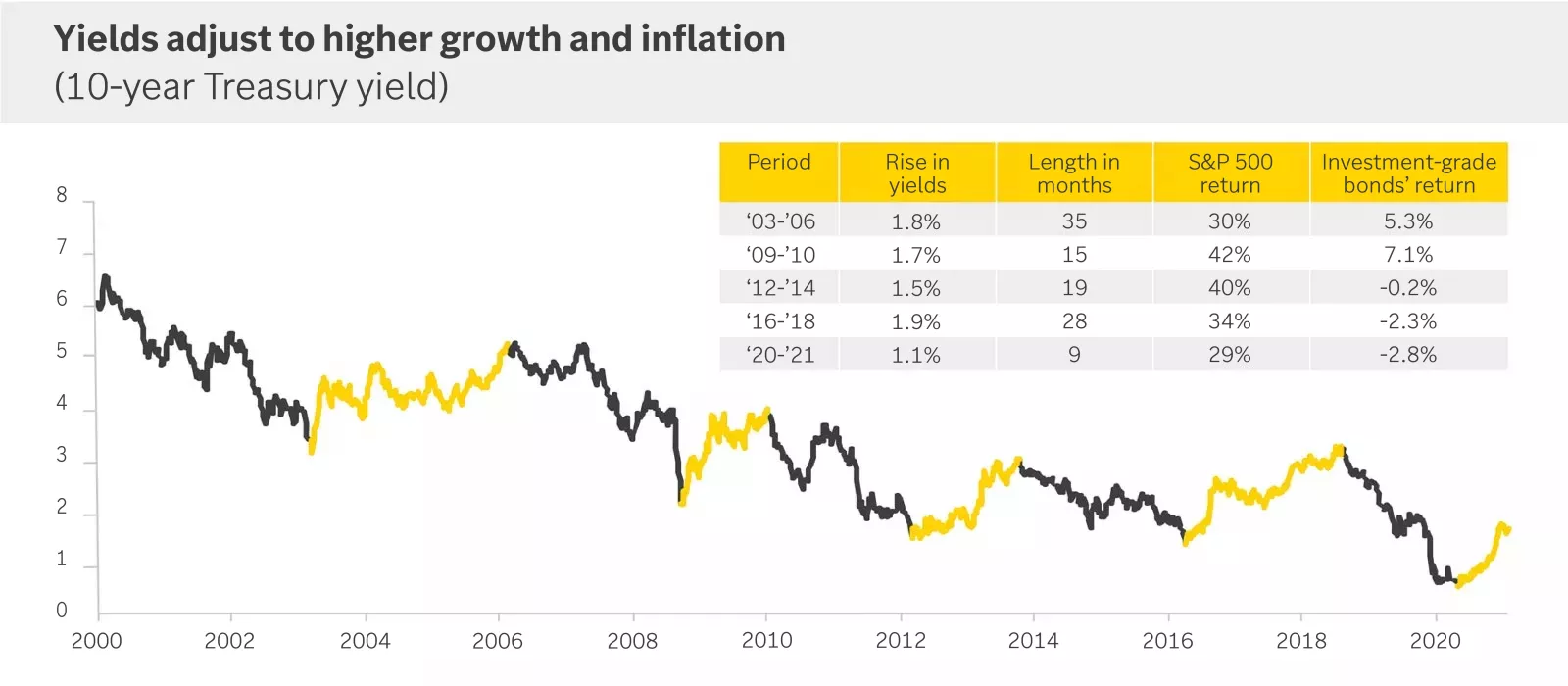

This chart illustrates how long-term interest rates have been moving lower since 2000. It shows five periods of rate increases within that time span and the S&P 500 return during each of those periods.

Short-term interest rates have remained near zero this year, anchored by the Federal Reserve’s support for the economic rebound. But longer-term rates have risen amid evidence of strong growth and the prospects of higher inflation, pressuring bond returns. For example, 10-year Treasury rates started 2021 below 1%, the lowest level to start a calendar year in history, but have since nearly doubled.

For investors wondering what this means for their stock and bond portfolio allocations, we’d offer three takeaways.

1. Rates have risen for the right reasons. Rising bond yields are typically associated with periods of accelerating growth and positive equity returns. Long-term rates have risen as growth and inflation have picked up. A healthier economy and rising demand produce higher inflation, so in our view, higher rates indicate confidence in the economic rebound.

Historically, stocks have performed better when rates are rising than when they are falling. Long-term interest rates have trended downward for more than 20 years, as shown in the graph below. But there have been five periods when benchmark 10-year rates rose noticeably. In those instances, the S&P 500 increased at a faster-than-average pace.

Source: FactSet, Edward Jones calculations as of 4/30/2021. Investment-grade bonds represented by the Bloomberg Barclays aggregate bond index.

2. “Higher” rates aren’t the same as “high” rates. The trajectory and speed at which rates rose earlier this year may have appeared abrupt. But this simply brought 10-year interest rates back to pre-pandemic levels, with 10-year yields still near historic lows. Now that we’ve returned to pre-pandemic GDP levels, we expect a maturing expansion to drive inflation pressures, which will eventually require Fed rate hikes. This will send longer-term interest rates to more restrictive levels. But in our view, we are several years away from higher rates posing a risk to the economy.

In the meantime, as the Fed keeps short-term rates pinned to zero and long-term rates will likely rise modestly, the yield curve – the difference in yields between short- and long-term bonds – will continue to steepen. A steepening yield curve has historically helped the relative performance of financials and other cyclical sectors.

3. Bonds can still add value in a rising rate environment. We believe that even when rates are rising, you should maintain an appropriate allocation to fixed income within your portfolio. Bonds can help provide a relatively predictable stream of income. They also can act as a portfolio stabilizer, helping to smooth out returns during times of market volatility.

A bond’s coupon payments and credit quality don’t change when interest rates rise. But bond prices fall as new bonds are issued with a higher interest rate. While longer-term bonds typically provide higher yields, they also come with greater interest rate risk.

A balanced fixed-income portfolio with short-, intermediate- and long-term bond maturities – known as bond laddering – can help position your fixed-income portfolio as interest rates change. We also recommend including an appropriate allocation to investment-grade and high-yield bonds. While these bonds carry the risk of increased credit exposure, they have historically improved portfolio returns in periods of accelerating economic growth.

Key points for investors

- As the economy gains traction, the path of least resistance for long-term rates will be higher, in our view. But they likely will not rise at the same trajectory as they did recently.

- You should expect periodic setbacks as the recovery advances. But with economic, policy and corporate financial conditions still aligned to the earlier stages of the business cycle, we think increases in rates from recent historic lows represent a short-term risk to the current rally, not a more structural threat to the broader expansion.

- If you’re concerned about changing market conditions, talk with your financial advisor. He or she can help ensure your portfolio is properly diversified. Exposure to cyclical sectors, which can benefit from a steepening of the yield curve, and bond laddering can help you successfully navigate the shifting investment landscape ahead.

Angelo Kourkafas

Angelo Kourkafas is responsible for analyzing market conditions, assessing economic trends and developing portfolio strategies and recommendations that help investors work toward their long-term financial goals.

He is a contributor to Edward Jones Market Insights and has been featured in The Wall Street Journal, CNBC, FORTUNE magazine, Marketwatch, U.S. News & World Report, The Observer and the Financial Post.

Angelo graduated magna cum laude with a bachelor’s degree in business administration from Athens University of Economics and Business in Greece and received an MBA with concentrations in finance and investments from Minnesota State University.