Fueling Opportunities with Lower Oil

Key takeaways

- Recent weakness among technology stocks has grabbed attention, but the broader market remains more resilient, with leadership rotating beyond this sector.

- The shift in market leadership is likely supported by the collapse in oil prices seen over June as the U.S.-Iran peace agreement holds, helping ease inflation pressures hitting economies.

- The relief from lower energy prices should add another tailwind to a U.S. economy that already looks in good shape, with the labor market improving and growth running at solid rates.

- Softening inflation should also lessen the pressure on central banks to hike interest rates. However, in the U.S., elevated underlying inflation pressures are likely to keep policymakers cautious for the time being, supporting the dollar.

- For investors, we think the drop in oil prices could add further impetus to the rotation in market leadership beyond tech—supporting diversified equity exposure, selective short-duration bonds, and continued allocation to international markets.

A renewed sell-off in technology stocks grabbed headlines last week. The Nasdaq index fell 4.5%, led by a large 5.5% decline in the so-called Magnificent 7 mega cap names. Meanwhile, the post IPO exuberance around SpaceX appears to be fading, with shares now down 25% from their peak.

However, away from these negative headlines, there was better news. Oil prices are tumbling and economic data remain upbeat. Against this backdrop the broader equity market delivered stronger performance, maintaining the rotation in leadership seen in recent weeks.

How should investors position amid these competing forces? Let's dive into the fundamentals and explore what they might mean for portfolios.

A collapse in oil prices

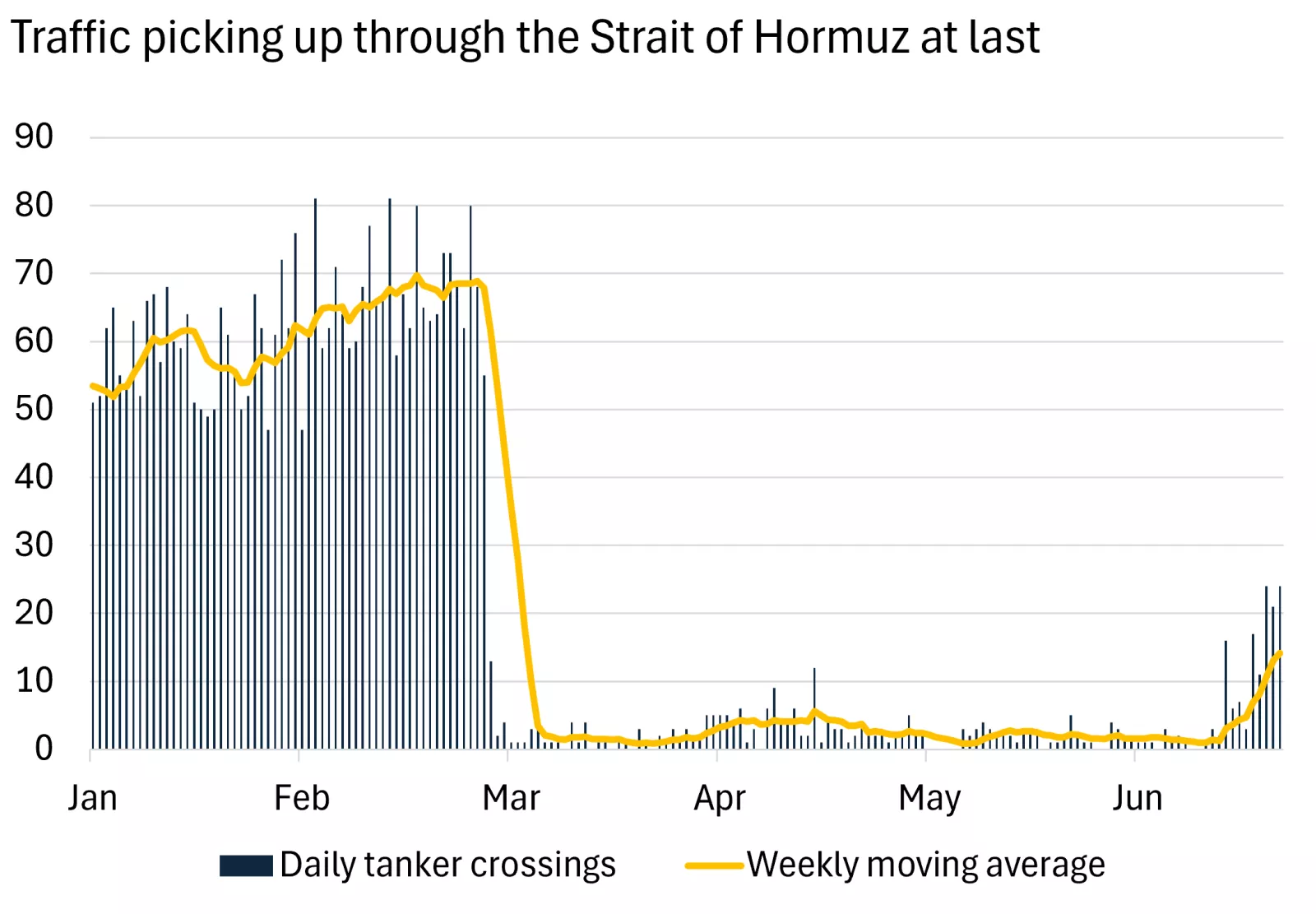

The interim peace deal signed by the U.S. and Iran earlier this month continues to hold, driving a further recovery in energy flows through the Strait of Hormuz. Tanker traffic has clearly picked up and should continue to recover in coming weeks as producers ramp up supply.

This chart shows that tanker crossings through the Strait of Hormuz have clearly picked up in June, even if these remain well down from before the U.S. Iran conflict.

This chart shows that tanker crossings through the Strait of Hormuz have clearly picked up in June, even if these remain well down from before the U.S. Iran conflict.

In response we have seen oil prices plummet. WTI is trading below $70 per barrel, down nearly $25 from this time last month and over $40 since its 2026 peak. Admittedly, prices are still above levels seen before the U.S.-Iran conflict, but much of this spike has now reversed.

Of course, an obligatory note of caution: The twists and turns of geopolitical disputes are hard to predict, and the risk of a renewed interruption to oil supply has not gone away. However, if sustained, prices around current levels could unlock some important implications for the economy and markets.

1. A disinflation breeze over the summer

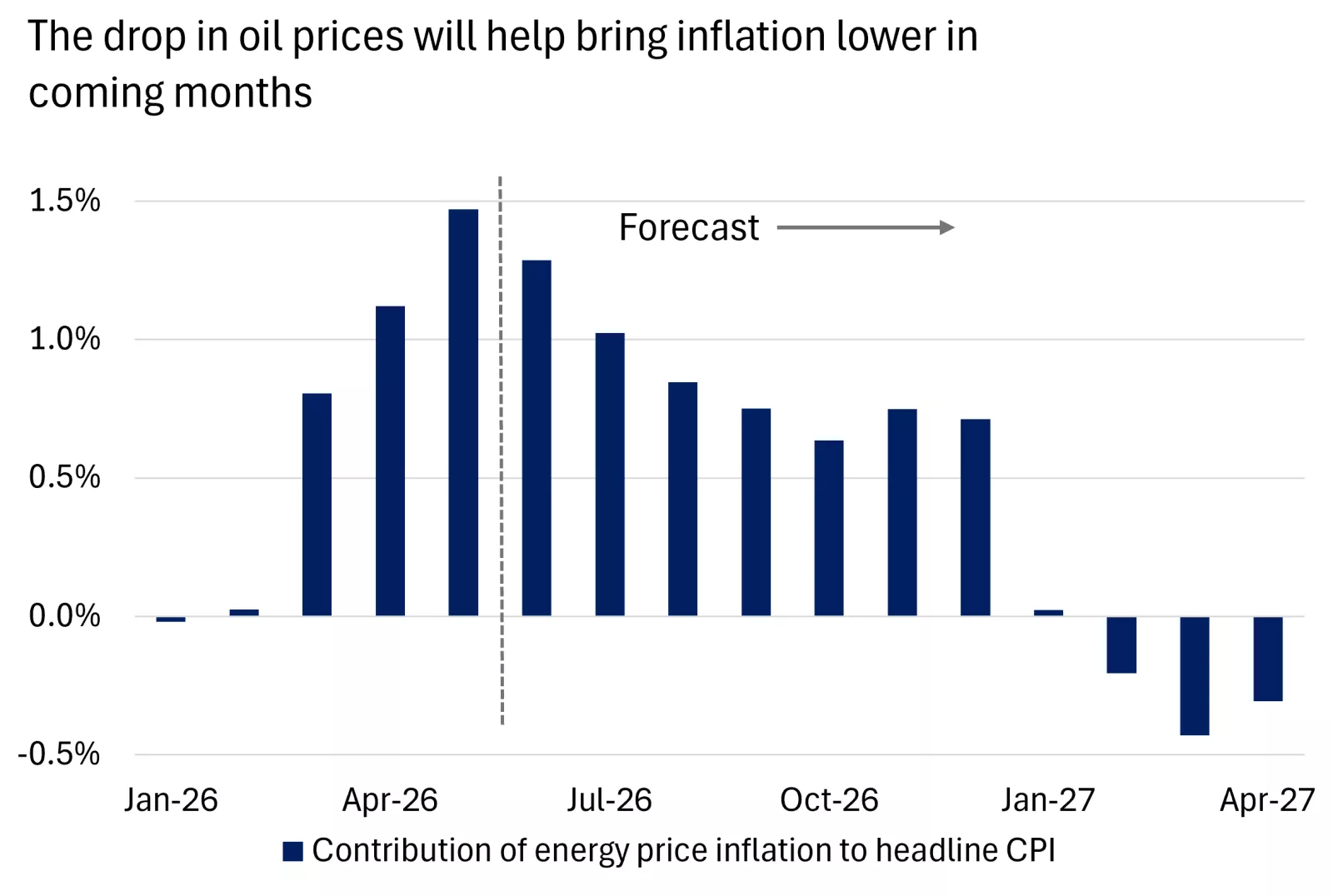

Rising energy prices have been a key driver in surging U.S. inflation this year. In the latest May data this component alone added a full 1.5 percentage points to headline Consumer Price Index (CPI) inflation, which hit 4.2% in year-over-year terms.

The good news, in our view, is that the drop in oil should reverse a good portion of this spike in coming months. By our calculations, the contribution from energy prices should moderate to around 1 percentage point in July, before falling further through the summer and fall. Absent any unexpected surges in other parts of the CPI basket this would mean that the peak in the 2026 inflation spike is likely now behind us, with helpful disinflation on the way.

This chart shows that the contribution from energy price to U.S. inflation is expected to peak in May this year, before fading notably through the summer.

This chart shows that the contribution from energy price to U.S. inflation is expected to peak in May this year, before fading notably through the summer.

2. An economic tailwind

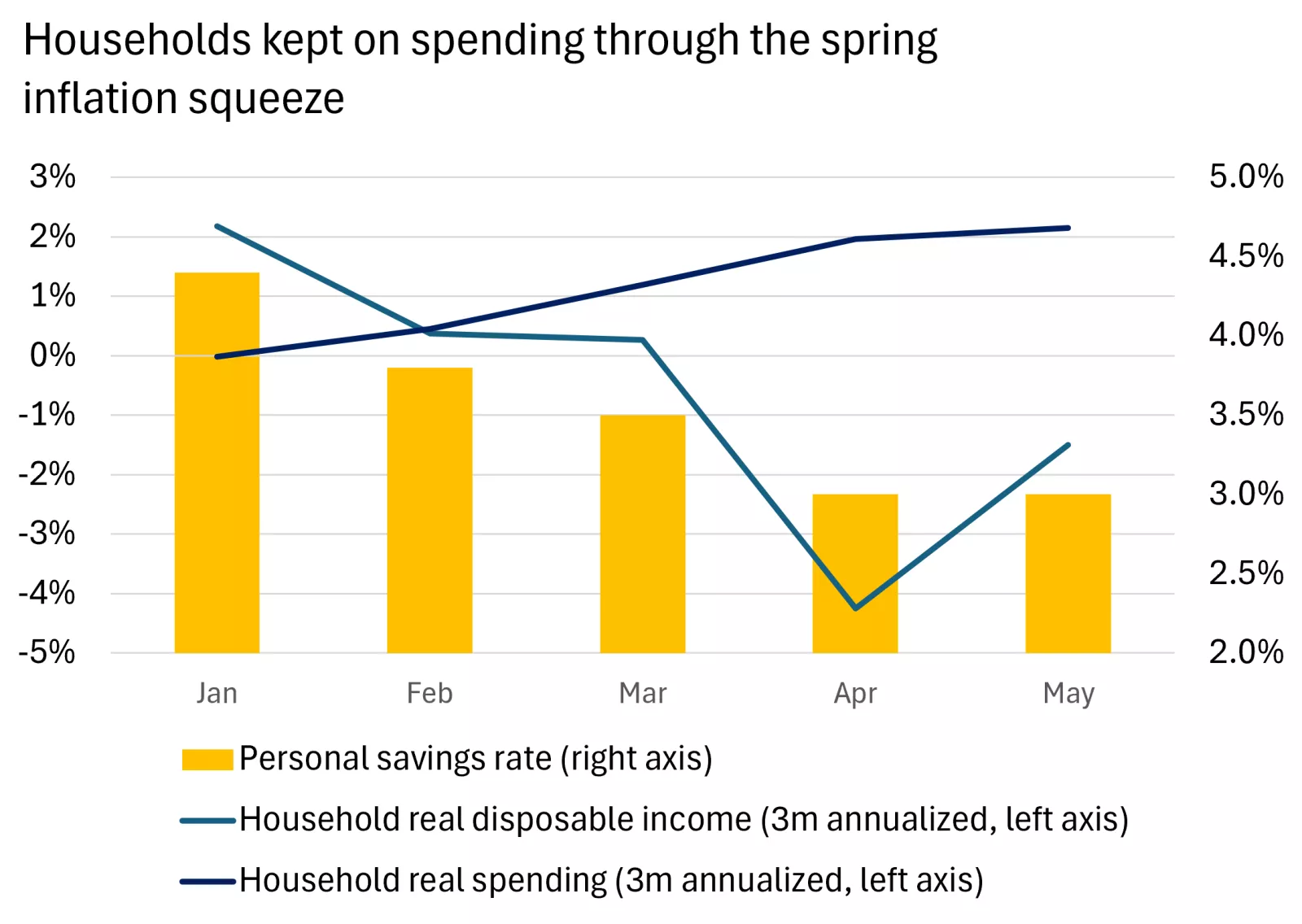

Cooler inflation should provide a helpful boost to households, with national average gas prices now down to $3.90 per gallon and likely to fall further in coming weeks and months.

We think this relief could be quite substantial. Real household incomes fell at an annualized run rate of 1.5% through March to May amid strong inflation. Households absorbed this shock remarkably well, with last week's spending figures showing a further rise in consumption in May, taking the increase in spending over this three-month period to 2.1% annualized. However, households did so by saving less, with the savings rate for the household sector down to just 3%. A partial reversal of the oil spike should provide more firepower to drive spending and rebuild savings, in our view.

This chart shows that U.S. households continued to spend freely between March and May, even as a spike in inflation pushed their real incomes lower.

This chart shows that U.S. households continued to spend freely between March and May, even as a spike in inflation pushed their real incomes lower.

This potential tailwind is just the latest cause for encouragement around the U.S. economy. The labor market has gained momentum this year (look out for this week's payroll report for further signs of improvement), first-quarter GDP growth was revised up to 2.1% (from 1.6%), and growth in the second-quarter is tracking a healthy looking 2.5%, helped by robust household and business spending.

For markets this backdrop looks supportive. We believe solid growth should continue to drive the improvement and broadening in corporate earnings growth seen this year.

3. Less pressure on central banks

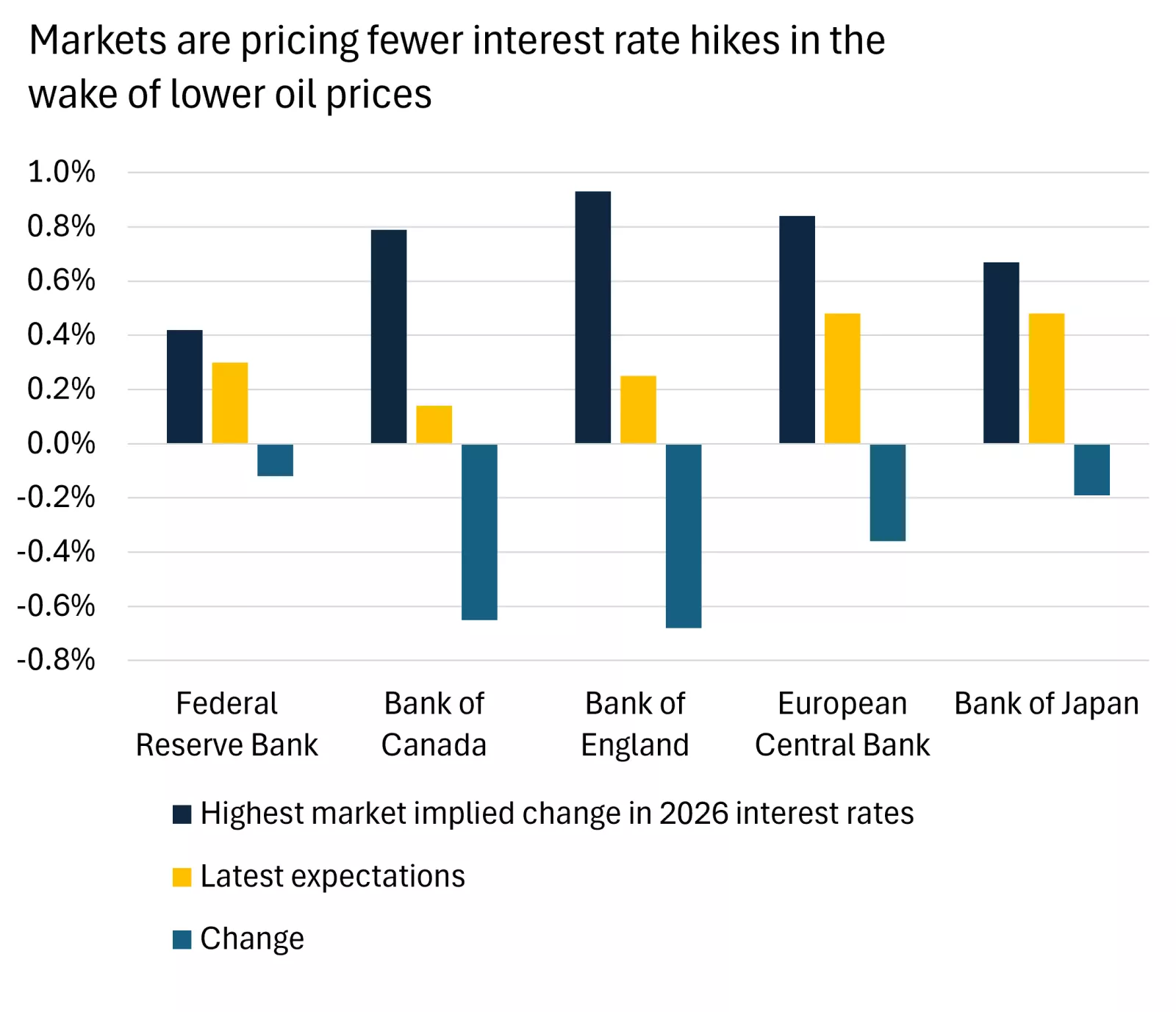

Central bankers will also likely be marking down their near-term inflation projections in the wake of lower oil prices. As these pressures moderate, markets are already anticipating fewer interest rate hikes.

This chart shows that investors have pared back expectations for central bank rate hikes across the developed economies as oil prices fall.

This chart shows that investors have pared back expectations for central bank rate hikes across the developed economies as oil prices fall.

This adjustment has been most pronounced for the Bank of Canada and Bank of England, with expectations for multiple cuts tempered by an improving inflation outlook and signs of tepid domestic growth. The eurozone and Japan have already delivered 25 basis point (0.25%) rate hikes, but markets have trimmed expectations for further moves.

In the U.S., the repricing in the short-term rate outlook has been moderate, with the expected increase in the fed funds rate this year down just 12 basis points (0.12%) from its peak. This conservative adjustment reflects the hawkish turn from the Fed at its most recent June meeting, at which half of the FOMC rate-setting committee penciled rate hikes into their forecast as concerns over the inflation backdrop worsen.

While the subsequent drop in oil prices should at least temper some of these concerns, in our view, FOMC members are also likely to have an eye on price growth excluding energy, which has been hot in recent months. Last week's PCE inflation report, the Fed's preferred measure, showed core inflation (excluding energy and food) running at a brisk 3.4% in year-over-year terms – well above the Fed's target.

We expect underlying price growth to moderate over coming months, helped by fading effects from tariff-driven inflation, ongoing moderate wage pressures and softening rental inflation. These trends, alongside the decline in energy price inflation described earlier, should keep the Fed on hold, in our view. However, the committee is signaling that it is ready to hike should inflation prove more persistent.

4. A return to U.S. exceptionalism?

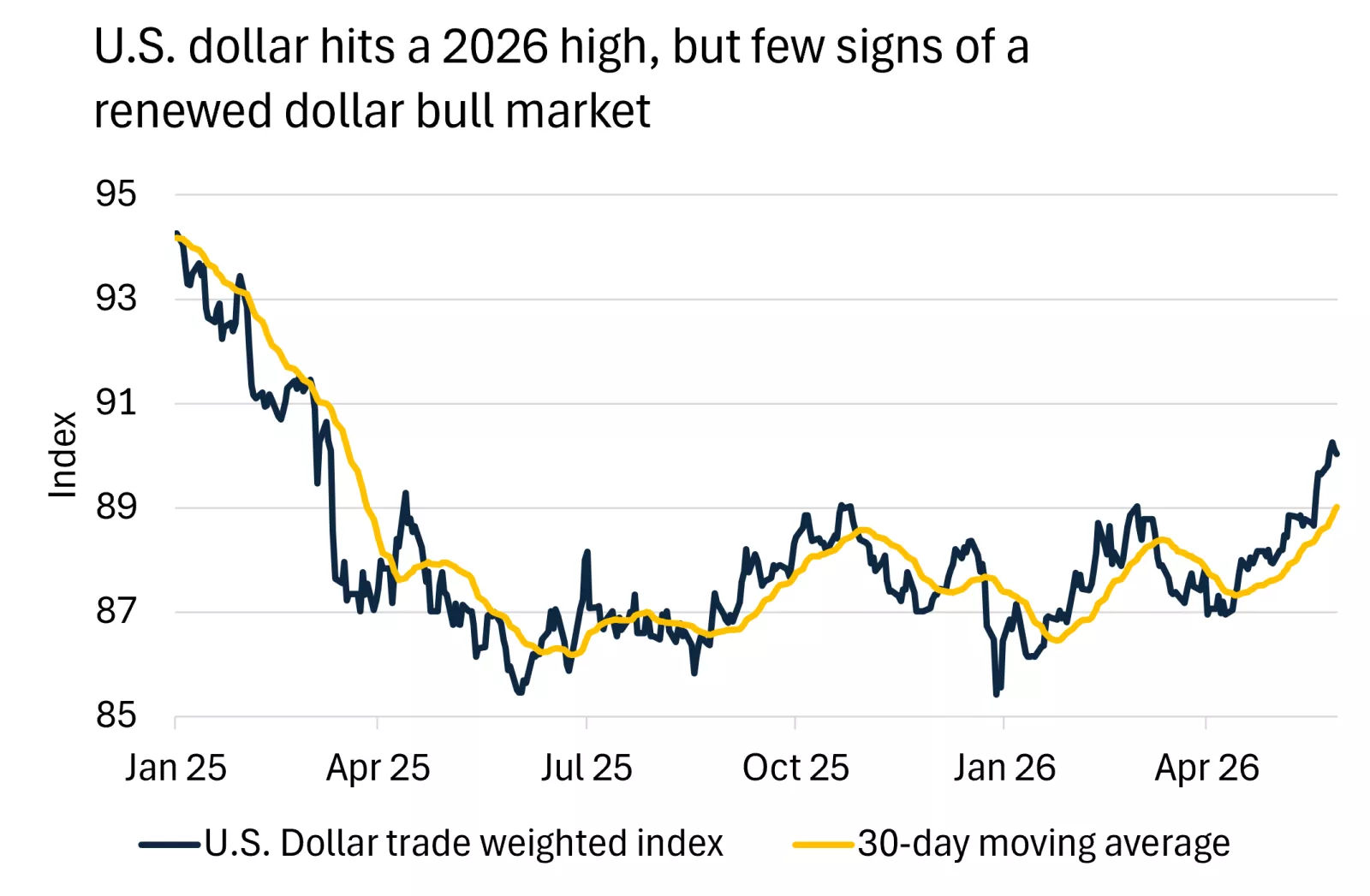

The hawkish shift at the Fed has supported the U.S. dollar, which hit a new 2026 high last week. A stronger dollar tends to be associated with weaker commodity prices, including precious metals, and weighs on the returns from investments overseas for U.S. investors too. Is this the start of a renewed period of dollar strength?

This chart shows the appreciation in the trade weighted U.S. dollar to a 2026 high. Past performance does not guarantee future results.

This chart shows the appreciation in the trade weighted U.S. dollar to a 2026 high. Past performance does not guarantee future results.

We don't think so. Periods of recent U.S. exceptionalism have been driven by stronger relative domestic growth, inflation and interest rates compared to the rest of the world. This divergence is not as apparent to us in the latest data. Moreover, despite a dip from 2025 highs, the dollar continues to look expensive from long-term valuation metrics, potentially weighing on the greenback. Finally, we have seen international investors look to diversify away from the dollar in recent years, which could continue to provide a headwind for the greenback.

Pulling the pieces together

How do we pull all these pieces together from a portfolio perspective, while also keeping in mind your longer-term investment goals and risk tolerance?

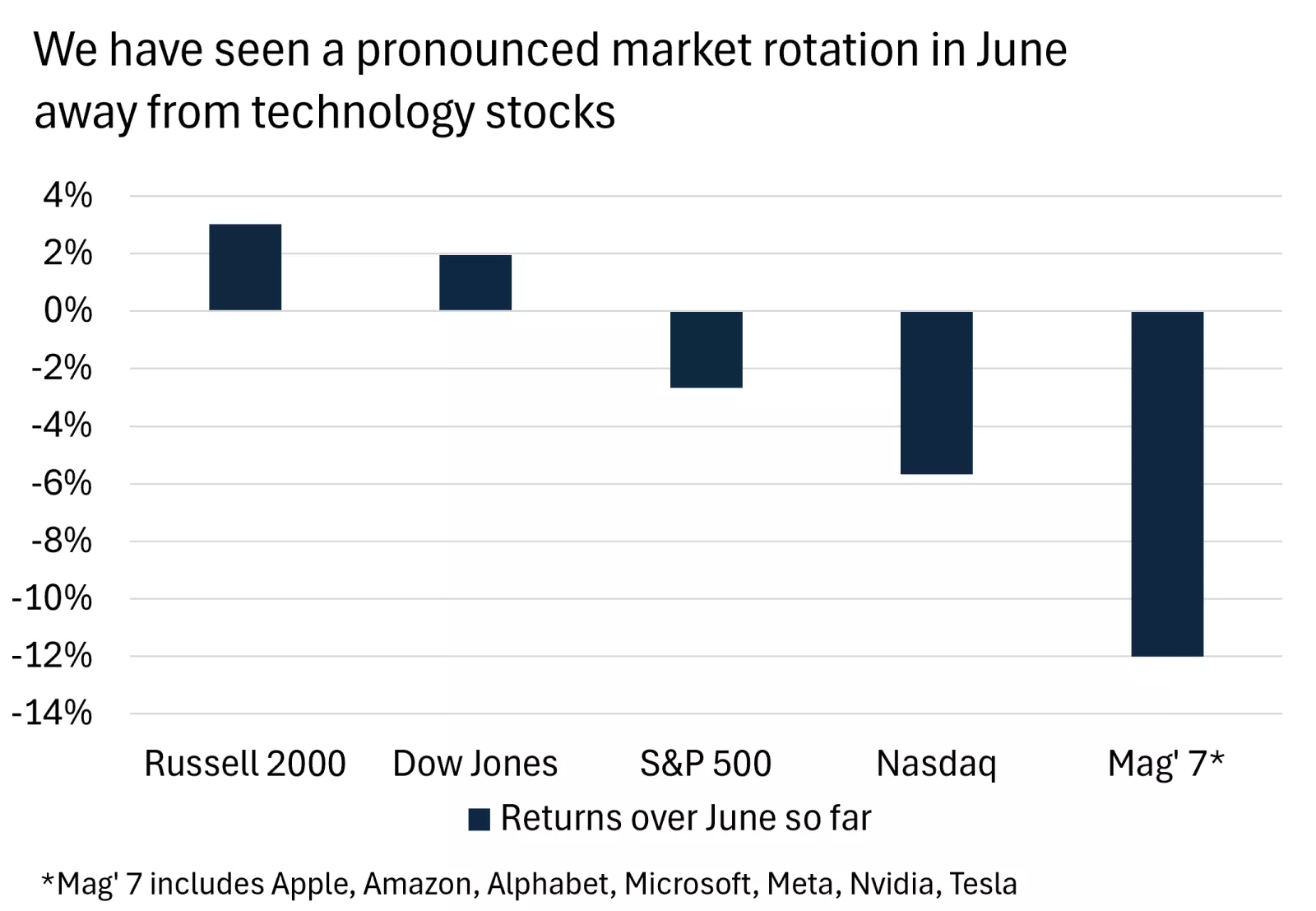

First, we think that lower oil prices add to the case for a broadening in market leadership, as this tailwind supports spending and activity across the economy. This feels especially important to us, as we see signs of the rapid rally in tech stocks from March to May reaching exhaustion. We like to hold large-and mid-cap U.S. equities to account for this potential broadening in leadership.

This chart shows the large declines in large-cap technology stock prices over June, in contrast to solid gains in less tech focused, and small-cap, indexes. Past performance does not guarantee future results. An index is unmanaged, cannot be invested into directly and is not meant to depict an actual investment.

This chart shows the large declines in large-cap technology stock prices over June, in contrast to solid gains in less tech focused, and small-cap, indexes. Past performance does not guarantee future results. An index is unmanaged, cannot be invested into directly and is not meant to depict an actual investment.

Second, while falling interest rate expectations have helped bonds rally in recent sessions, we continue to prefer to hold underweights in this asset class. That said, for bond investors, the 2-year U.S. Treasury note offers what we consider an attractive pick-up in yield (0.44%) compared to cash at present, creating a potential opportunity to increase income for cash holdings. We think these bonds could also rally if we are right that the Fed does not follow through with interest rate hikes.

Finally, we are not convinced that the recent spike in the dollar heralds a step-change in exchange rates that would justify a preference for U.S. stocks over international equities. Instead, we think holding allocations to international markets, particularly emerging-market stocks, helps provide some useful portfolio diversification.

James McCann

Investment Strategy

Sources for all data in commentary: Bloomberg, BLS, Atlanta Fed

James McCann

Senior Economist

Thought Leader In:

- Economic issues impacting the lives of everyday Americans.

- The effects of government spending, taxes and regulation changes on our clients.

- Building diversified portfolios to help investors reach their long-term financial goals.

“The economic, political and policy landscape is shifting dramatically, making it ever more challenging for our clients to navigate their personal finances. In this environment, it's our deep, research-driven insights that can help clients stay on track to reach their financial goals."

James McCann

Senior Economist

Previous weeks' weekly market wraps

Important Information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.