Congratulations on making your start in the working world! Whether you’ve just graduated from college or are starting a family, time is on your side, and building good money-management habits now can lead to greater financial security and freedom in your future. We’ve put together a list of tips to help. Keep in mind that everyone moves through life stages at a different pace, so depending on where you are, you may want to check out some of the suggestions for other age groups.

Build financial literacy

Not only do you need a grasp of basic financial terms and concepts, you have to understand how to apply those concepts – taking advantage of compound interest, for example – to help ensure your own well-being. Many U.S. residents lack that know-how, according to the Financial Industry Regulatory Authority, and make costly choices that can leave them struggling with higher monthly expenses and an insufficient nest egg to retire comfortably.

The good news is that by reading these tips, you’re already taking a step in the right direction. Increasing your financial literacy will help you understand finance and economic news, use it to make informed decisions and give you confidence in your strategy. Figuring out what you need to know is more important than ever now that most employers have shifted from defined-benefit pension plans (that guaranteed a certain level of income to retirees of previous generations) to defined-contribution plans like 401(k)s that guarantee only the size of the company’s contribution. Defined-contribution plans, for better or worse, leave the outcome of investment decisions up to you.

Evaluate income and expenses to create a budget

A budget can help ensure you’re living a lifestyle you can afford and can put you on a path toward achieving your savings goals. Start by adding up your income, then subtracting your expenses, including housing, utilities, car payments, food and entertainment. Make sure you account for expenses that may not occur on a regular basis, such as annual subscriptions, car insurance, taxes or health care expenses.

If you find that you want or need to cut expenses, consider small lifestyle changes such as packing a lunch or even larger ones such as living with roommates or your parents. Picking up work on the side will also bolster your cash flow.

Once you’ve completed your budget, put together a plan for the money you have left. It’s wise to start a rainy day fund for emergencies and begin making long-term investments as well.

Start an emergency fund

This may seem challenging when your financial resources are limited, but you’ll be glad you did when your car breaks down or the monthly power bill turns out to be twice what you anticipated because of unusually hot or cold weather.

Generally, it’s wise to keep enough to cover three to six months of total expenses, which can also carry you through an unexpected layoff or an injury that leaves you temporarily unable to generate income. That said, even a few hundred dollars can make a difference in your financial stability. Edward Jones offers solutions to save for emergencies and align those savings with your goals for investing and retirement. When it comes to cash, you want enough but not too much. Work with a financial advisor to help ensure you are not only staying on track for emergency savings but also are able to discuss the trade-offs of too much cash when necessary.

Manage your debt

Too much debt can hurt your credit score and keep you from achieving your goals. Your credit history affects not only what loans you qualify for and the interest rate you pay, but can be a factor in obtaining car insurance as well as landing the job you want. Many employers review the credit history of job applicants before making a hiring decision. If you're able, you can climb out of existing debt more quickly by paying extra each month, starting with your highest-interest, nondeductible debt like credit cards. Better yet, you could pay off your credit card bill in full every month. The less you’re spending on paying down debt, the more you’ll have for saving and investing, both of which can benefit you more in the long run.

Financial education that hits different

EdWords of Wisdom offers you the financial basics for your anything-but-basic life. Get practical financial ed-vice on, and in, your terms to help you plan for tomorrow.

Contribute to your company's retirement plan

Many companies match retirement plan contributions, and setting aside at least enough to earn the full match can make a big difference in your account’s growth. Then, work toward saving 10% to 15% of your income (including any employer match) for retirement. One way you can do that is by increasing your contribution by at least 1% a year.

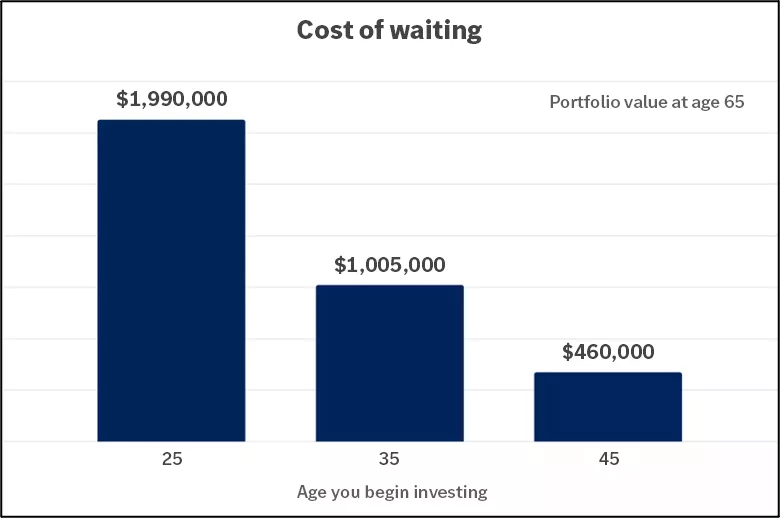

As you can see from the chart below, the cost of waiting can be significant. Take advantage of the fact that retirement is years away by contributing to your retirement account now.

This bar chart shows that waiting even a few years to start saving can significantly decrease the amount of money you’ll have when you’re ready to retire. It assumes $1,000 invested each month with a 6% annual rate of return. Example does not include taxes, fees and commissions, which would reduce the return. The tallest bar shows you could have a portfolio valued at $1,990,000 by age 65 if you started investing at age 25. The middle bar shows this same portfolio would be valued at $1,005,000 by age 65 if you started investing at age 35. The smallest bar shows this same portfolio would be valued at $460,000 by age 65 if you started investing at age 45. Figures are rounded to the nearest $5,000. Example is for illustration purposes only and does not reflect the performance of any specific investment. Source: Edward Jones.

This bar chart shows that waiting even a few years to start saving can significantly decrease the amount of money you’ll have when you’re ready to retire. It assumes $1,000 invested each month with a 6% annual rate of return. Example does not include taxes, fees and commissions, which would reduce the return. The tallest bar shows you could have a portfolio valued at $1,990,000 by age 65 if you started investing at age 25. The middle bar shows this same portfolio would be valued at $1,005,000 by age 65 if you started investing at age 35. The smallest bar shows this same portfolio would be valued at $460,000 by age 65 if you started investing at age 45. Figures are rounded to the nearest $5,000. Example is for illustration purposes only and does not reflect the performance of any specific investment. Source: Edward Jones.

Develop a smart investment strategy

Investing, or using your money to try to create more money over time, is a pivotal piece of your financial strategy. While investing can carry risk, not investing can hurt your financial future too. Given the benefit of compounding returns, it's important to get started as soon as possible, whether you’re planning to pay for your child’s education, buy a house or build a retirement nest egg.

When developing your investment strategy, you'll want to consider when you'll need to access your money and your comfort with risk. For short-term goals, such as saving for a down payment on a house, you'll generally want to hold cash and short-term fixed-income investments. For long-term goals, such as retirement, you have the leeway to invest more in high-growth securities – which often carry a higher risk of loss but can increase your wealth tremendously over the long term. An Edward Jones financial advisor can help you decide on the balance between risk and growth that’s right for you.

Consider working with a financial advisor

Financial advisors will work with you to understand your investing goals and style. While you might be doing research on your own, an advisor can help you understand the broader picture and point out risks and benefits you may not know to even ask about.

Learn how we can help you stay on track. Find a financial advisor for a no-obligation consultation today.

Whatever you do, start now

Time is a very valuable asset. The sooner you set your goals and start working toward them, the more time you'll have to enjoy your plans.

Meagan Dow

Meagan Dow is a senior strategist on the Advice & Planning Research team at Edward Jones. The Advice & Planning Research team develops and communicates advice and guidance for financial planning needs, including retirement, healthcare, preparing for the unexpected and leaving a legacy. Meagan has over 15 years of financial services and investment experience. She is a contributor to the Edward Jones Perspective newsletter and has been quoted in various publications.