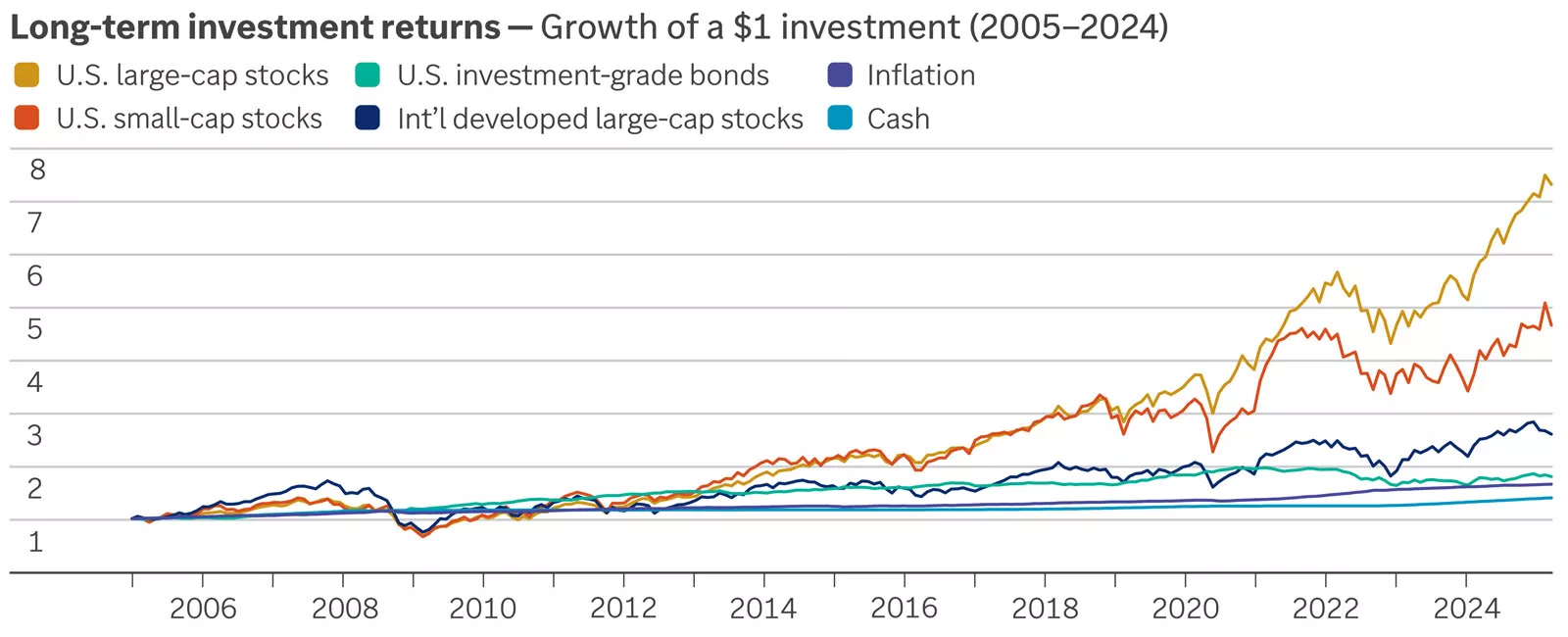

Higher growth potential — Equities serve as a cornerstone for most portfolios because of their potential for growth. In the following chart, you can see that stocks have consistently provided higher returns than bonds or cash alternatives. In fact, U.S. large-cap stocks have provided an average annualized return of 10.3% over the past 20 years.¹

But remember — you need to balance reward with risk, and investing in equities involves risks. The value of your shares will fluctuate, and you may lose principal. And generally, stocks with higher potential return come with a higher level of risk. This highlights the importance of diversifying your portfolio to help manage risk.

- Dividend income — Many companies choose to pay dividends on a regular basis, most often quarterly. While dividends can be increased, decreased or eliminated at any point without notice, investing in companies that pay dividends can provide these benefits:

- Additional income — If you’re using this money as a regular income stream, consider staggering your stocks’ dividend payment dates.

Source of investment — If you reinvest your dividends into additional shares of stock, your money has the potential to grow faster. Historically, dividend payments have been an important part of the total return from stocks. Over the past 20 years, dividends that have been reinvested have accounted for nearly 20% of the total return on stocks over the long term.¹

The power of compounding — When you reinvest dividends or capital gains, you can earn future returns on that money — in addition to the growth of your original amount invested — called compounding returns. Compounding can work to your advantage, particularly if you invest over longer periods of time.

Let’s say you purchase $10,000 worth of stock. In the first year, your investment appreciates by 5%, for a gain of $500. If you simply collected the $500 in profit each year for 20 years, you would have accumulated an additional $10,000. However, by allowing your profits to stay invested, a 5% annualized return would grow to $26,533 after 20 years, thanks to the power of compounding.2

Purchasing power protection — Inflation reduces how much you can buy because the cost of goods and services rises over time. However, as the following chart displays, stocks have historically provided protection against inflation in the long run, given the faster growth of stocks.

Equities offer two key weapons in the battle against inflation:

- Growth of principal

- Rising income

Stocks that increase their dividends on a regular basis give you a pay raise to help balance the higher costs of living over time.

This chart shows the historical growth of different types of investments and inflation, depicting how the value of stocks has grown faster over this 20-year period when compared to bonds, cash and inflation.

This chart shows the historical growth of different types of investments and inflation, depicting how the value of stocks has grown faster over this 20-year period when compared to bonds, cash and inflation.

Diversifying your investment portfolio can help smooth — but not eliminate — the impacts of market fluctuations. Maintaining a well-balanced portfolio can also help you benefit from top-performing investments as market leadership rotates over time.

Review the following allocations when checking your portfolio’s diversification:

- Asset class — A stock asset class is a group of stocks generally differentiated by their region or market capitalization size. Your portfolio’s asset class mix is one of the most important factors in determining performance. Once you’ve determined your mix between stocks and bonds, consider using our strategic asset allocation guidance as a starting point for diversifying your portfolio.

- Style — Next, we recommend diversifying across equity styles. Performance of equity styles, such as growth or value, varies across the phases of the economic cycle. We suggest owning a balanced mix of growth and value stocks to help smooth out performance over time.

- Sector — Also consider diversifying among the major market sectors and industry subsectors. Factors such as economic cycles, interest rates and market shocks can impact industries differently, just as they do for equity styles.

Making sure you have appropriately diversified your portfolio can be easier when you work with the right financial advisor. Edward Jones can help you build an investment portfolio that aligns with your financial goals now and in the future.

Market declines can be unnerving, but they’re a normal part of investing. The good news is bull markets have historically lasted much longer than bear markets and have provided positive returns that offset the declines. 4

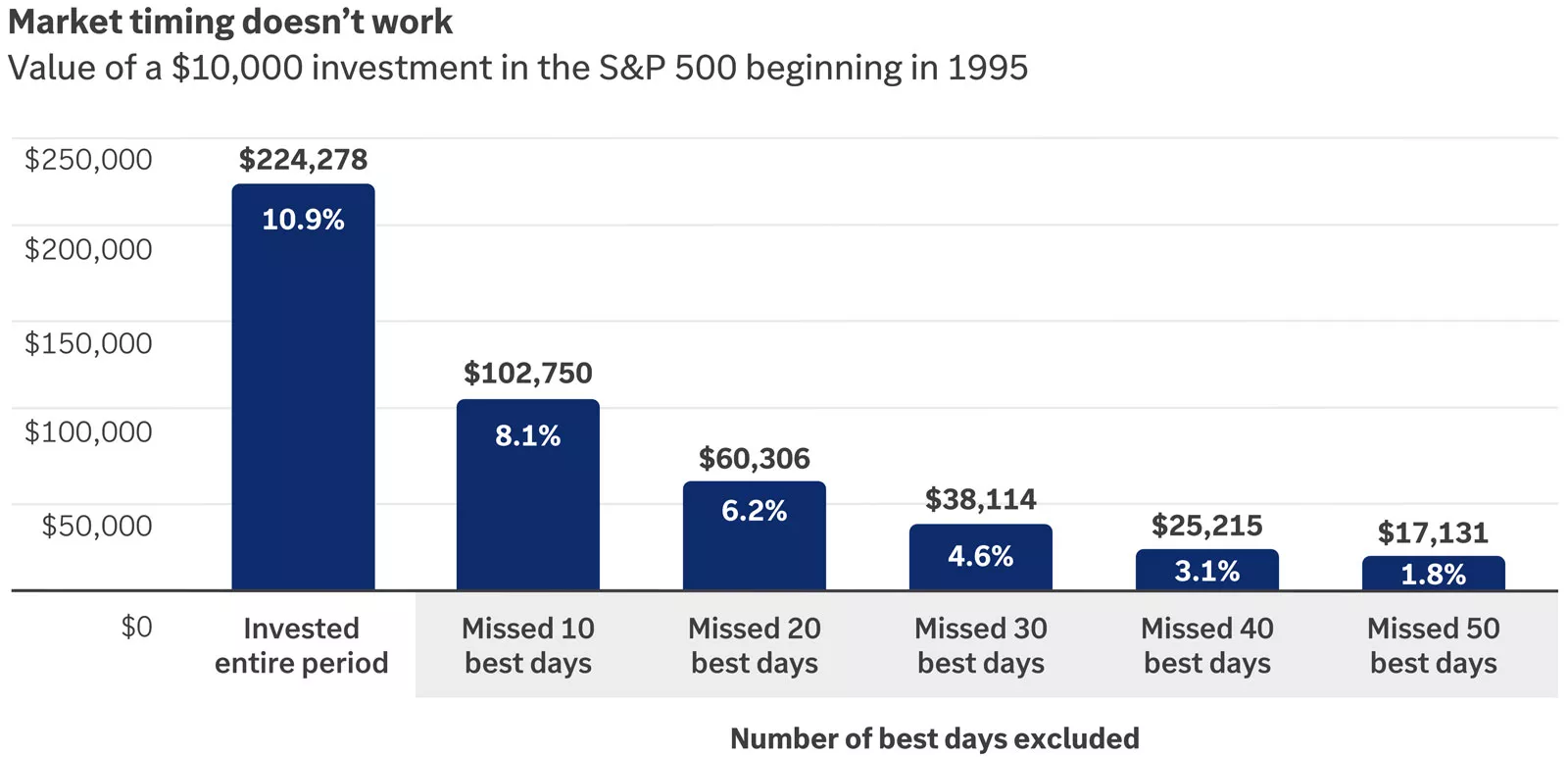

Additionally, no one can perfectly time market highs and lows. And the best days of the market have often followed some of the worst days. As the following chart illustrates, an investor who missed the 10 best days of the market experienced significantly lower returns than someone who stayed invested during the entire period, including periods of market volatility. So keep in mind that time in the market is a better approach than trying to time the market.

We recommend focusing on what you can control: staying invested with a well-diversified investment strategy that aligns with your financial goals. Strategies such as rebalancing, dollar cost averaging and reinvesting dividends can help take the emotion out of your investing decisions, helping you stay disciplined when markets hit a rough patch.5

This chart uses a series of bars to show that from the end of 1994 until Dec. 31, 2024, a $10,000 investment would have been worth $224,278 if invested for the entire period. Missing just the 10 best days during that period would reduce the value by more than half, to $102,750.

This chart uses a series of bars to show that from the end of 1994 until Dec. 31, 2024, a $10,000 investment would have been worth $224,278 if invested for the entire period. Missing just the 10 best days during that period would reduce the value by more than half, to $102,750.

You can invest in stocks by owning stock mutual funds, exchange-traded funds (ETFs), separately managed accounts (SMAs), individual stocks or a combination of these. When determining which type of investment may best meet your needs, consider the following:

Asset class — Given the differences among equity asset classes, you may consider using different types of investments to gain exposure to them. For example, given the general quality and stability of U.S. large- and mid-cap stocks, individual stocks may provide an appropriate option for you. However, for more volatile or lower-quality asset classes, such as small-cap stocks or emerging-market stocks, a more diversified investment — such as a mutual fund or ETF — may be a more appropriate option to help manage risks. Remember, while diversification cannot guarantee a profit or prevent a loss in a declining market, it can help smooth out performance over time.

Amount to invest — To help balance a portfolio of individual stocks and limit overconcentration in any single stock or sector, we believe you should own at least 25 to 30 stocks in different industries, or 15 stocks in different industries if you also own equity mutual funds or ETFs. If it’s not practical for you to own this many stocks, focusing solely on well-balanced mutual funds or ETFs can help you achieve broad equity diversification.

SMAs, which involve directly owning individual stocks managed by a professional investment manager, often have minimum investment amounts of $50,000 or more. If you have a smaller amount to invest, owning mutual funds or ETFs may be more appropriate.

Level of involvement — With individual stocks, you’ll need to monitor your portfolio’s quality and diversification on an ongoing basis. If you prefer to delegate these decisions to professional investment managers, then mutual funds, ETFs or SMAs may be more appropriate.

Tax efficiency — With mutual funds, investors have less control over when they realize capital gains, which can occur when they sell the mutual fund but also when the mutual fund sells underlying investments. Actively managed funds with higher turnover can realize capital gains more frequently than those with lower turnover. Capital gains can also be realized when investor redemptions force the mutual fund to sell underlying stocks. For this reason, stock mutual funds may be more appropriate for less tax-sensitive investors or for tax-advantaged accounts.

ETFs can avoid taxable capital gain distributions that result from selling underlying securities to meet redemption requests. Owning individual stocks, including through SMAs, can provide even more control over the potential tax impacts from investing, including potential opportunities to harvest losses more efficiently. With these investments, investors have their own cost basis and pay taxes only on capital gains realized when individual stocks are sold from their portfolios.3

After talking with your financial advisor, you may decide individual stocks are appropriate for your circumstances. But with thousands of stocks out there, how do you choose them?

We recommend a focus on quality. The following indicators can help you evaluate the quality of a stock:

- Country — Consider companies primarily based in regions that follow familiar accounting standards and reporting requirements, such as the U.S., Canada and Europe.

- Size — Larger companies usually possess a longer track record of success and a broader base of customers and sales, as well as management depth. We recommend a focus on large- and/or mid-cap individual stocks.

- Longevity — Look for companies with a solid track record. Companies with 10 years or more of operating history likely have more experienced management teams and have faced at least one economic downturn.

Financial health — Focus on companies with investment-grade credit quality. We believe dividends are also an important measure of a quality stock, particularly those with an ability to raise dividends consistently. Companies that have excess cash flow and strong financial positions often choose to pay dividends to attract and reward their shareholders. As a result, their stock is often less volatile than that of companies that don’t pay dividends.

But beware of reaching for high yields. A higher-yielding stock could indicate investors are concerned whether the company can continue to pay its dividend. We’ve found these stocks are most at risk of cutting their dividends.

Your financial advisor — using research from our trusted partners, CFRA and Morningstar — can help you determine which individual stocks are appropriate for your portfolio.

From time to time, you may need to sell a stock to help diversify your portfolio or limit overconcentration in a stock position. Significant changes in a company’s fundamentals or a stock’s valuation may also be reasons to sell.

As your portfolio’s objective changes over time, you might adjust the stocks you own to meet income needs or match your risk tolerance.