Headlines are louder, but the structure is holding

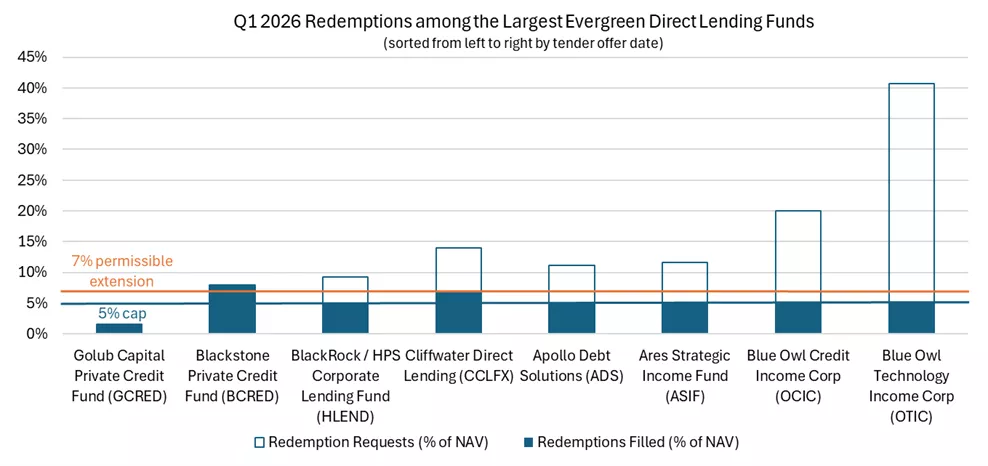

Concerns around private credit have intensified as the quarter has progressed. Media coverage has focused on rising redemption requests at several large evergreen direct lending funds. These redemptions requests have increased for those funds with later redemption notice deadlines. While these headlines have driven scrutiny, we believe the underlying picture remains broadly consistent with the original design of these funds and objectives of the asset class.

Redemptions have risen, but this was not unexpected

Redemption requests across evergreen private credit vehicles have increased in recent months, reflecting a combination of heightened media attention and investor caution. Funds with redemption dates later in Q1 have generally experienced higher request volumes, as concerns and negative headlines accumulated throughout the quarter. Blue Owl Technology Income Corp's (OTIC) redemptions are materially higher given the focus on technology which is drawing greater scrutiny due to the higher potential for AI disruption in software-related names. In addition, this fund, which is not currently recommended by IMR, has a greater portion of overseas investors who may be driving a larger portion of the redemption pressure.

Q1 2026 Redemptions among the largest evergreen direct lending funds

Q1 2026 Redemptions among the largest evergreen direct lending funds

This dynamic has produced a wide dispersion in approaches. Some funds met redemptions in full, while others fulfilled withdrawals up to their stated quarterly caps and all requested were prorated if the entire tender was not filled. These differences largely reflect timing and firm specific decisions rather than being a signal on the relative liquidity profile of the fund.

Prorating redemptions is a feature, not a flaw

Unlike mutual funds or ETFs, evergreen private credit vehicles are designed to provide periodic, limited liquidity, not full daily access. Quarterly tenders and proration mechanisms are core structural protections intended to safeguard long-term investors by reducing the risk of forced asset sales during periods of heightened redemption demand.

When redemption requests exceed stated caps, proration should not be interpreted as financial stress. Rather, it reflects disciplined adherence to fund design. While gating is often framed negatively in headlines, these mechanisms help preserve portfolio quality and protect remaining investors.

In a small number of high-profile cases, managers used permitted flexibility, such as eligible redemption extensions or affiliated capital contributions, to meet a larger portion of redemption requests in a single quarter. In one widely cited example, employee contributions helped reduce net redemptions to roughly 7%, allowing requests to be met without reopening a tender window.

While allowable under governing documents, such actions should be viewed as exceptional measures, implemented in part to manage short-term optics for both individual firms and the broader private credit market. Looking ahead, we expect redemptions to be met at stated quarterly caps, and in some cases at extended caps, with proration remaining a normal outcome when requests exceed those thresholds. It is also important to remember evergreen private market vehicles, besides those structured as interval funds, retain board level discretion on when it is appropriate to provide access to redemptions.

Putting redemptions into perspective

Redemption activity will continue to be monitored closely. If elevated requests persist for several quarters, similar to the period of elevated redemptions in private real estate during 2022, most private credit funds should be able to manage these outflows through existing liquidity tools and portfolio cash flows. However, if redemption pressure were to remain elevated for a more extended period, challenges could arise for funds that are unable to replenish capital through new inflows.

At present, outflows appear concentrated among a smaller subset of investors who may not have fully appreciated the liquidity mechanisms of these vehicles or who entered with shorter time horizons. It is important to remember that while evergreen vehicles have been the fastest growing part of private credit, most of the asset class is still accessed via vehicles without these types of early redemption mechanisms which provides stability for the asset class as a whole especially as institutions have continue to increase allocations to private credit.

Software and AI exposure: worth monitoring, but not driving credit stress yet

Another area of increased attention is the private credit market’s exposure to software and technology-enabled businesses, particularly amid rapid advances in artificial intelligence. Software represents a meaningful share of private direct lending portfolios, which has raised questions about the business model disruption AI presents to traditional software businesses and longer-term credit risk.

At this stage, available data does not indicate broad deterioration in credit performance tied to AI related disruption. Many software borrowers operate either mission critical, system of record platforms with long-term contracts, high switching costs, or deeply embedded workflows that tend to slow disruption. In addition, private equity sponsors have been actively incorporating automation and AI considerations into operating strategies for multiple years, often focusing on efficiency gains rather than reacting to a single technological shift.

While technology exposure warrants ongoing monitoring, current evidence suggests that AI is not expected to be a primary driver of losses in private credit portfolios over the near-term. As with all sector concentrations, outcomes are likely to differentiate over time, reinforcing the importance of manager selection and underwriting discipline.

Fundamentals remain stable

Importantly, elevated redemptions and heightened technology-related concerns have not been accompanied by a material weakening in underlying credit fundamentals yet. Structural features of private credit such as tighter documentation, enhanced reporting, and closer lender engagement continue to support portfolio resilience.

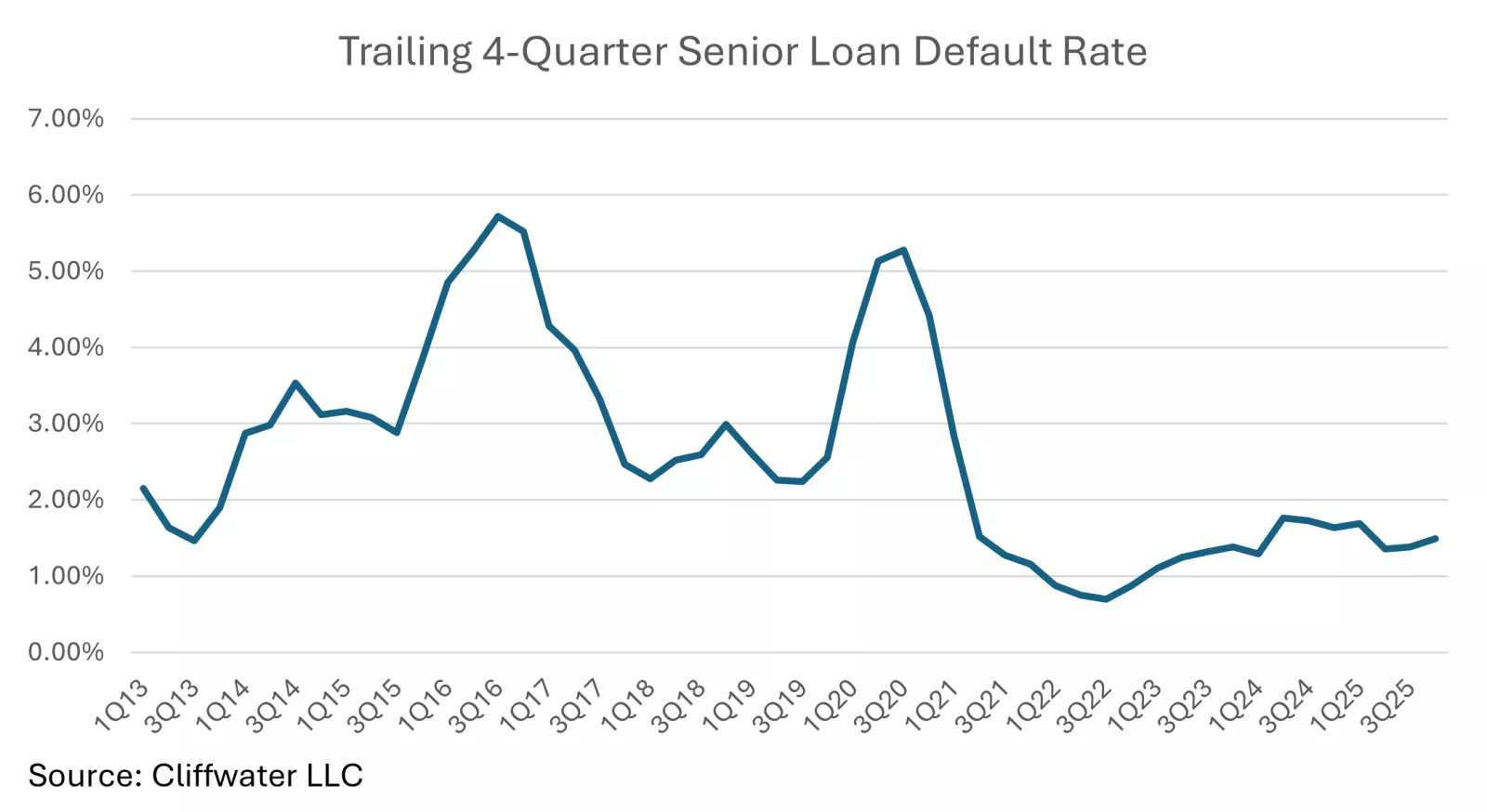

Losses are expected to rise gradually over time as part of a normal credit cycle, potentially resulting in periods of temporary net asset value pressure. Historically, however, private credit loss experience has been comparable to other leveraged finance markets, and recent default rates remain below long-term averages. It is worth noting that private credit funds often employ leverage that will likely magnify losses when they inevitably occur.

Line chart showing trailing 4-quarter senior loan default rates from Q1 2013 to Q3 2025. The chart depicts two notable peaks at approximately 5.7% in Q3 2016 and 5.3% in Q3 2020, with current rates stabilizing around 1.5%, well below historical averages.

Line chart showing trailing 4-quarter senior loan default rates from Q1 2013 to Q3 2025. The chart depicts two notable peaks at approximately 5.7% in Q3 2016 and 5.3% in Q3 2020, with current rates stabilizing around 1.5%, well below historical averages.

What this means for investors

Private credit remains a long-term allocation designed to deliver income and diversification, not immediate liquidity. While periods of negative headlines and elevated redemptions have negatively impacted sentiment, they do not alter the fundamental role of the asset class for appropriately positioned investors.

For those with realistic liquidity expectations and a long-term perspective, the current environment underscores a key point: liquidity controls are functioning as intended, even when investor demand for cash rises.

Important Information:

This content is provided as educational only and should not be interpreted as specific recommendations or investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.

Alternative investments are speculative, highly illiquid and include a high degree of risk. Investors could lose some or all of their investment. Alternative investments are designed for long-term investment. Alternative investments typically have higher fees and expenses than other investment vehicles which will lower returns achieved by investors. Alternative investments have distinctive characteristics, such as investing in private markets and investor eligibility.

Unlike mutual funds, alternative investment funds are not subject to some of the regulations designed to protect investors and are not required to provide the same level of disclosure. Before investing, you should carefully consider the features, suitability and risks of these investments