Key takeaways:

- The 2026 COLA is 2.8%, slightly above the 20-year average.

- COLA applies even if you delay claiming benefits.

- Medicare Part B premiums will likely offset some of the increase.

- A strategic use of COLA can support portfolio longevity.

After a delay from the government shutdown, the Social Security Administration (SSA) announced a 2026 cost-of-living adjustment (COLA) for Social Security benefits of 2.8%. The COLA was slightly above expectations and the 20-year average of 2.6%.

The COLA is based on the rate of inflation. The 2026 increase reflects the average change in the inflation index (specifically, the Consumer Price Index for Urban Wage Earners and Clerical Workers, known as the CPI-W) from the third quarter of last year to the third quarter of this year.

Social Security recipients will see the COLA reflected in their January benefit payment. However, if your Medicare Part B premium is deducted from your Social Security paycheck, an increase in your premium will likely offset some of the increase in your Social Security benefit.

Importantly, you’ll still receive the COLA even if you delay claiming Social Security benefits. Each year’s COLA is applied to your benefit base, so any increases you would have received are included in your benefit when you ultimately claim.

COLA’s impact on your retirement strategy

The Social Security COLA is a valuable, yet often overlooked, component of retirement planning. Because this year’s COLA is applied to the benefit you received last year, it compounds over time. This increase can help retirees keep pace with rising costs throughout retirement.

Depending on your spending plans, the COLA may allow you to maintain or even reduce how much you need to withdraw from your investment portfolio. Even small reductions in your withdrawal rate can meaningfully benefit your portfolio’s longevity.

If you don't need the COLA to pay for higher expenses, you can put those extra dollars to use by adding them to your cash reserves. Cash reserves can help you prepare for potential market declines by helping meet your spending needs while giving your portfolio time to recover.

We generally recommend retirees maintain:

- 12 months’ worth of portfolio withdrawals in cash in a separate account for spending

- Three to five years’ worth of portfolio withdrawals in a short-term fixed-income ladder

- Three to six months’ worth of spending in an emergency fund

Other Social Security adjustments

In addition to the COLA, the SSA announced these 2026 adjustments:

- Maximum taxable earnings amount — $184,500

- Earnings limit for retirees who file before reaching full retirement age (FRA) — $24,480 for years before reaching FRA; $65,160 for the year a retiree reaches FRA

Social Security COLA: A look back

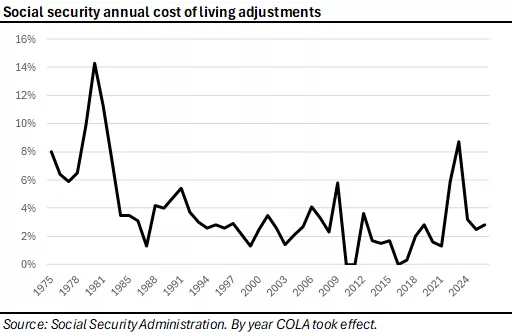

This chart provides the annual cost-of-living adjustment (COLA) for Social Security from 1975 through 2026, by the year the COLA took effect. The highest annual COLA during this period was 14.3%, and the lowest was 0%.

This chart provides the annual cost-of-living adjustment (COLA) for Social Security from 1975 through 2026, by the year the COLA took effect. The highest annual COLA during this period was 14.3%, and the lowest was 0%.

*The Social Security Administration has additional information you may find useful. This information provided by the Social Security Administration is provided as a courtesy and is intended for informational purposes only. Edward Jones makes no representations concerning the content of this site.

Kyle Harpin, CFA®, CFP®

Senior Analyst, Client Needs Research

Kyle Harpin is an analyst on the Client Needs Research team, which creates advice and guidance related to preparing for retirement, living in retirement, saving for education, estate planning and protecting financial goals.

Kyle graduated summa cum laude from the W.P. Carey School of Business at Arizona State University with a bachelor’s degree in finance. He is a CFA® charterholder and a member of the CFA Institute and the CFA Society of Nevada. Kyle also holds the CFP® designation.

Important Information:

This content is provided for educational purposes only and should not be interpreted as specific investment, tax, or legal advice. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Edward Jones, its employees, and financial advisors cannot provide tax or legal advice. You should consult your attorney or qualified tax advisor regarding your situation.

Investors should make investment decisions based on their unique investment objectives and financial situation.