Keeping perspective in a headline-driven market

Key takeaways

- Geopolitics and energy continue to drive markets: The ongoing conflict in Iran is keeping energy prices elevated and volatility high, with markets becoming more concerned over a longer‑lasting energy price shock.

- Inflation pressures set to spike in the near term: Higher oil and gasoline prices are set to push headline inflation back up to around 3.5% year-over-year, delaying progress toward the Fed's inflation target for another year.

- Growth outlook resilient but uneven: A spike in inflation and tightening financial conditions will likely weigh on consumer spending, housing and other rate-sensitive activity. However, we think the economy should remain resilient, absent a larger energy crisis.

- A difficult balancing act for the Fed: Markets are pricing a small risk that the Fed is forced to hike rates this year. We think policy tightening is unlikely unless we see a larger and broader inflation outburst, with the central bank balancing these risks against threats to growth and the labor market.

- Keep a long-term focus: For some investors the recent market upheaval could provide an opportunity to lock in higher bond yields or take advantage of cheaper equity valuations. More broadly, we think investors should maintain a long-term focus and stay aligned to their strategic allocations amid spiking volatility, with time in the market typically a better strategy than timing the market.

The conflict in Iran continues to dominate market sentiment.

Reports of a U.S, ceasefire on Iranian energy infrastructure and ongoing peace talks helped lower oil prices and boost equity and bond markets at the start of last week. However, this optimism proved fleeting as subsequent headlines indicated that the U.S., Israel and Iran remain far apart on the terms of any agreement.

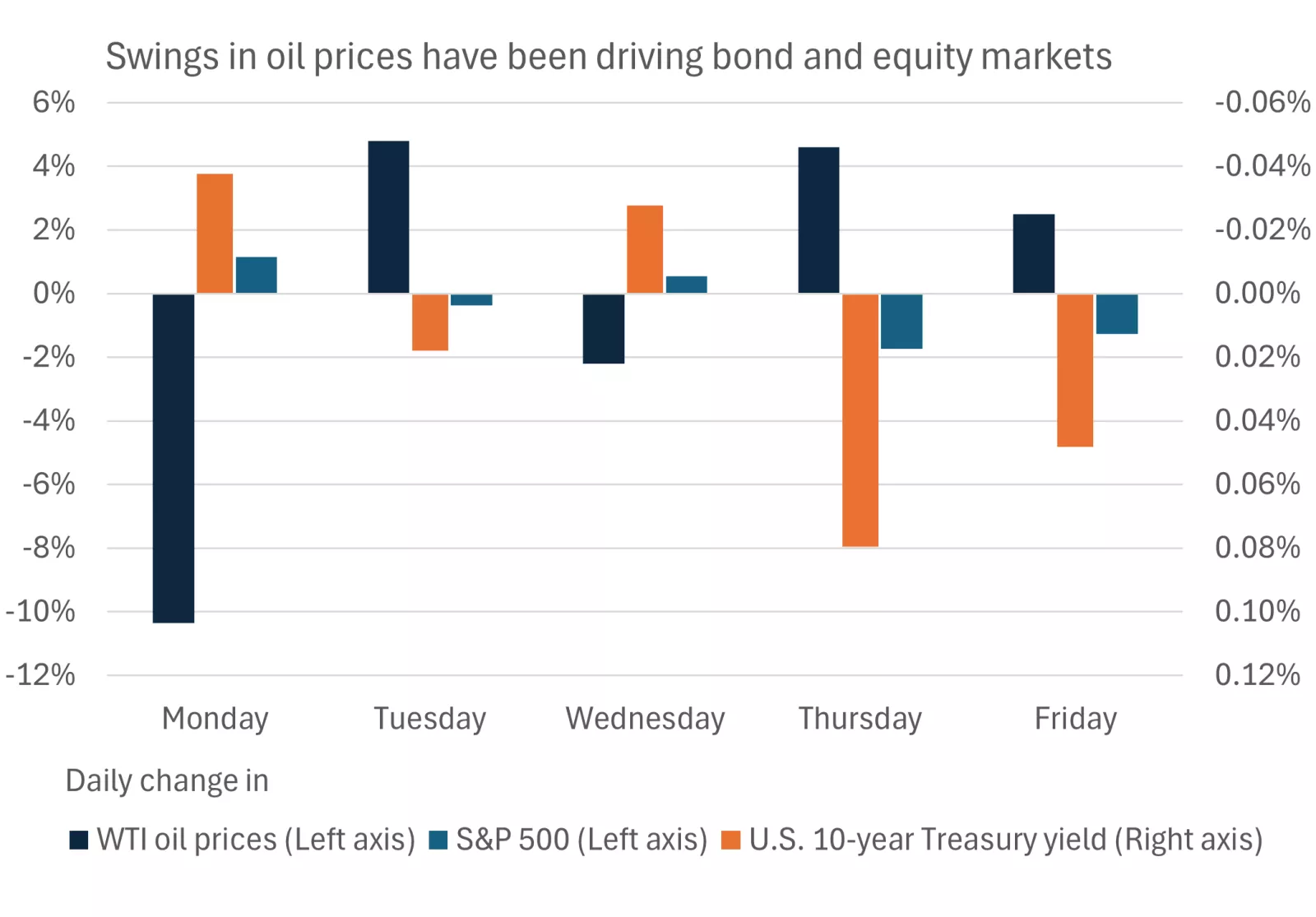

This chart shows that daily swings in oil prices have been driving moves in bond and equity markets, with lower oil prices leading to a rally in equity and bond markets, while higher prices have been associated with sell-offs.

This chart shows that daily swings in oil prices have been driving moves in bond and equity markets, with lower oil prices leading to a rally in equity and bond markets, while higher prices have been associated with sell-offs.

Against this backdrop markets seem increasingly skeptical over any quick de-escalation in the conflict, with President Trump's pledge on Thursday to extend the ceasefire on energy infrastructure failing to lift sentiment. As the conflict nears the one-month mark, markets are pricing a more prolonged spike in oil prices this year.

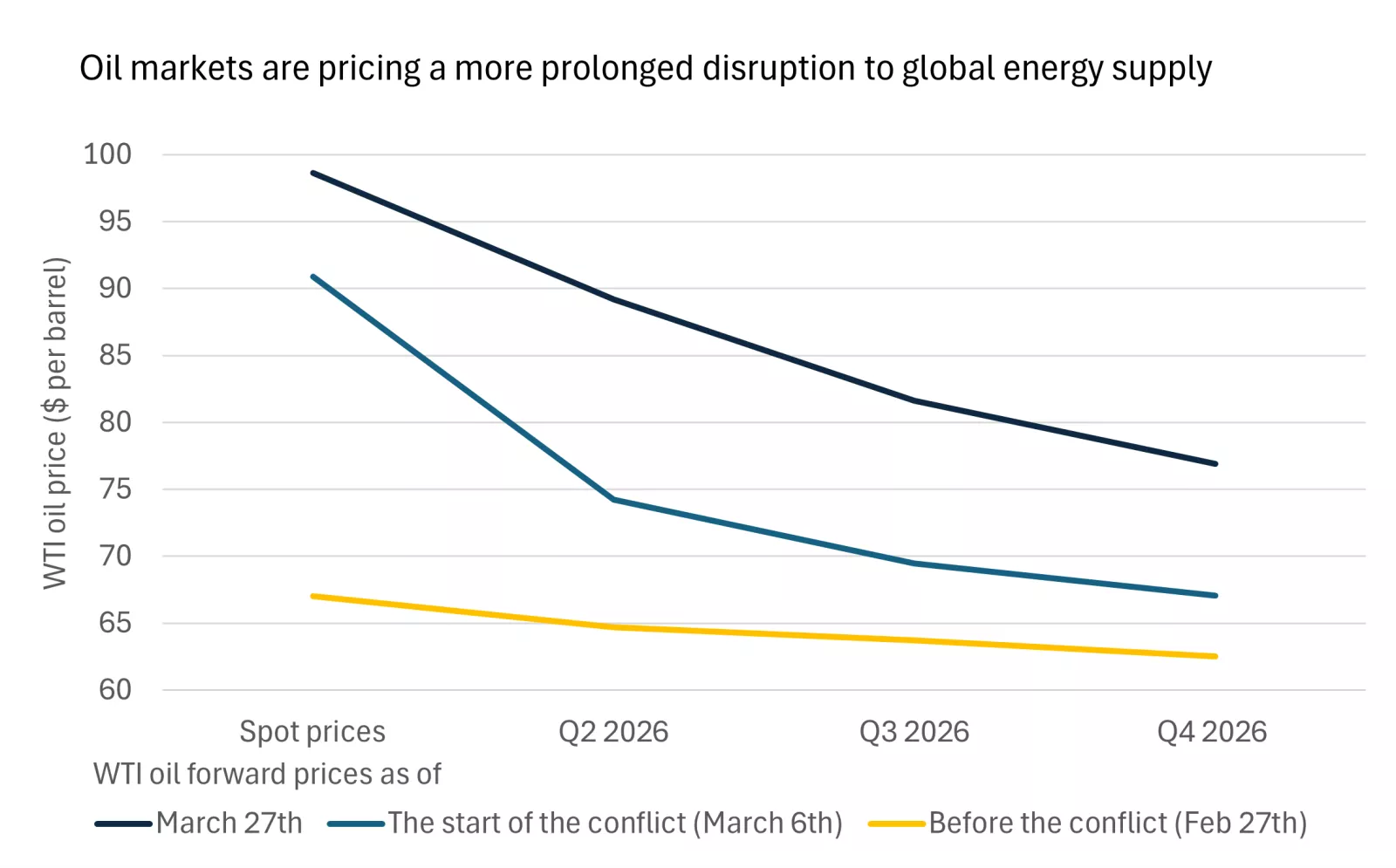

This chart shows that spot oil prices have risen as we have moved through the conflict, as have expectations around the future path for oil prices through 2026.

This chart shows that spot oil prices have risen as we have moved through the conflict, as have expectations around the future path for oil prices through 2026.

In response, equities remain under pressure as investors parse the potential impact on household demand and corporate profit margins. The S&P 500 index was down around 2% last week, although this in part reflected weakness concentrated among the mega-cap technology names, with the less technology-focused Dow Jones Index broadly flat over the same period. Bond yields meanwhile continue to push higher, as investors fret over the inflationary impact of higher energy prices and central-bank reactions to this shock.

Economic data in coming days and weeks will help give some early indication of how households and businesses are weathering higher energy prices, as well as help markets calibrate the impact on corporate earnings and outlook for interest rates.

Pressures at the pump

Most Americans will have already felt the impact of the Iran conflict at the gas pump. Average gasoline prices across the country are up to nearly $4 per gallon from $2.80 at the start of the year. In practice, this equates to around a $20 increase in the cost of filling your tank, depending, of course, on its size.

These price changes will be quickly captured in official consumer price index (CPI) data. Gas prices account for around 3% of the CPI basket, but higher energy prices will be felt in a range of other components too, including food prices, air fares and utility bills.

We think these dynamics should generate a pronounced spike in price growth in coming months, interrupting the slow progress we had been seeing toward the Fed's 2% target. Our analysis suggests that headline CPI will spike to around 3.5% in year-over-year terms in coming months on the back of higher energy prices, although core inflation that excludes these (and food prices) will rise less.

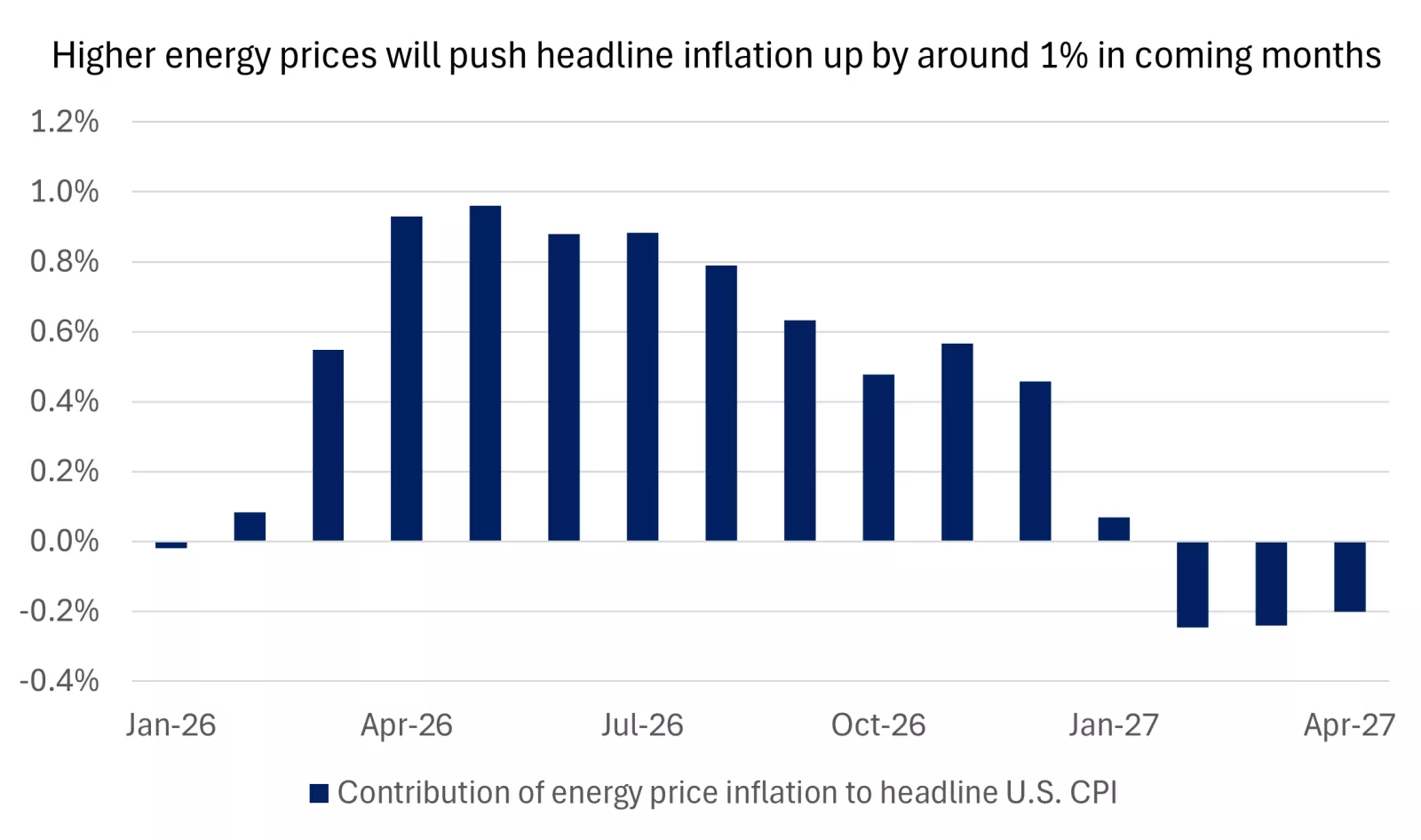

This chart shows the expected contribution of energy prices to headline U.S CPI through 2026 based on the path for oil prices embedded in forward markets.

This chart shows the expected contribution of energy prices to headline U.S CPI through 2026 based on the path for oil prices embedded in forward markets.

The good news is, in our view, that this acceleration should start to slowly fade in the second half of 2026 and ease more rapidly back toward target in early 2027, assuming the gradual moderation in oil prices expected in forward markets is correct. However, a near term price squeeze will present a headwind for households.

Keep calm and carry on spending?

We will look for early signs of how households are managing these strains in upcoming retail-sales reports. University of Michigan Consumer Sentiment data for March showed some early fallout from the Middle East conflict, with households feeling more pessimistic around current conditions, the outlook and inflation.

However, the hit to sentiment was small, and we know that consumers are supported by robust balance sheets, a still solid labor market, and tax cuts this year. Overall, we think that higher inflation will present only a modest drag on consumer spending and broader U.S. growth in 2026. However, we will need to watch for signs of any deeper retrenchment, especially if we see a larger or even more prolonged spike in global energy prices.

Elsewhere, we are likely to see some drag on interest-rate-sensitive activity in the U.S. economy. Rising mortgage rates could undermine the tentative improvement we had been seeing in housing market activity in early 2026 and pose another challenge for home builders. More broadly, the combination of higher interest rates and uncertainty could discourage aspects of business investment, although we think some of this blow should be cushioned by the ongoing explosion in AI infrastructure investment.

A slow but steady labor market?

One risk to this story of economic resilience stems from the labor market. Hiring has slowed to a crawl in recent months, and a further pullback in employment growth could push unemployment higher, potentially raising risks around the business cycle and undermining the resilient consumer backdrop described above.

Against this backdrop, we think Friday's payroll report will be even more in focus than usual. We would be surprised to see any major fallout from the conflict at this early juncture, and consensus expectations point to a solid, if unspectacular, 51,000 gain in payrolls over March and an unchanged unemployment rate. If delivered, we think this should ease fears around potential fragility in the labor market, especially following a weak February report.

Central banks in a bind

Oil shocks present difficult trade-offs for central banks. On the one hand, these push inflation temporarily higher, with the latest price shock likely to leave price growth above the Fed's 2% target for a sixth consecutive year. However, they also tend to simultaneously chip away at growth and add to potential downside risks in the economy.

The Fed acknowledged these trade-offs at its March meeting but stopped short of signaling potential rate hikes in response to higher near-term inflation, with most members still forecasting a rate cut this year in updated economic projections. This stands in contrast to other developed-market central banks, which have taken a more hawkish stance on the latest inflation disappointment, indicating a willingness to raise interest rates in response.

A balanced Fed response has helped limit the rise in expectations for rate hikes in the U.S. Markets are currently pricing only a small chance that the Fed raises interest rates this year, compared with expectations for two or three 25 basis point (0.25%) moves across European central banks and one or two hikes in Japan.

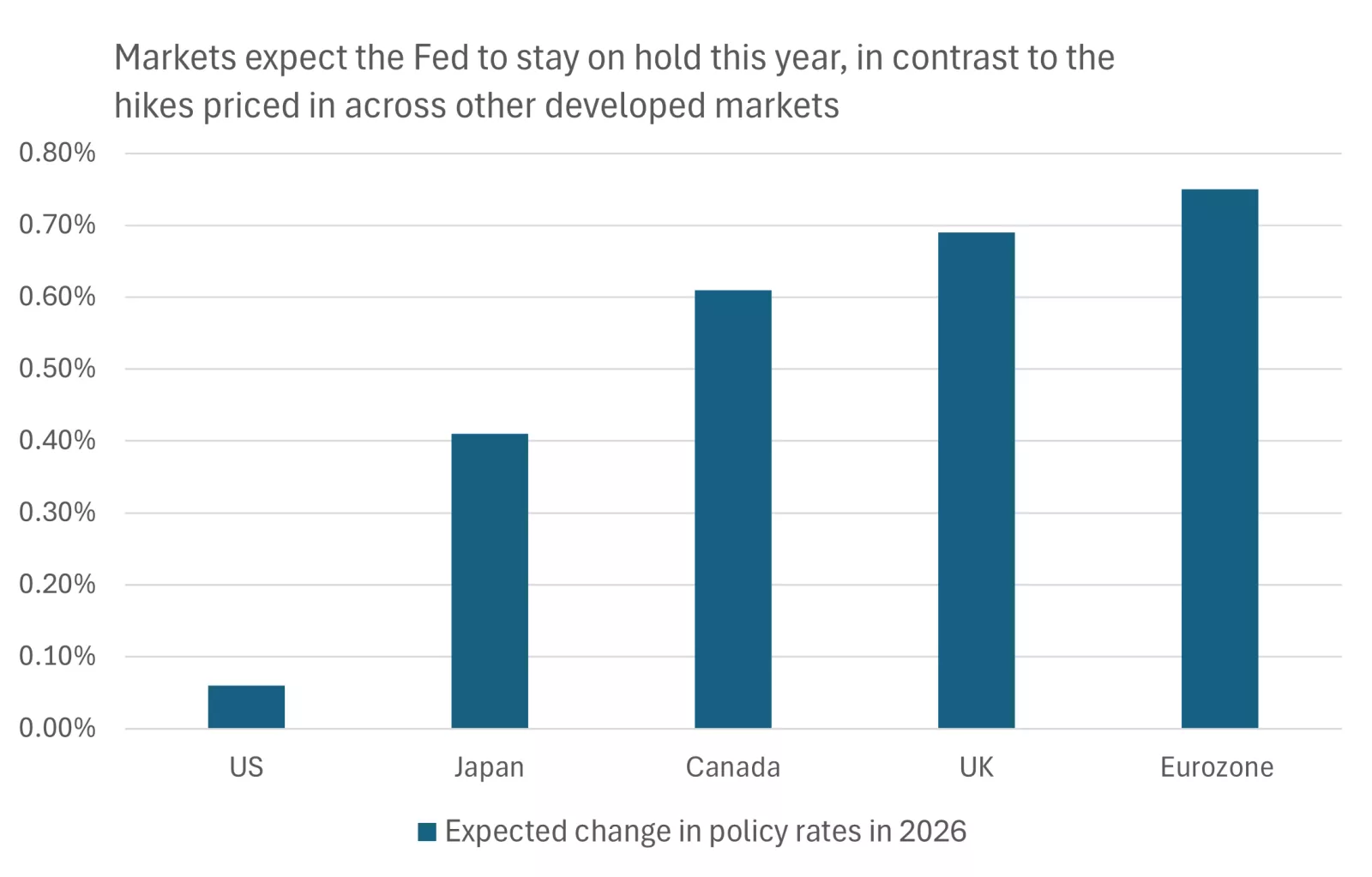

This chart shows that markets are pricing only a small chance of Fed rate hikes this year, compared to multiple hikes expected from other developed-market central banks.

This chart shows that markets are pricing only a small chance of Fed rate hikes this year, compared to multiple hikes expected from other developed-market central banks.

Until there are clearer signs of a resolution to the conflict in Iran, we are likely to continue to see markets speculate over potential U.S. rate hikes. However, some easing in tensions, and associated energy prices, should help cool these fears and potentially open the door to a renewed discussion of a potential rate cut later in the year.

Stay focused on the long term amid headline-driven markets

Markets will likely remain sensitive to news over the conflict in the Middle East in coming days and weeks. This could keep volatility elevated in the short term and maintain the painful correlations in markets which have seen equities and bonds sell off simultaneously in the face of any bad news around the conflict and energy supply.

While this might be uncomfortable in the short term, there could be longer-term opportunities emerging for certain investors.

The sell-off in bonds over the past month offers fixed-income investors an opportunity to lock in more attractive yields. The 10-year U.S. Treasury note has risen just shy of 50 basis points (0.5%) in March so far, toward the top of the 4%-4.5% range that we anticipate this year (absent a further deterioration in the Iran conflict).

Similarly, the drop in equity markets seen over the course of this shock has helped push valuations toward more attractive levels. The Nasdaq is now down 11% from its peak last year and formally entered correction territory on the back of this latest shock. Similarly, rallies in some of the best performing parts of the market this year – like emerging market equities, international equities and small-cap stocks – have been partly or fully reversed. We think that investors with longer time horizons, and tolerance for short-term volatility, might find attractive opportunities in the wake of these discounts.

Finally, while there might be opportunities for some strategic investments in bonds and equities, or targeted rebalancing of portfolios, we think the broader message for many investors should be to stay invested and diversified in the face of the latest geopolitical shock.

This chart demonstrates our belief that, over the long run, time in the market is a better investment strategy compared with timing the market. Missing just a handful of the best days of the S&P 500 over the past 30 years would have led to meaningfully lower returns.

This chart demonstrates our belief that, over the long run, time in the market is a better investment strategy compared with timing the market. Missing just a handful of the best days of the S&P 500 over the past 30 years would have led to meaningfully lower returns.

Long-term research shows that time invested in the market has outperformed timing the market, even amid bouts of volatility. Robust financial plans are built on long-term return expectations that incorporate both knockout years, such as 2023-2025, and the worse returns typical across a range of shocks. We think keeping this long-term focus can help ease some of the anxiety around inevitable bumps in the road.

James McCann

Investment Strategy

Source for all data in the commentary: Bloomberg.

Weekly market stats

| INDEX | Close | Week | YTD |

|---|---|---|---|

| Dow Jones Industrial Average | 45,167 | -0.9% | -6.0% |

| S&P 500 Index | 6,369 | -2.1% | -7.0% |

| NASDAQ | 20,948 | -3.2% | -9.9% |

| MSCI EAFE* | 2,864 | 0.8% | -1.0% |

| 10-yr Treasury Yield | 4.43% | 0.0% | 0.3% |

| Oil ($/bbl) | $100.28 | 2.1% | 74.6% |

| Bonds | $98.54 | -0.1% | -1.3% |

Source: FactSet, 03-27-2026. Bonds represented by the iShares Core U.S. Aggregate Bond ETF. Past performance does not guarantee future results. *4-day performance ending on Thursday.

The Week Ahead

Important economic data for the week ahead includes consumer confidence, retail sales, employment and S&P and ISM Purchasing Managers' Index (PMI).

Review last week's weekly market update.

James McCann

Senior Economist

Thought Leader In:

- Economic issues impacting the lives of everyday Americans.

- The effects of government spending, taxes and regulation changes on our clients.

- Building diversified portfolios to help investors reach their long-term financial goals.

“The economic, political and policy landscape is shifting dramatically, making it ever more challenging for our clients to navigate their personal finances. In this environment, it's our deep, research-driven insights that can help clients stay on track to reach their financial goals."

James McCann

Senior Economist

Important Information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.