Markets looking onward and upward, even as Middle East risks linger

Key takeaways

- The Middle East ceasefire continues to hold, but the ongoing closure of the Strait of Hormuz keeps risks to global energy markets elevated. A diplomatic solution remains likely, though clearer signs of progress are still needed, in our view.

- Despite these lingering concerns, markets have rallied as investors increasingly price out downside risks from the conflict and refocus on still‑healthy fundamentals around growth and corporate earnings.

- U.S. consumer spending is holding up well despite higher energy prices, with windfalls from tax cuts more than offsetting this hit. Meanwhile, business sentiment surveys are pointing to continued, if modest, underlying economic growth.

- Consistent with this resilience, we have seen only modest downgrades in earnings expectations for energy‑sensitive sectors, with these offset by continued strength and upgrades in technology, helping deliver a broad‑based and upbeat earnings profile.

- A flood of earnings reports this week will provide more color over the corporate backdrop, while the Fed is expected to remain on hold given elevated inflation and geopolitical uncertainty in what might be Jerome Powell's last meeting as chair.

- Amid uncertainty, volatility, and shifting market leadership this year, we continue to believe that staying invested across a well-diversified equity and bond portfolio provides the best strategy.

A Middle East stalemate

President Trump extended the ceasefire with Iran last week, maintaining the welcome pause in hostilities and signaling, in our view, a desire for a diplomatic solution to this conflict.

However, talks on a more permanent peace deal have, for the time being, stalled. Reports suggest that a second round of formal talks could come soon, but it remains to be seen how quickly negotiators can bridge differences over critical issues such as Iran's nuclear program and security guarantees.

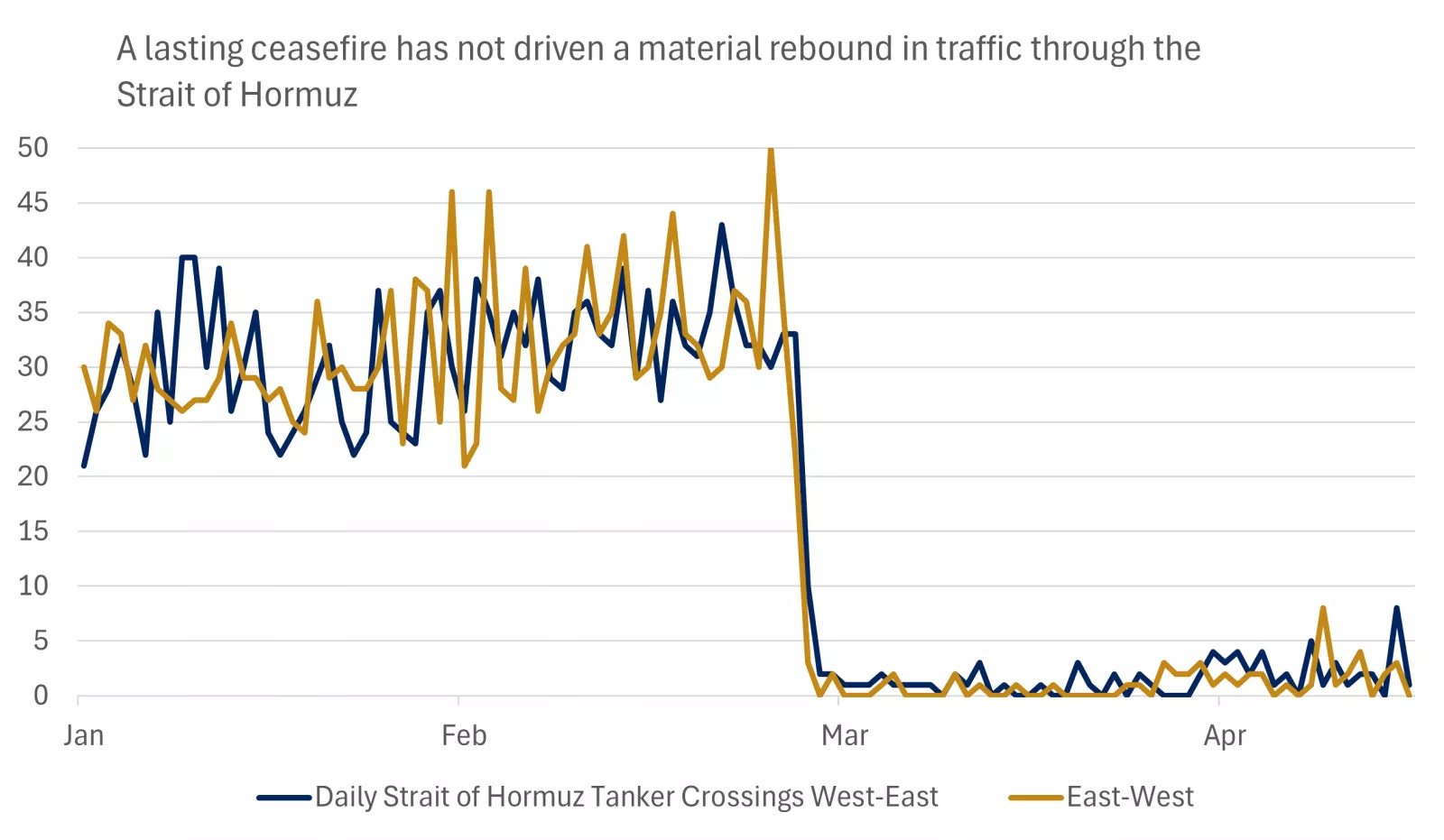

Meanwhile, the Strait of Hormuz, a conduit for around a fifth of global oil supplies, remains closed, pushing oil prices back up to $95 per barrel.

This chart shows a collapse in two way oil tanker traffic through the Strait of Hormuz over March and April, with few signs of a recovery despite a military ceasefire.

This chart shows a collapse in two way oil tanker traffic through the Strait of Hormuz over March and April, with few signs of a recovery despite a military ceasefire.

We continue to think that a diplomatic settlement that helps alleviate these pressures can be reached in coming weeks, especially with the rising costs of the conflict sharpening political incentives to find a deal. However, we will need to see more concrete signs that talks are progressing to avert further increases in oil prices that could weigh on economies and markets.

Markets looking beyond the conflict

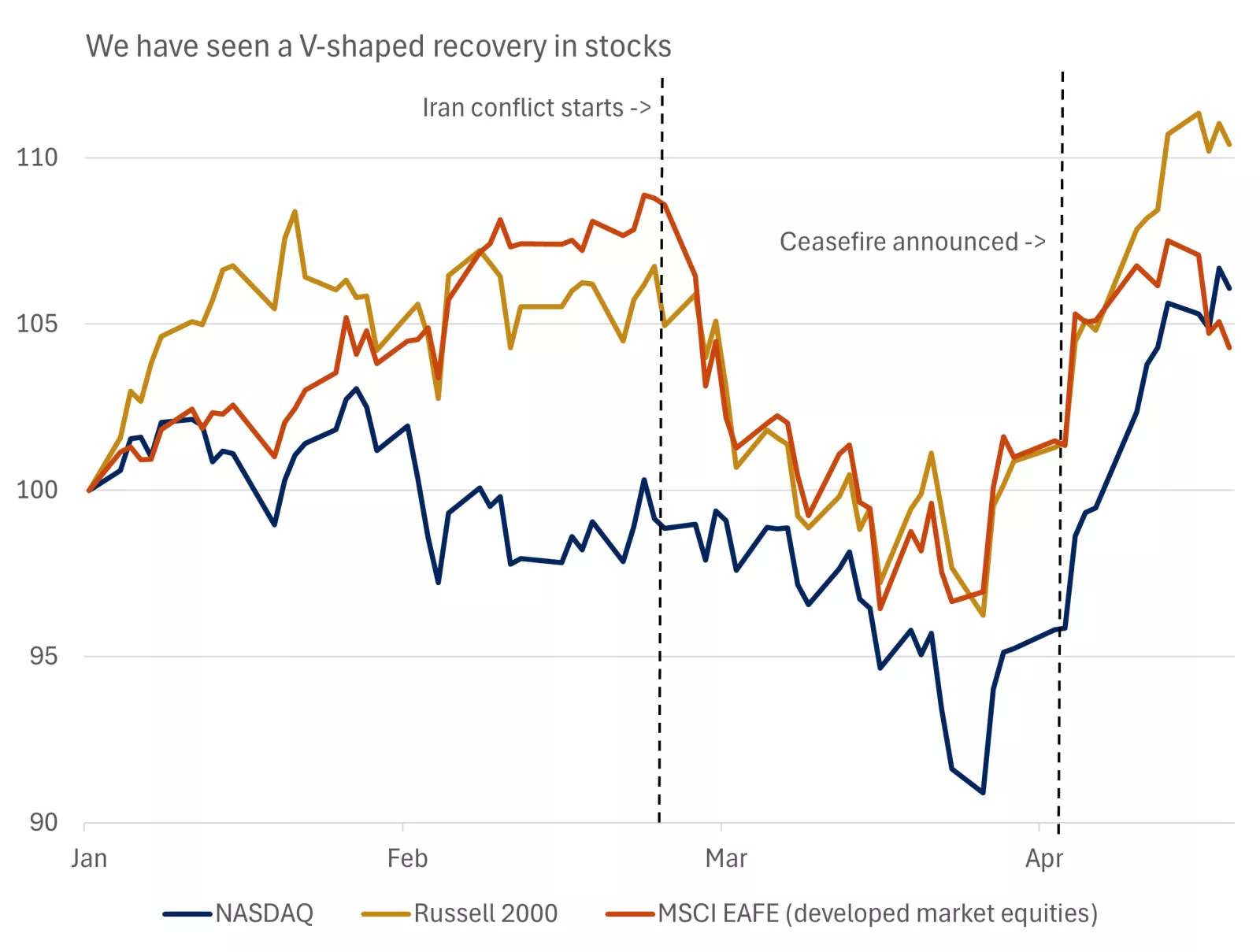

Markets have been pricing out the tail risk in the Middle East in recent weeks with equities having recouped the sell-off seen in March. This run could leave stocks vulnerable in the near-term should we see setbacks around a diplomatic solution in the Middle East.

The speed and scale of the April rebound highlight the importance of staying invested amid heightened uncertainty. An investor who sold the Nasdaq index when it hit correction territory in late March would have locked in these substantial losses and missed a near 15% rebound in this index since. Meanwhile, an investor holding through this period would be looking at a 7% gain from late February to the time of writing, albeit with significant volatility on the way. This provides a useful reminder of the old adage that time in the market beats timing the market.

This chart shows the selloff in major U.S. and international equity benchmarks at the onset of the Iran conflict, with markets recovering strongly after a ceasefire was announced in early April.

This chart shows the selloff in major U.S. and international equity benchmarks at the onset of the Iran conflict, with markets recovering strongly after a ceasefire was announced in early April.

Economy resilient for now

Last week brought the first look at how U.S. households were weathering the latest inflation shock. Retail sales jumped 1.7% month-over-month in March as surging oil prices pushed spending at gas stations some 15% higher. However, rising gas costs did not deter other types of spending. The control retail-sales measure, which excludes spending on volatile items like gas, autos and building materials, was up a robust 0.7% over the month.

Stepping back, these data point to impressive near-term resilience in consumer spending, potentially helped by stronger tax refunds in the wake of last year's tax cuts. Estimates from the Congressional Budget Office suggest that refunds could be $150 billion higher this year, which alongside lower withholdings, will help provide a boost to consumer purchasing power.

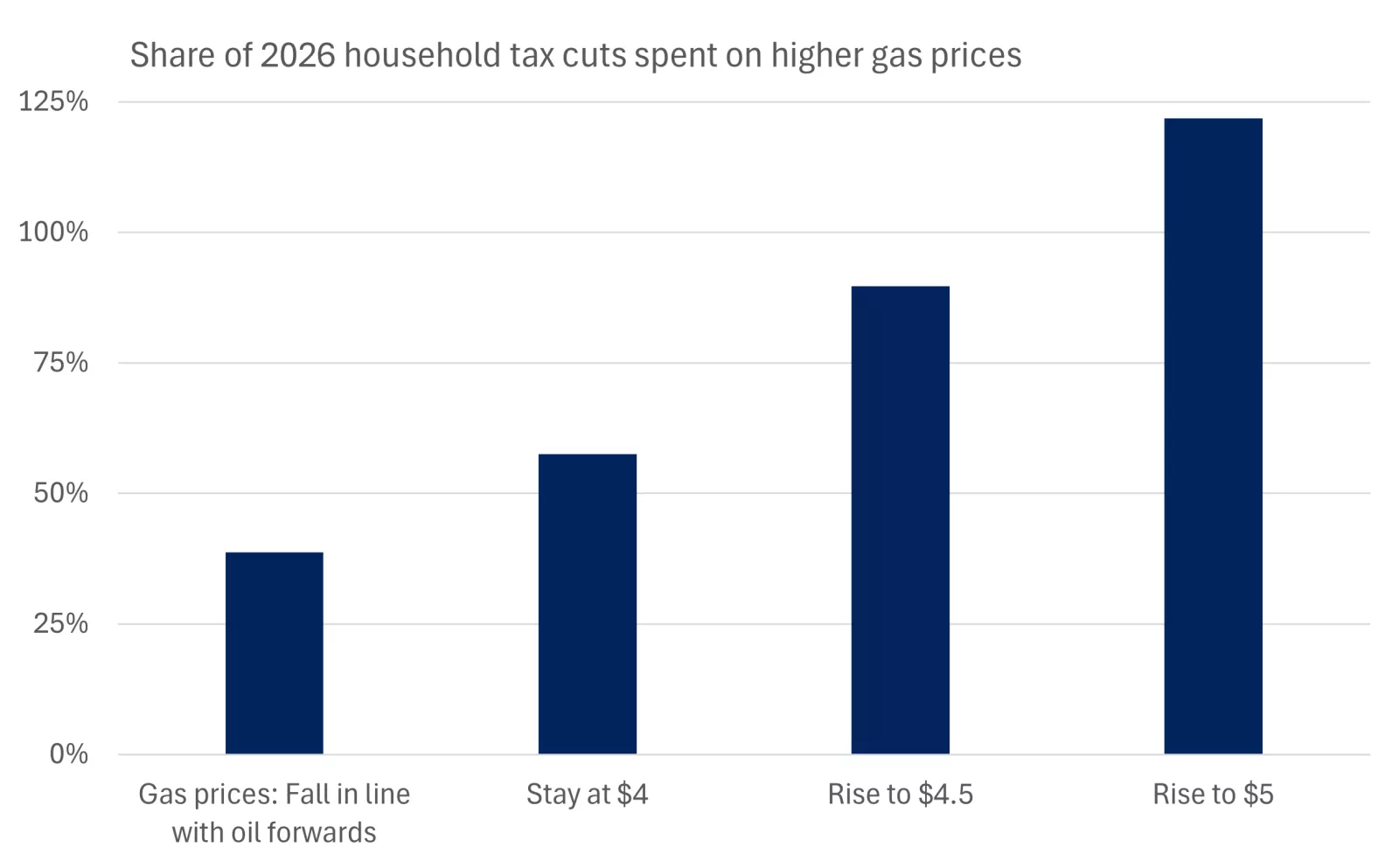

To what extent can tax cuts shield consumers from higher gas prices? Based on our analysis, higher gas prices will only eat up around 40% of these windfalls if prices fall as anticipated in forward markets. If prices remain stuck at $4 per gallon this year, the additional spending at the pump would account for more like 60% of the boost from tax cuts and lower withholdings. Finally, we estimate that prices would need to rise to between $4.75-$5 per gallon, and stay elevated at these levels, to fully absorb all the benefits from lower taxes.

This chart shows that a temporary spike in gas prices would only erode around 40% of the boost to household incomes from tax cuts, with increases to between $4.75-$5 per gallon needed to fully absorb these windfalls

This chart shows that a temporary spike in gas prices would only erode around 40% of the boost to household incomes from tax cuts, with increases to between $4.75-$5 per gallon needed to fully absorb these windfalls

This helps underline why markets are anticipating a near-term knock to growth from the Iran shock, but not a large downgrade. Businesses appear to be telling a similar story. The first estimate of the manufacturing and services PMI sentiment surveys for April came in better than anticipated, with a rebound in the composite reading of 52 pointing to positive, if still subdued, growth.

Fed under new leadership soon, but still on the sidelines

Despite a better tone in markets, the Fed is unlikely to make strong judgments around the outlook at its meeting this week. The central bank is widely expected to leave interest rates on hold, and we think Chair Powell will continue to talk to the significant uncertainty around the outlook. In practice, the signal will likely be that the Fed remains on hold as it looks to better understand the path forward in this conflict, and its fallout on growth and inflation.

This meeting could be Jerome Powell's last as chair. The path for Kevin Warsh, President Trump's nominee for chair, to be confirmed by the Senate, has cleared after the Department of Justice announced it will drop its criminal investigation into Powell following overspending on renovations of Fed buildings. The timeline for confirmation is unclear, but Warsh could be in line to take up the role of Fed chair in time for the June FOMC meeting.

Rates markets rallied in response to this news, in part likely in relief that the procedural roadblock has seemingly been eased, but also in anticipation that Warsh might be more likely to lead the committee to cut interest rates sooner than his predecessor, in our view.

We would be careful about expecting significant changes in near-term policy. It will likely be hard to build consensus for rate cuts at upcoming FOMC meetings with headline Consumer Price inflation running around 3.5% year-over-year. However, we do think a decline in gas and oil prices by the end of the year could open the door to a rate cut in late 2026.

Earnings in focus

Alongside resilient looking economic fundamentals and building hopes for lower interest rates, markets also appear to be feeling upbeat on the earnings backdrop.

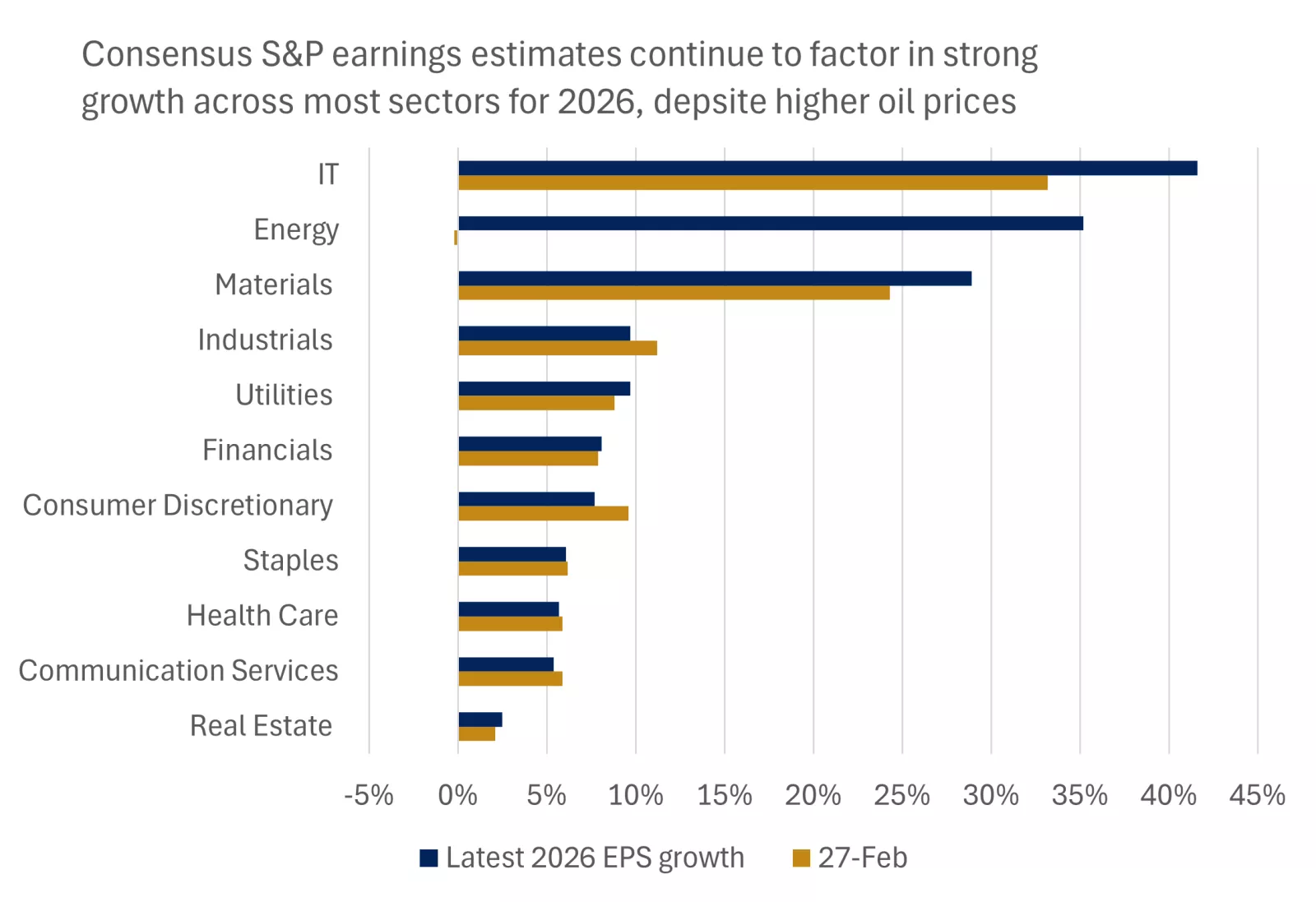

This chart shows the changes in 2026 earnings expectations by S&P sector from the eve of the Iran conflict to now, with only smaller downgrades seen in energy sensitive sectors while tech expectations have risen even further.

This chart shows the changes in 2026 earnings expectations by S&P sector from the eve of the Iran conflict to now, with only smaller downgrades seen in energy sensitive sectors while tech expectations have risen even further.

There have been some small downgrades to earnings expectations for this year in the face of higher oil prices, with these adjustments, as we might anticipate, showing up most in the consumer discretionary and industrial sectors. However, earnings growth estimates in these sectors remain solid, and across a wider range of sectors the outlook is still upbeat.

Moreover, we have seen upgrades in tech-earnings expectations to even more eye-catching levels amid a slew of positive earnings reports. Intel shares hit a new record high on Friday on much stronger-than-anticipated sales forecasts, adding to robust results in the semiconductor sector. The Philadelphia semiconductor index closed higher for an 18th consecutive session on Friday and is now up just shy of 50% over April so far.

This week we look forward to further earnings reports from the tech sector, including Microsoft, Meta, Alphabet, Apple and Amazon, which will help provide litmus tests over the AI story. Meanwhile, reports from General Motors, Coca-Cola, Exxon, Visa and Chipotle will help provide insights into how conditions look across a broader swathe of sectors.

Diversification remains the best bet

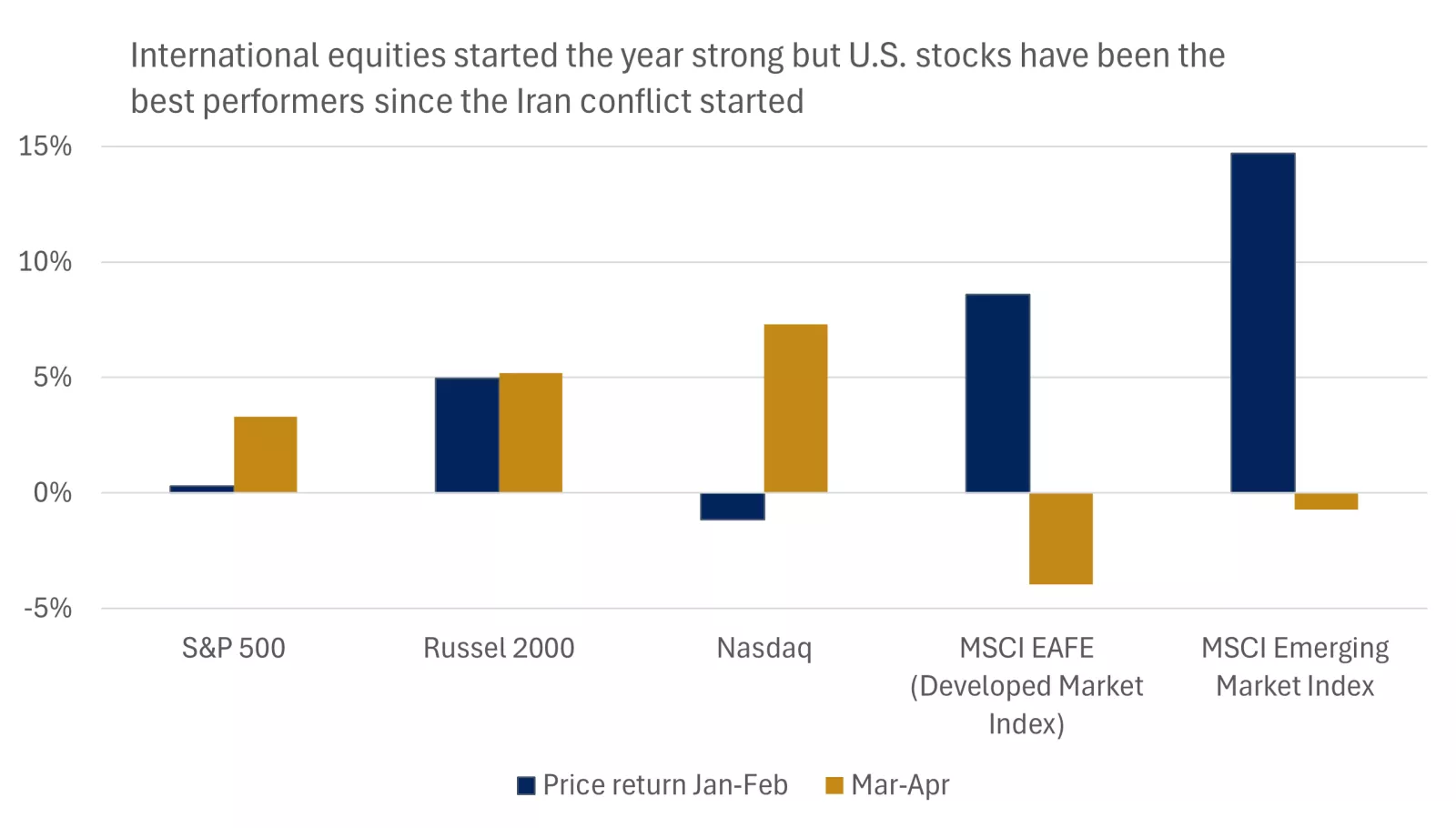

The outperformance of international equities was a key theme at the start of the year, as improving earnings growth, more attractive valuations, and a weaker dollar all combined to drive a shift in market leadership. However, in the wake of the Iran shock, and the latest upgrades to U.S. tech-earnings expectations, we have seen U.S. stocks clearly outperform since the end of February.

This chart shows the shifting market leadership in 2026, with U.S. stocks lagging international equities before the oil shock, but performing better after.

This chart shows the shifting market leadership in 2026, with U.S. stocks lagging international equities before the oil shock, but performing better after.

These shifts in market leadership underline why we think investors should target a diverse basket of stocks in the current environment. Our asset allocation for the next one to three years is overweight U.S. large-and mid-cap stocks, developed-market equities, and emerging-market equities too.

In our view, diversification allows exposure to a range of investment themes, from AI investment, to improving international earnings, to more attractive valuations. Moreover, it can help cushion shocks that might emerge to the macroeconomic and market outlook by spreading and diversifying risk across a wider group of companies and geographies.

Speak to your financial adviser to help ensure that your portfolio has appropriate diversification for the current environment, based on helping achieve your financial goals.

James McCann

Investment Strategy

All data in commentary sourced from Bloomberg, the Congressional Budget Office, and JP Morgan.

The Week Ahead

Important economic data and events for the week ahead include the Fed meeting, GDP, PCE inflation and Manufacturing PMI.

Previous weeks' weekly market wraps

James McCann

Senior Economist

Thought Leader In:

- Economic issues impacting the lives of everyday Americans.

- The effects of government spending, taxes and regulation changes on our clients.

- Building diversified portfolios to help investors reach their long-term financial goals.

“The economic, political and policy landscape is shifting dramatically, making it ever more challenging for our clients to navigate their personal finances. In this environment, it's our deep, research-driven insights that can help clients stay on track to reach their financial goals."

James McCann

Senior Economist

Important Information:

The Weekly Market Update is published every Friday, after market close.

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged and cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.