As you plan for your next chapter, it’s important to understand how Social Security fits into your retirement income. Because it’s a guaranteed, lifetime benefit independent of the market, the timing of your claim deserves careful consideration.

The age you file for benefits affects the size of the benefit you receive. If you take your benefit when you’re first eligible (age 62), your benefit could be reduced by 30%. But if you delay to age 70, your benefit could be increased by up to 24%, based on full retirement age (FRA) of 67. FRA is the age at which you can receive 100% of your benefits. By taking Social Security at age 70, you can receive your largest benefit.

So, when should you file? It depends on your unique situation. However, you’ll want to consider these four key factors when making your decision about when to take Social Security benefits.

1. Need

Do you have limited means to meet your retirement income needs? If so, and you’re unable to defer retirement or reduce expenses, then it may make sense to take Social Security early. However, if you have flexibility over your retirement plans, delaying your Social Security benefits can help improve the likelihood your money lasts through retirement.

2. Employment

If you plan on working during “retirement” and start your benefit before your FRA, some of your benefit could be withheld, depending on your earned income. (Earned income doesn’t include income from investments, pensions or Social Security itself.) Even though your benefit will be adjusted at FRA if you have benefits withheld, depending on your life expectancy, you may not recover the full amount. So, if you plan on earning meaningful employment income in retirement, it typically makes sense to delay claiming.

3. Life expectancy

How long you (and your spouse) expect to live plays an important role. Your Social Security benefit acts as longevity insurance because it ensures you’ll receive a minimum income amount (with cost-of-living adjustments) no matter how long you live. The better your health and the longer you and your spouse expect to live, the more it may make sense to take Social Security later.

4. Spousal considerations

There are two types of benefits for spouses: a spousal benefit (paid while both spouses are living) and a survivor benefit (paid after one spouse passes). If your spouse files for benefits early, any potential spousal benefit available to them would also be reduced. Your decision can also impact your spouse — meaning, if you take benefits early and receive a reduction in benefits, the survivor benefit for your spouse would also be permanently reduced.

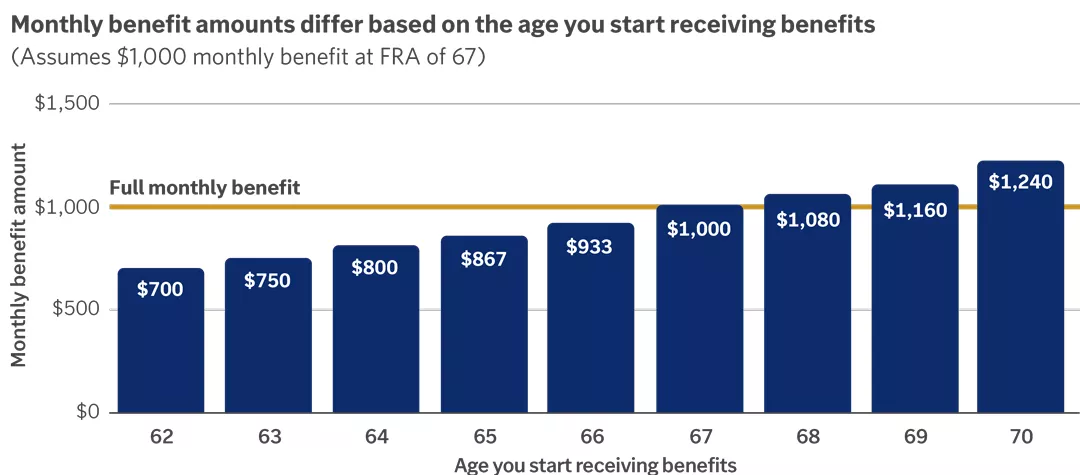

This chart shows how your monthly Social Security benefit differs based on the age you start receiving your benefits. Assuming a $1,000 monthly benefit at full retirement age of 67, you would receive $700 a month if you started receiving benefits at 62. But the benefit can increase incrementally to $1,240 a month — or a 24% increase — if you wait until age 70.

This chart shows how your monthly Social Security benefit differs based on the age you start receiving your benefits. Assuming a $1,000 monthly benefit at full retirement age of 67, you would receive $700 a month if you started receiving benefits at 62. But the benefit can increase incrementally to $1,240 a month — or a 24% increase — if you wait until age 70.

Visit your local Social Security office or www.ssa.gov for more information on your available benefits and options. The decisions you make about Social Security today can have a big impact on your income tomorrow.

Important information:

Content is intended as educational only and should not be interpreted as specific advice. Investors should make investment decisions based on their unique goals and financial situation. Edward Jones, its employees and financial advisors cannot provide tax or legal advice.