Fed tilts more hawkish in Kevin Warsh's first meeting as Chair

Key takeaways

- The Fed held the fed funds target range steady at 3.5%-3.75% and removed the previously projected 2026 rate cut from the dot plot, as expected.

- Updated economic projections pointed to a more inflation-focused Fed: inflation forecasts moved higher, the labor-market assessment improved, and the near-term growth outlook was lowered.

- Officials remain divided on the next policy move, but the center of gravity appears to have shifted in a more hawkish direction. Rate cuts are no longer the base case, and about half of policymakers now see at least one rate hike this year.

- Markets interpreted the policy message as more hawkish than expected, pushing bond yields higher, particularly at the front end of the yield curve, which tends to be more sensitive to changes in monetary-policy expectations.

- For investors, a key takeaway, in our view, is that while interest rates may stay higher for longer, the Fed is not yet signaling the start of a renewed tightening cycle. In this backdrop, we believe equity markets can continue to perform well, particularly if earnings growth remains in the double-digit range.

Fed extends pause, shifts more hawkish

The Federal Open Market Committee's (FOMC) first meeting under Chair Kevin Warsh can be described as a hawkish pause. Because the decision to hold rates steady for a fourth consecutive meeting was widely expected, markets focused instead on the updated economic projections, the revised policy statement, and Warsh's tone in his first press conference as chair.

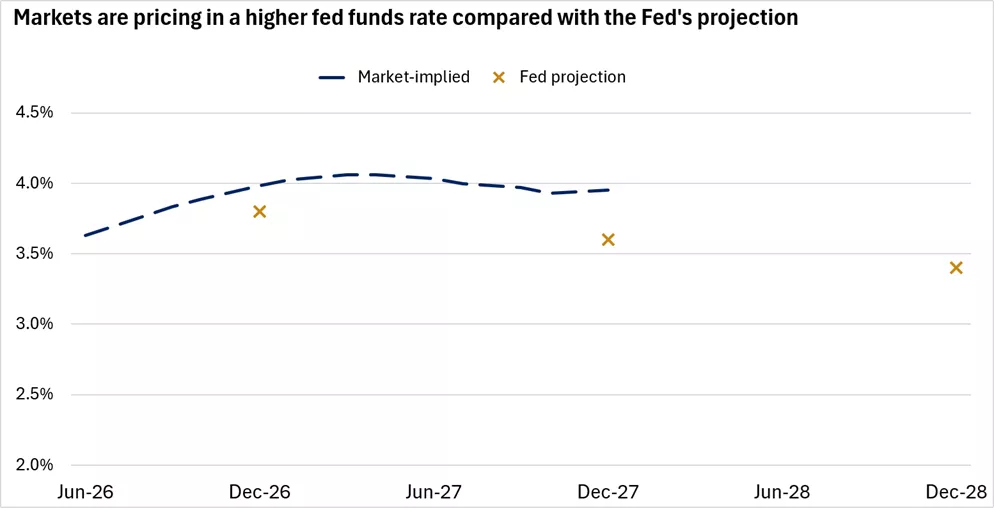

The most important changes came from the Fed's projections. Policymakers raised their inflation forecasts, which likely drove the removal of the previously projected 2026 rate cut from the dot plot. However, officials remain divided on the path forward: half of participants project at least one rate hike, while the remaining respondents expect no change or a cut. This suggests the Fed is not unified around additional tightening, but the debate appears to be moving toward whether current policy can bring inflation back to target in a reasonable timeframe. Markets responded by pricing in a higher fed funds rate than reflected in the Fed's own projections, shown below.

The chart shows that markets are pricing a higher fed funds rate compared with the Fed's projection.

The chart shows that markets are pricing a higher fed funds rate compared with the Fed's projection.

Notably, Chair Warsh did not submit a forecast, consistent with his stated preference for streamlining the central bank's communications. The projections also showed that participants lowered their near-term economic growth outlook, though it remains above trend, while upgrading their assessment of the labor market.

The policy statement was shortened significantly and shifted toward a more inflation-focused message, removing the prior easing bias and forward guidance. Taken together, the projections and statement suggest the key policy question is no longer how soon the Fed can cut rates, but how long rates may need to remain elevated to bring inflation to target.

Kevin Warsh used his first press conference as chair to reaffirm policymakers' commitment to its price-stability mandate. He also laid out a broad review of the Fed's operations, with new task forces set to evaluate the central bank's communications, balance sheet, maximum-employment and price-stability frameworks, and use of data. Meaningful changes would likely require broad consensus across Fed officials, but these announcements suggest Warsh intends to revisit and potentially fundamentally rethink how the Fed operates and communicates.

Higher inflation and stable labor market likely keep the Fed on hold

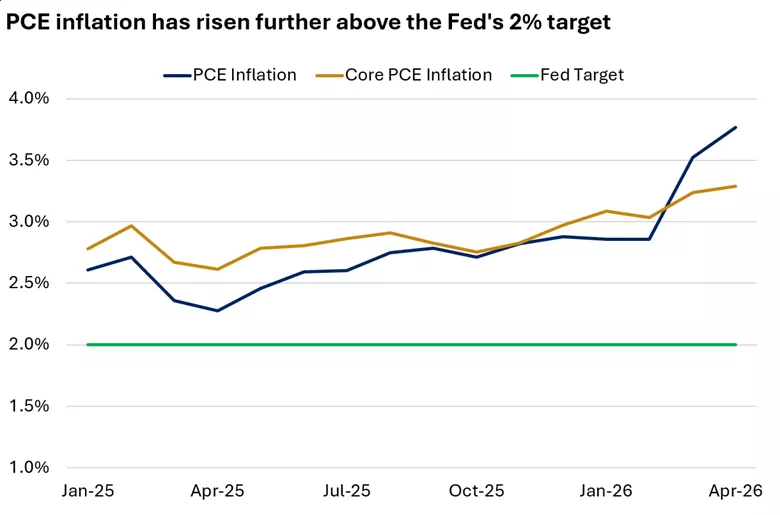

The Fed's preferred inflation gauge — the Personal Consumption Expenditures (PCE) price index — has risen in recent months, partly due to higher energy prices. Core PCE inflation, which excludes the more volatile food and energy categories, has risen more modestly, reflecting firmer goods prices. Importantly, services inflation has not shown clear signs of reacceleration, which is supportive of stable core inflation as well. Still, both measures have moved further above the 2% target, shown below.

The chart shows that headline and core PCE inflation have risen further above the Fed's 2% target.

The chart shows that headline and core PCE inflation have risen further above the Fed's 2% target.

If the recent inflation pickup remains concentrated mostly in energy, the Fed may be reluctant to respond to what could prove to be a temporary supply shock. But if energy costs feed into broader goods and services inflation — or if long-term inflation expectations move higher — we think policymakers may feel compelled to keep rates higher for longer and possibly consider a hike.

The labor market also gives policymakers more room to prioritize inflation risks. The unemployment rate remains contained at 4.3%, only modestly above the Fed's long-run projection of 4.2%, widely viewed as its estimate of full employment. In addition, 7.6 million job openings exceed the 7.3 million unemployed workers. With the employment side of the Fed's mandate largely being met, policymakers have less urgency to ease policy. Of note, wage gains also remain relatively contained, at 3.4% year-over-year in May, suggesting that stickier wage-price inflation is less of a concern.

The inflation outlook could become more balanced if geopolitical risks continue to ease and oil prices remain lower. In our view, this points to a prolonged Fed pause as the most likely outcome. The Fed is unlikely to ease while inflation is moving higher, but it does not yet appear ready to hike rates unless inflation pressures broaden or long-term inflation expectations become less anchored. Even in that scenario, we believe a single rate hike would likely be viewed by markets as a mid-cycle adjustment, rather than a renewed tightening cycle.

For markets, this suggests a “higher-for-longer” rate backdrop. That environment can remain supportive of equity markets, in our view, if higher rates reflect solid earnings and resilient growth, especially if inflation cools. Keep in mind that despite elevated oil prices and inflation, retail sales came in above expectations in May, reflecting resilient household consumption. For investors, recent trends toward sector rotation and broader market participation could also be supported by continued consumption and solid earnings growth across a wide range of sectors.

Short-term bonds now offer a wider yield advantage over cash

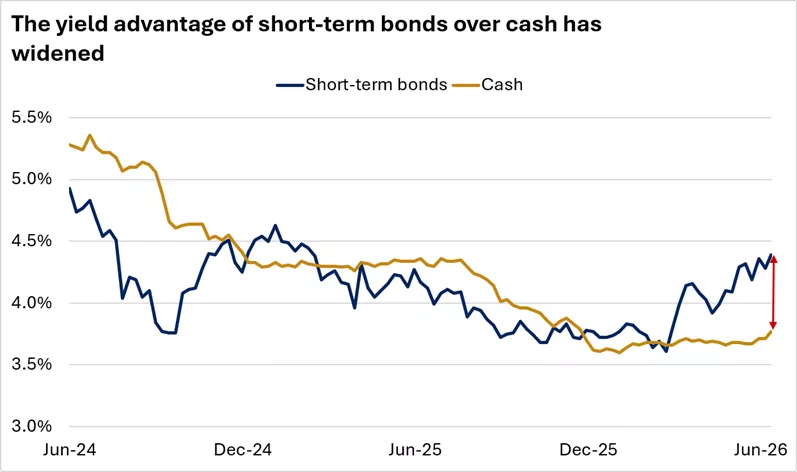

Cash yields have declined as the Federal Reserve cut rates in recent years. At the same time, short-term bond yields have risen from recent lows, reflecting a shift in investor expectations. Markets are now pricing in that the Fed may need to keep rates higher for longer — and potentially raise rates if inflation pressures persist.

Inflation expectations, a key component of bond yields, have also contributed to higher yields, especially at the front end of the yield curve. As a result, short-term bonds now offer a wider yield advantage over cash, shown below.

The chart shows that the yield advantage of short-term bonds over cash has widened. Short-term bonds are represented by the yield to worst of the Bloomberg 1-5 year U.S. Government/Credit Index. Cash is represented by the yield to worst of the Bloomberg U.S. Treasury Bellwethers 3 month Index. Past performance does not guarantee future results. An index is unmanaged, cannot be invested into directly and is not meant to depict an actual investment.

The chart shows that the yield advantage of short-term bonds over cash has widened. Short-term bonds are represented by the yield to worst of the Bloomberg 1-5 year U.S. Government/Credit Index. Cash is represented by the yield to worst of the Bloomberg U.S. Treasury Bellwethers 3 month Index. Past performance does not guarantee future results. An index is unmanaged, cannot be invested into directly and is not meant to depict an actual investment.

Importantly, short-term bonds are not the same as cash. Their prices can fluctuate as interest rates move. However, because they have shorter maturities, they are generally less sensitive to interest-rate changes than intermediate- and long-term bonds.

What this means for investors

Continued earnings strength can help support equity markets

While higher-for-longer rates could be a headwind for equities, we believe continued consumption and earnings strength can help offset higher discount rates, especially if inflation gradually moves back toward target. Valuations have pulled back recently, but earnings growth has offset much of the impact, helping support performance. However, monetary-policy uncertainty could remain a source of volatility, in our view, particularly if markets continue to reassess the likelihood of rate hikes.

Short-term bonds may offer an alternative for excess cash

Cash plays an important role in portfolios, providing funds for unexpected expenses, short-term savings goals, and everyday spending. However, holding too much cash can reduce long-term returns. After evaluating how much cash you need, consider gradually reinvesting excess cash.

Short-term fixed income — whether through bond funds, ETFs, individual bonds or CDs — may offer a way to generate additional income while only modestly extending duration. Short-term bonds can provide a middle ground between the stability of cash and the higher interest-rate sensitivity of longer-term bonds. In a higher-for-longer interest rate environment, we believe that balance may be especially attractive for investors seeking income while maintaining flexibility.

Overall, we recommend staying invested while staying mindful that geopolitical and monetary-policy uncertainty could remain sources of potential volatility. We see opportunities in U.S. large- and mid-cap stocks, which we think stand to benefit from their quality, tech exposure and broadening leadership amid continued economic resilience. And be sure to consider all of this in the context of your investment goals, risk tolerance, and time horizon.

Brian Therien, CFA

Investment Strategy

Source for all data in commentary: FactSet

Brian Therien

Brian Therien is a Senior Fixed Income Analyst on the Investment Strategy team. He analyzes fixed-income markets and products, and develops advice and guidance to help clients achieve their long-term financial goals.

Brian earned a bachelor’s degree in finance from the University of Illinois at Urbana–Champaign, graduating with honors. He received his MBA from the University of Chicago Booth School of Business.

Previous weeks' weekly market wraps

Important Information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.