Market rally interrupted as spotlight shifts to recession worries

Published December 15, 2022

Equity markets moved lower on Thursday amid growing recession concerns. Wednesday's Federal Reserve announcement stoked worries over a potential "higher-for-longer" interest-rate outlook, while a weak retail-sales report released Thursday morning added to the market's sour mood, highlighting headwinds the economy faces in the wake of this year's aggressive Fed-policy actions to fight inflation.

Craig Fehr, CFA

Investment Strategist

1 Source: Bloomberg

2 Dollar-cost-averaging does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

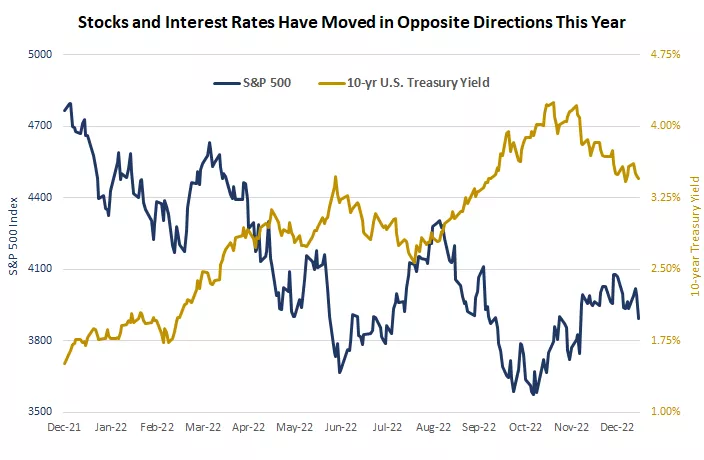

This chart shows the connection between 10-year treasury yields and the S&P 500. As the yield fall, stocks have climbed and vice-versa.

This chart shows the connection between 10-year treasury yields and the S&P 500. As the yield fall, stocks have climbed and vice-versa.

Craig Fehr is a principal and the leader of investment strategy for Edward Jones. Craig is responsible for analyzing and interpreting economic trends and market conditions, along with constructing investment strategies and asset allocation guidance designed to help investors reach their financial goals.

He has been featured in Barron’s, The Wall Street Journal, the Financial Times, SmartMoney magazine, MarketWatch, the Financial Post, Yahoo! Finance, Bloomberg News, Reuters, CNBC and Investment Executive TV.

Craig holds a master's degree in finance from Harvard University, an MBA with an emphasis in economics from Saint Louis University and a graduate certificate in economics from Harvard.

Important Information:

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.