With Fed rate cuts off the table, bond yields are likely to stay higher for longer

Key takeaways

- Inflation has moved further above the Fed's 2% target, effectively removing the likelihood of rate cuts this year.

- As a result, bond yields are likely to remain elevated, with the 10-year Treasury staying near the upper end of our expected 4.0%-4.5% range for this year.

- Tax-exempt municipal bond yields have risen alongside taxable yields and remain above their historical average.

Fed rate cuts no longer the base case

The Fed's June economic projections signaled a modestly more hawkish stance, as policymakers raised inflation expectations and removed the previously forecast 2026 rate cut. However, officials remain divided on the path forward, suggesting the debate has shifted from when to cut to whether current policy can return inflation to target within a reasonable timeframe.

The Fed's preferred inflation gauge has risen further above the 2% target, partly reflecting higher energy prices. The headline figure moved above 4% in May, while core inflation increased more moderately, leaving the Fed with little room to ease policy.

Policymakers still expect headline inflation to return to target by 2028, indicating they believe the recent pickup is unlikely to become persistent. If inflation pressures remain concentrated mostly in energy, the Fed may be reluctant to respond aggressively to what could prove to be a temporary supply shock. But if energy costs feed into broader goods and services prices — or if long-term inflation expectations drift higher — policymakers may be more inclined to consider a hike.

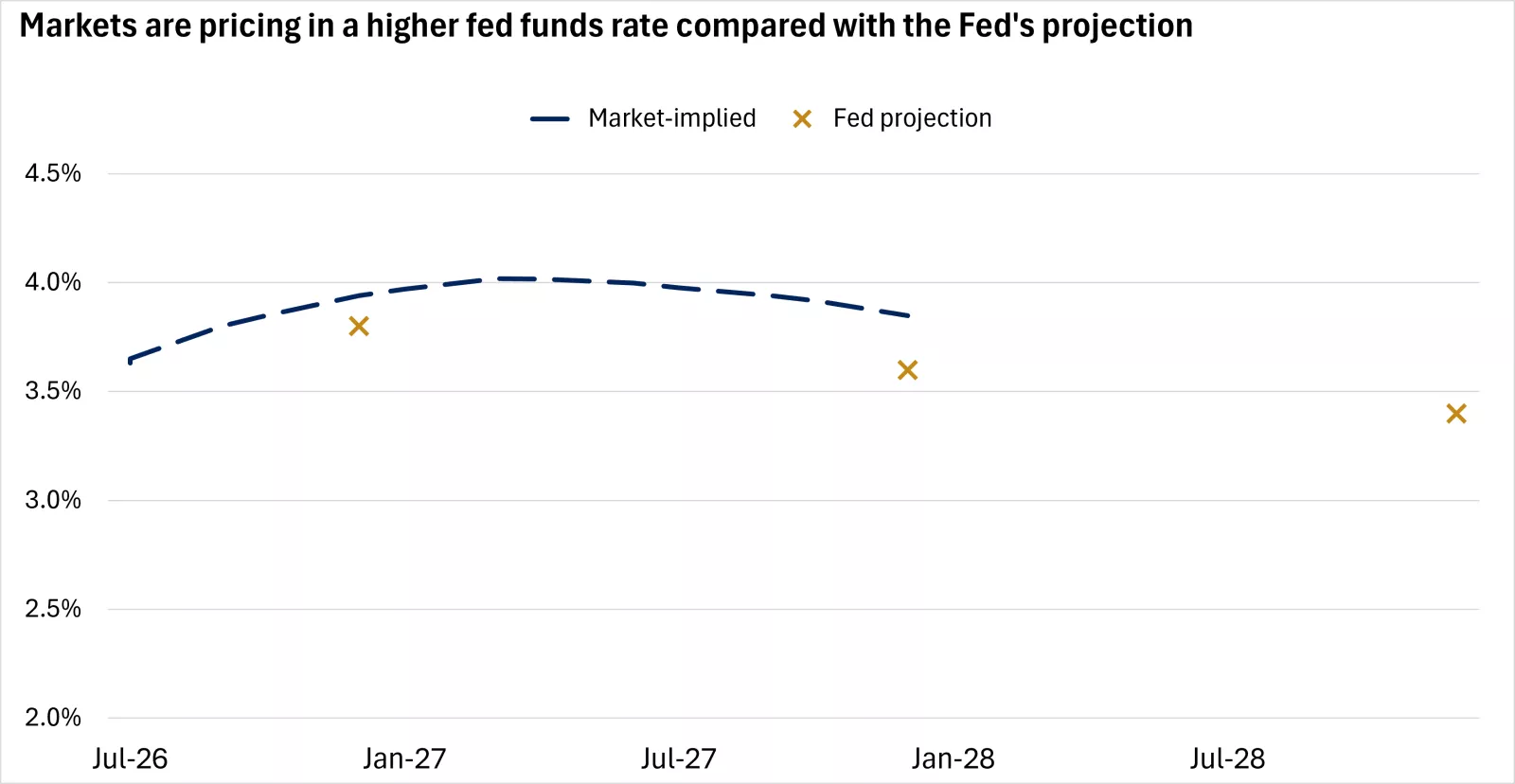

The inflation outlook could become more balanced if geopolitical risks continue to ease and oil prices remain lower. At the same time, the resilient labor market also gives policymakers more room to prioritize inflation risks, as the employment side of the Fed's dual mandate is largely being met. Overall, markets reflect some likelihood of a rate hike, shown in the chart below.

The chart shows that markets are pricing in a higher fed funds rate compared with the Fed's projections.

The chart shows that markets are pricing in a higher fed funds rate compared with the Fed's projections.

We believe a prolonged pause is the most likely outcome, as the Fed is unlikely to ease while inflation is moving higher, but there is not yet consensus among policymakers for tightening. Even if the Fed delivers a single rate hike, we believe markets would likely view it as a mid-cycle adjustment, rather than the start of a renewed tightening cycle, provided inflation expectations remain contained.

Bond yields likely to remain range-bound but elevated

With rate cuts likely off the table in the near term, the rate backdrop should remain higher for longer. The 10-year Treasury yield appears likely to remain near the upper end of our expected 4.0%-4.5% range. Moderating inflation expectations, helped by easing energy prices, could limit further upward pressure on yields. At the same time, resilient economic growth, a steady labor market and concerns over fiscal deficits should make a sustained decline in yields unlikely.

The result appears to be a range-bound but elevated yield environment. Meaningful bond rallies that push yields lower may require clearer evidence that inflation is moving back toward target or that the labor market is cooling enough to revive expectations of rate cuts. Importantly, higher yields improve income potential, the primary driver of bond returns.

Municipal bond yields are above historical average

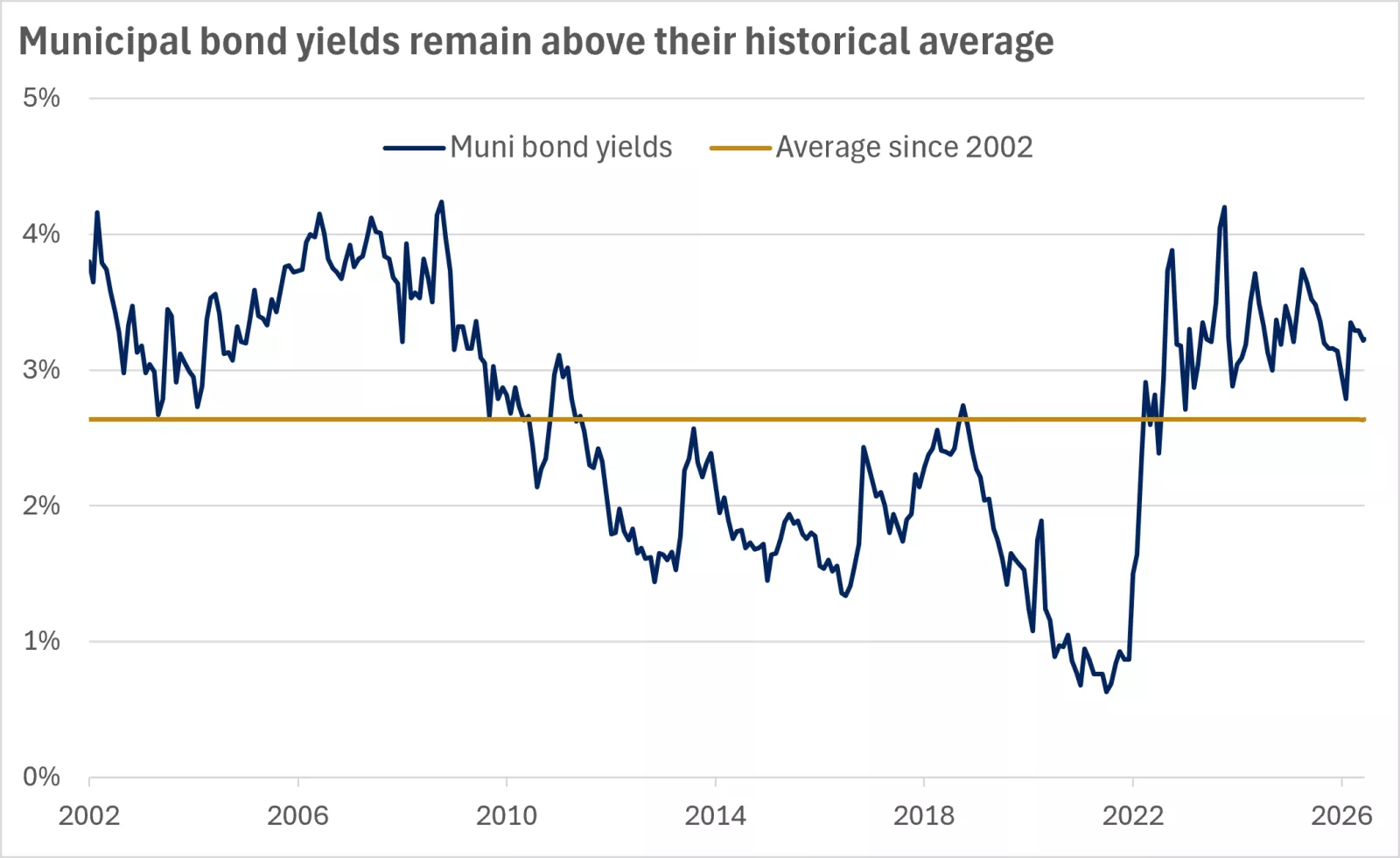

Municipal (muni) bond yields have moved higher alongside taxable bond yields and remain above their historical average, as shown in the chart below.

The chart shows the municipal bond yields are above their average since 2002.

The chart shows the municipal bond yields are above their average since 2002.

Higher yields mean that muni bonds can offer more income than they have in recent years, potentially presenting a more attractive entry point for investors, particularly those in higher income tax brackets.

A key benefit of municipal bonds is their tax efficiency. Interest on most muni bonds is exempt from federal income tax, and, in some cases, state and local taxes when issued in an investor's home state. As a result, high-income investors should focus not only on muni bonds' stated yield, but also on their after-tax value relative to taxable alternatives. On a tax-equivalent basis, muni bonds may provide a compelling mix of tax-efficient income, generally strong credit quality and portfolio diversification. The muni bond market can also be sensitive to supply-demand dynamics. If elevated borrowing costs lead some issuers to delay or reduce financing, more limited supply could help could support muni bond prices.

Brian Therien

Brian Therien is a Senior Fixed Income Analyst on the Investment Strategy team. He analyzes fixed-income markets and products, and develops advice and guidance to help clients achieve their long-term financial goals.

Brian earned a bachelor’s degree in finance from the University of Illinois at Urbana–Champaign, graduating with honors. He received his MBA from the University of Chicago Booth School of Business.

Important information:

This content is intended as educational only and should not be interpreted as specific recommendations or investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. Opinions are as of the date of this report and subject to change.

Past performance of the markets is not a guarantee of future results.

Before investing in bonds, investors should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decease, and the investor can lose principal value if the investment is sold prior to maturity.