You’ve settled into your retirement lifestyle, so where do you go from here financially? Consider these strategies that can help you protect your wealth in your golden years.

Monitor your spending and withdrawals

While the 4% rule can be a good starting point in determining how much you can afford to withdraw each year, your withdrawal strategy is not meant to be fixed or rigid. Retirement could last 25 years or more, and changes during that period may require you to make adjustments.

For example, if your portfolio experiences sharper declines than expected or several years of weak performance, you may need to limit any increases in your withdrawals or even reduce your withdrawals and spending to better position your portfolio to provide for your long-term needs. This flexibility can have a dramatic effect on the probability of your portfolio lasting through retirement. For that reason, your strategy should be reviewed at least annually and adjusted as appropriate.

Flexibility in withdrawals can have a big effect on your success

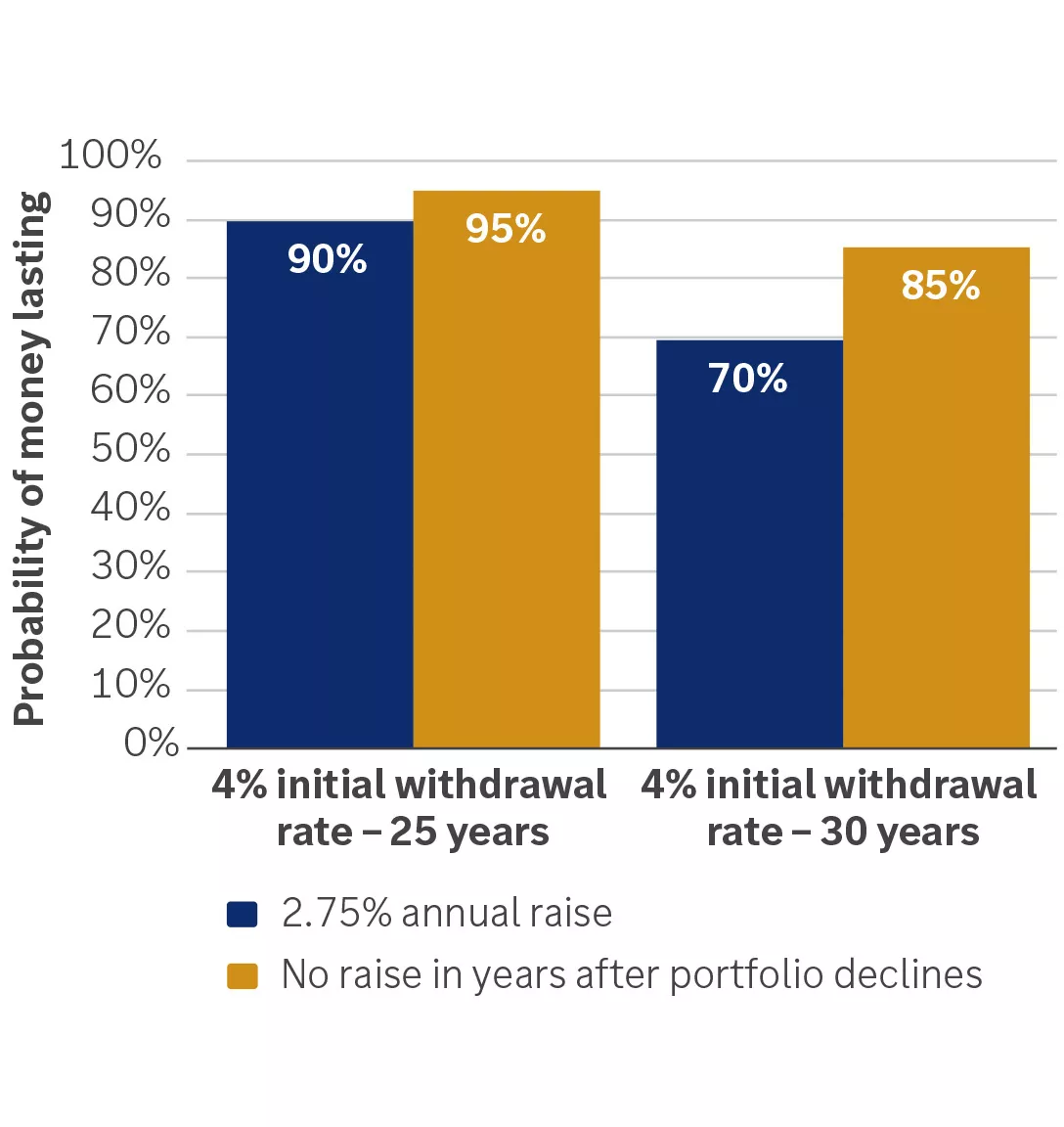

Should you take annual raises every year, or skip them when your portfolio's value declines?

The chart illustrates the impact of avoiding annual raises in portfolio withdrawals after years when the portfolio’s value declines. For investors who start with a 4% withdrawal rate, the portfolio has a 90% chance of lasting 25 years with a 2.75% raise every year compared with a 95% chance if there’s no raise following years when the portfolio’s value declines. It has a 70% chance of lasting 30 years with a 2.75% raise every year, compared with an 85% chance if there’s no raise following years when its value declines.

The chart illustrates the impact of avoiding annual raises in portfolio withdrawals after years when the portfolio’s value declines. For investors who start with a 4% withdrawal rate, the portfolio has a 90% chance of lasting 25 years with a 2.75% raise every year compared with a 95% chance if there’s no raise following years when the portfolio’s value declines. It has a 70% chance of lasting 30 years with a 2.75% raise every year, compared with an 85% chance if there’s no raise following years when its value declines.

Adopt lower-risk investment strategies — for the most part

You’ve saved for decades, but how should you invest your money after retirement? If you are withdrawing assets to meet your retirement income needs, you should consider keeping a year's worth of income needed from your portfolio in cash and another three to five years' worth of income in CDs and short-term fixed-income investments. This will help ensure your near-term income needs can be met and potentially prevent you from having to sell assets in a down market.

You'll also still need intermediate- and long-term fixed-income investments in your portfolio as well as growth investments, like stocks. As you age, your allocation to these types of investments should continue to decrease. But, depending on your age and life expectancy, you could still have 25 years of retirement left and you'll likely need growth investments to help keep up with inflation. Even if you're in your later retirement years, a small allocation to growth investments can provide diversification benefits, increasing your return potential without increasing your overall risk. As a reminder, diversification does not guarantee a profit or protect against loss in declining markets.

Additionally, if you’ve earmarked a portion of your assets for legacy goals, you have flexibility to take on more risk with those assets, since they have a longer time horizon.

Take your required minimum distributions

When you reach age 73, you’re generally required to start making minimum annual withdrawals from your tax-deferred retirement accounts, such as your 401(k) and traditional IRA. You’ll take a significant hit if you don’t: The IRS penalty for not taking the required minimum distribution (RMD) is 25% of the amount not taken on time.

The deadline to take your first RMD is usually April 1 of the year after you turn 73 and Dec. 31 each year after that. Your RMD for any year is the account balance at the end of the prior calendar year divided by a life expectancy factor from the appropriate IRS table. If you’d like more information on the requirements of your RMD, be sure to get in touch with your Edward Jones financial advisor. Additionally, the IRS provides resources to help you calculate your RMD.

Make your RMD work for you

If you need your RMD to pay for your living expenses in retirement, it should be one of the first sources you draw from since you're required to take that money anyway. If you don't need it, though, consider reinvesting the cash into a taxable account, so it can continue to grow. Or, if you want that money to go to others, you can open a 529 account for your grandchildren or start a trust for your heirs.

Additionally, once you reach age 70½, you can make a qualified charitable distribution (QCD) by transferring assets directly from your IRA to a qualified charity. A QCD can satisfy all or part of your RMD from your IRA, and for 2026 you can exclude up to $111,000 of QCDs from your taxable income each year per taxpayer, which can help lower your tax bill.

Or, since it’s a good time to be thinking about your legacy, consider using your RMD to cover life insurance costs. You can put this money into an irrevocable life insurance trust, which can provide estate tax benefits and avoid gift taxes.

Designate a trusted contact

Identify a trusted contact whom your financial advisor can reach if they are worried that you may be subject to financial fraud or exploitation, or experiencing diminished capacity. This should be someone (a family member, neighbor, friend, etc.) you can rely on and trust. This person would not be given account information, however, or have the power to make decisions for you.

Review your estate plan

You’ve secured your own financial future, but what about the situations your beneficiaries will find themselves in after your death? Now is the time to put together an estate plan if you haven’t already. It's also important to review your estate plan regularly to ensure it's still aligned with your wishes, especially after marriage, divorce or other life changes. This includes reviewing:

- Your will, which outlines how you want your estate to be handled upon your death.

- Your incapacity documents, which would include designating a financial power of attorney and health care power of attorney, as well as completing a health care directive.

- Your trust (if applicable), which allows you to designate a trustee to oversee the use of an asset on behalf of a beneficiary.

- Your beneficiary designations on your retirement accounts and life insurance policies as well as any Transfers or Payables on Death (TOD and POD) you may have on other accounts and property.

If leaving a financial legacy is important to you, you'll also want to review whether you are on track to meet your legacy goal.

How Edward Jones can help

If you’re interested in learning more about how Edward Jones can help you create an effective strategy for achieving your financial goals, reach out to an Edward Jones financial advisor today for a no-obligation consultation.

Meagan Dow

Meagan Dow is a senior strategist on the Advice & Planning Research team at Edward Jones. The Advice & Planning Research team develops and communicates advice and guidance for financial planning needs, including retirement, healthcare, preparing for the unexpected and leaving a legacy. Meagan has over 15 years of financial services and investment experience. She is a contributor to the Edward Jones Perspective newsletter and has been quoted in various publications.

Important information:

This information is for educational and illustrative purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.

Edward Jones, its employees and financial advisors are not estate planners and cannot provide tax or legal advice. You should consult your estate-planning attorney or qualified tax advisor regarding your situation.

Edward Jones is a licensed insurance producer in all states and Washington, D.C ., through Edward D. Jones & Co., L.P., and in California, New Mexico and Massachusetts through Edward Jones Insurance Agency of California, L.L.C.; Edward Jones Insurance Agency of New Mexico, L.L.C.; and Edward Jones Insurance Agency of Massachusetts, L.L.C. California Insurance License OC24309.