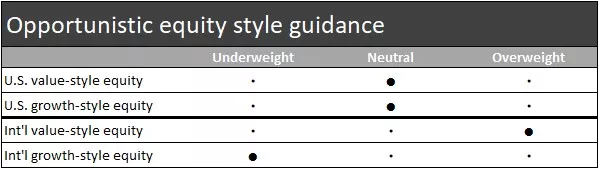

Our opportunistic equity style guidance is overweight international value-style equity; underweight international growth-style equity; neutral for U.S. value-style equity and U.S. growth-style equity

Our opportunistic equity style guidance is overweight international value-style equity; underweight international growth-style equity; neutral for U.S. value-style equity and U.S. growth-style equity

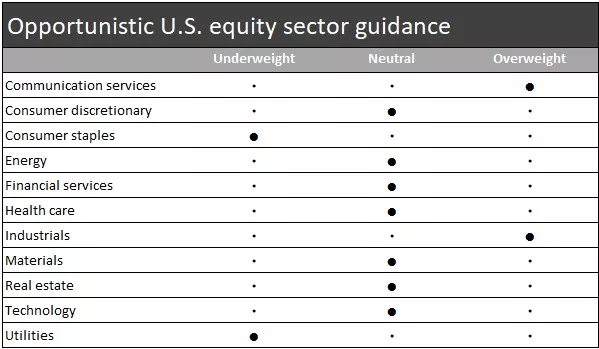

Our opportunistic equity sector guidance follows:

• Overweight for communication services and industrials

• Neutral for consumer discretionary, energy, financial services, health care, materials, real estate and technology

• Underweight for consumer staples and utilities

Our opportunistic equity sector guidance follows:

• Overweight for communication services and industrials

• Neutral for consumer discretionary, energy, financial services, health care, materials, real estate and technology

• Underweight for consumer staples and utilities

Our opportunistic U.S. investment-grade bond guidance is neutral in interest rate risk (duration) and credit risk.

Our opportunistic U.S. investment-grade bond guidance is neutral in interest rate risk (duration) and credit risk.

Tom Larm, CFA®, CFP®

Tom Larm is a portfolio strategist on the Investment Strategy team. He is responsible for developing advice and guidance related to portfolio construction, asset allocation and investment performance to help clients achieve their long-term financial goals.

Tom graduated magna cum laude from Missouri State University with a bachelor’s degree in finance. He earned his MBA from St. Louis University, is a CFA charterholder and holds the CFP professional designation. He is a member of the CFA Society of St. Louis.

Important information

Past performance of the markets is not a guarantee of future results.

Diversification does not ensure a profit or protect against loss in a declining market.

Investing in equities involves risk. The value of your shares will fluctuate, and you may lose principal. Mid- and small-cap stocks tend to be more volatile than large-company stocks. Special risks are involved in international and emerging-market investing, including those related to currency fluctuations and foreign political and economic events.

Rebalancing does not guarantee a profit or protect against loss and may result in a taxable event.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.

The opinions stated are as of the date of this report and for general information purposes only. This information is not directed to any specific investor or potential investor, and should not be interpreted as a specific recommendation or investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.