Health care is one of the largest expenses a retiree will face, and many worry about being able to afford it. To help you enter retirement confidently, follow these steps to create a health care strategy — a strategy that can help you cover the costs for the health care you want and need.

Health care continues to become a larger share of retirees’ expenses.

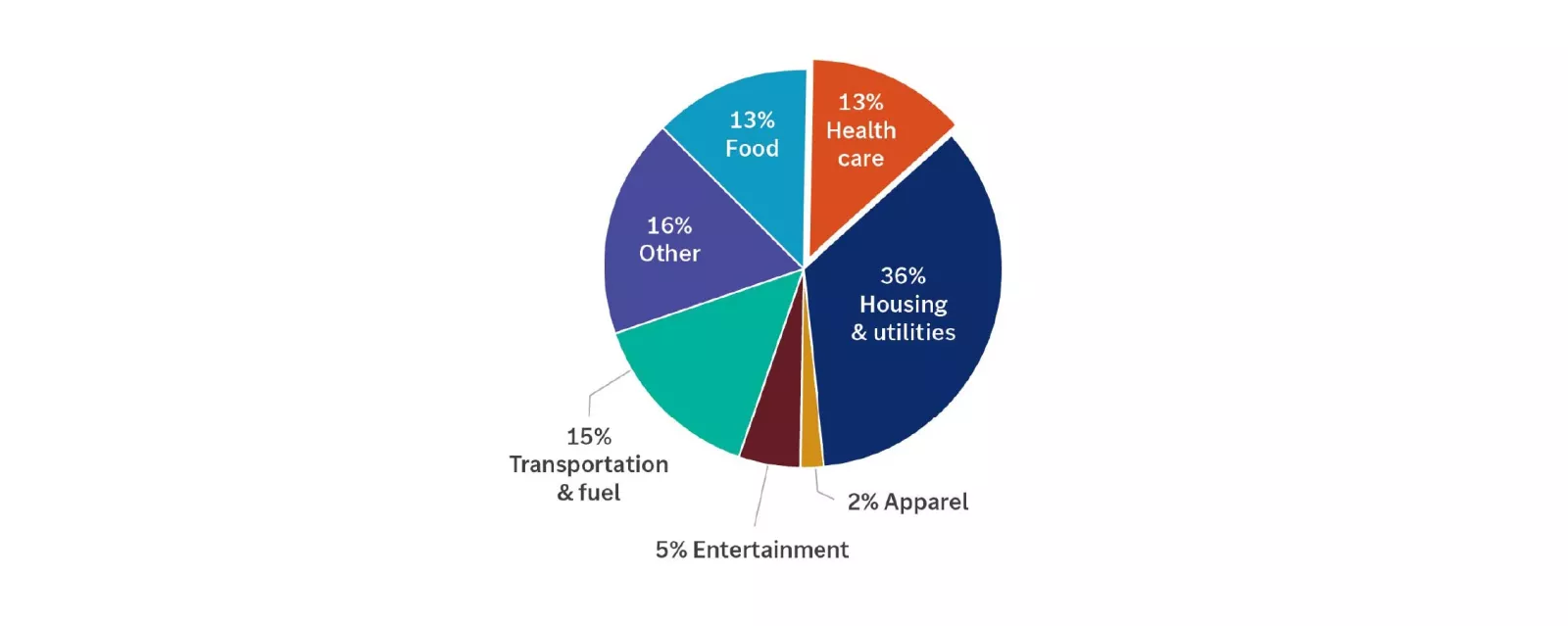

Retiree household expenditures

This pie chart shows the average expenditures for a household ages 65 and older: 13% of expenses go to health care, 13% to food, 36% to housing and utilities, 2% to apparel, 5% to entertainment, 15% to transportation and fuel, and 16% to other.

This pie chart shows the average expenditures for a household ages 65 and older: 13% of expenses go to health care, 13% to food, 36% to housing and utilities, 2% to apparel, 5% to entertainment, 15% to transportation and fuel, and 16% to other.

Explore your ability to contribute to a health savings account (HSA)

If you’re eligible to contribute to an HSA and can afford to save (rather than spend) the contributions, you’ll have a powerful tool to help cover your health care costs in retirement.

HSAs come with many advantages:

- They’re triple-tax exempt, meaning allowable contributions are exempt from federal taxes, earnings growth is tax-free, and distributions are tax-free when used for qualified medical expenses. This gives them more tax advantages than other retirement accounts when used for qualified medical expenses.

- Many offer the option of investing the funds, which provides the potential for growth.

Have a plan for any health insurance need before Medicare eligibility at age 65

Most people won’t be eligible for Medicare before age 65, but many retire before then. Finding health insurance during that gap may be expensive, but not having coverage could be even more costly and lead to negative effects to your health and well-being.

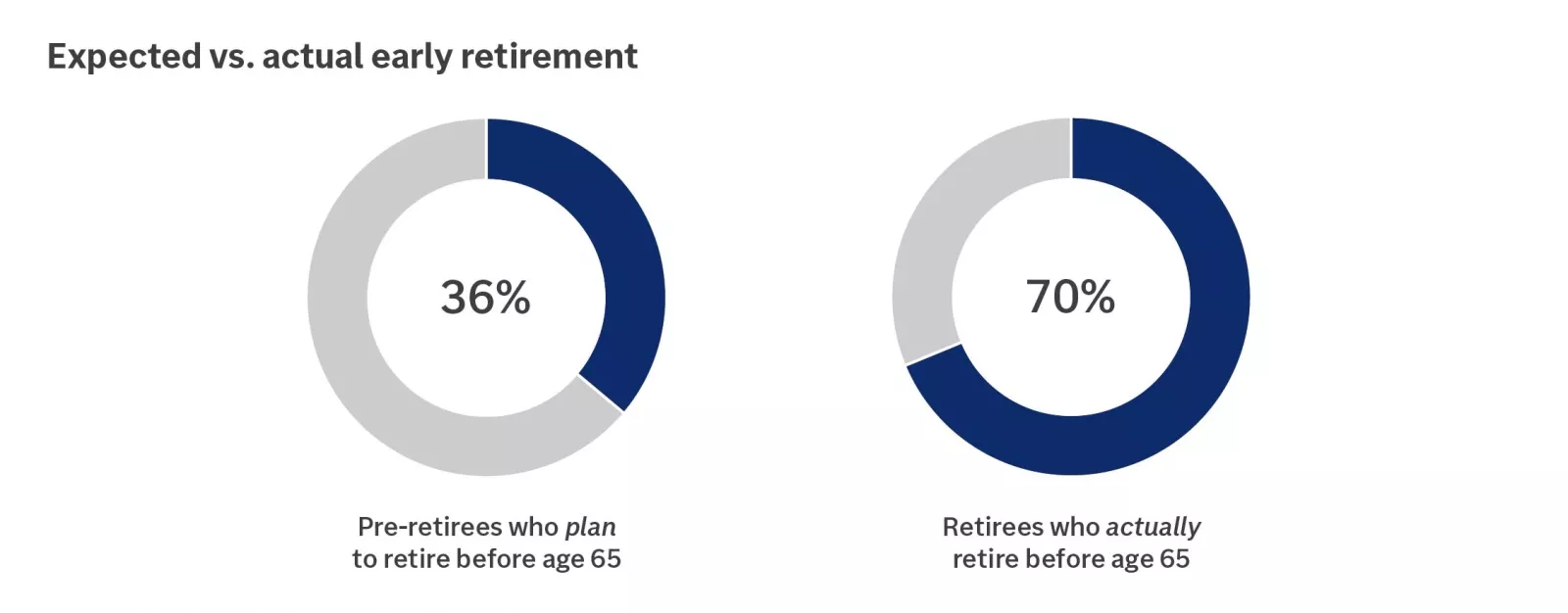

This chart shows only 36% of pre-retirees plan to retire before age 65, but 70% of retirees actually retire before age 65.

This chart shows only 36% of pre-retirees plan to retire before age 65, but 70% of retirees actually retire before age 65.

There are four commonly available options we recommend exploring:

- Retiree health benefits — Insurance your employer provides to retired workers

- Spouse’s plan — Insurance from your spouse’s plan if they’re still working or have access to retiree benefits

- COBRA — Continuation of current coverage for a set time after leaving an employer plan

- Marketplace plan — Exchanges where individuals can buy health insurance (also called Affordable Care Act or Obamacare plans)

When comparing options, we recommend considering coverage, cost and eligibility to contribute to an HSA.

Ensure you’re building traditional health care costs into your retirement plan

Pre-Medicare

If you’re planning to retire early , ensure you can cover the cost of health care in the years before you’re eligible for Medicare (age 65 for most individuals).

If you’re still many years from retirement, you can start by estimating around $10,000 per year per person if you believe you’ll have access to a workplace or retiree plan, or around $15,000 per year per person if you’ll be relying on a marketplace plan. A financial advisor can help you adjust from there if needed.

Medicare

A good starting point is to initially budget $4,500 to $6,500 per person annually once you’re eligible for Medicare.

Then you’ll want to make some adjustments:

- If you’re getting close to enrollment, you can search for Medigap or Medicare Advantage plans in your area to get a more precise estimate of what your costs might be. Keep in mind that Medigap premiums tend to be higher than Medicare Advantage premiums, but Medicare Advantage users tend to have larger out-of-pocket costs, especially in years of heavy health care use.

- If you’ll have high income in retirement, you may need to incorporate Medicare surcharges known as income-related monthly adjustment amounts, or IRMAA .

- Finally, increase the amount to account for inflation that will likely occur between now and when you’ll enroll in Medicare. We generally recommend assuming health care costs increase by 3% to 5% each year.

Develop a strategy to meet long-term care expenses (ideally between ages 50 and 60)

Medicare coverage is extremely limited for long-term care, so we don’t recommend relying on it for long-term care needs. Because long-term care events are increasingly likely the longer you live — and can be very costly — everyone should have a plan in place to cover a long-term care need. While we generally recommend starting to plan for the need between ages 50 and 60, some may prefer to start earlier, and it’s never too late!

We recommend planning for $150,000 of care per person as a starting point, which is based on receiving two to three years of care with increasing levels of care support.

Once you have a sense of how you’d want to receive long-term care and how much it may cost, you’ll want to discuss the options for covering those costs. That could include a combination of:

- Self-insuring — Using your own income or assets to cover long-term care expenses

- Traditional long-term care insurance — A long-term care insurance policy that pays for long-term care expenses

- Life insurance with:

- Hybrid/linked benefit — Uses the death benefit plus an additional amount to pay for long-term care expenses

- Chronic illness riders — Uses only the death benefit to pay for long-term care expenses

A financial advisor can help you understand the risks of a long-term care event, customize long-term care estimates and walk through the benefits and trade-offs of the different options available for covering those costs.

Before age 65, understand your Medicare options and deadlines for enrollment

Most people will become eligible for Medicare at age 65.

- If you’re planning on retiring before then, you’ll likely want to enroll at age 65. Start understanding deadlines and exploring your Medicare options about a year before you plan on enrolling.

- If you’re retiring later, you may still want to enroll in some parts of Medicare at age 65. You should verify your ability to delay enrolling in Medicare with your employer and understand what special enrollment periods you’ll qualify for. Even if you can delay, you may want to explore whether Medicare coverage would be more advantageous than your current coverage.

Meagan Dow

Meagan Dow is a senior strategist on the Advice & Planning Research team at Edward Jones. The Advice & Planning Research team develops and communicates advice and guidance for financial planning needs, including retirement, healthcare, preparing for the unexpected and leaving a legacy. Meagan has over 15 years of financial services and investment experience. She is a contributor to the Edward Jones Perspective newsletter and has been quoted in various publications.

Important information:

This content is meant as educational only and is not intended for other than broadly informational purposes. The information has been prepared from sources and data we believe to be reliable, but we make no guarantee to its accuracy or completeness.