Highlights

| • Passive and active management: the basics |

| • Passive vs. active: Benefits and trade-offs |

| • When should you consider passive management? |

| • When shouldn’t you consider passive management? |

| • Which style will outperform? |

| • Does active perform better than passive in some asset classes? |

| • How should you allocate your assets? |

Passive and active management: The basics

What's the difference between active and passive investing?

At the most basic level, these investment approaches can be summarized in this way:

- Active investments seek to do more than just match the performance of an index — they attempt to outperform the market, target less investment risk or produce more income.

- Passive investments seek to match the performance of an entire asset class, an asset-class investment style (such as value and growth styles in equities) or a sector by replicating the returns of a specific index.

Typically, passive funds own many of the same securities, and in the same weightings, as their respective indexes. Passive fund managers make no “active” decisions, potentially resulting in less trading, which reduces fund expenses and potential taxable distributions to shareholders. The performance of a passive fund should mirror the index it’s tracking, which means the fund will share the ups and downs of the index.

In contrast, an active manager will seek to outperform an index by achieving a higher return, taking less risk or combining these two objectives. Because active fund managers choose investments, they have the potential to outperform the market on the upside and limit losses when the market declines, relative to the index. However, there is no guarantee that an actively managed fund will outperform its index.

The table below summarizes the key benefits and trade-offs of these investment approaches. (An index is not managed and is unavailable for direct investment.)

Passive vs. active: Benefits and trade-offs

| Passive | Active |

|---|---|---|

| Benefits | • Likely to perform close to index | • Opportunity to outperform index |

| Trade-offs | • Unlikely to outperform index | • Potential to underperform index |

When should you consider passive management?

If the idea of lower expenses and the potential for better tax efficiency appeals to you, then a passively managed investment may be appropriate. However, with these benefits comes the trade-off of receiving index-like returns — on the upside and the downside.

When shouldn’t you consider passive management?

If the thought of participating in all the downside of the market is unnerving to you, then you may be better served by investing in an actively managed fund that has at least the potential to limit the downside (although this is no guarantee). This potential does come at a higher cost, since the annual expenses of most active funds are generally greater than those of passively managed funds.

Which style will outperform?

Many studies* have tried to determine whether the active or passive management style will outperform over time. These studies indicate the following:

- Performance may vary, depending on the asset class.

- Performance may move in cycles — and there will probably be years when even the “best-performing” style may not have positive returns relative to a passive strategy.

In evaluating whether active or passive management outperforms, it’s important to realize that the asset class can often influence the results. For example, some asset classes, such as large-cap equities or investment-grade fixed income, are larger and more established, which might make it harder for an active fund manager to outperform the index. Remember, this doesn’t mean active management doesn’t work in certain asset classes — many active managers outperform regardless of their asset class. It just means it can be more challenging to find managers who might outperform in certain asset classes.

On the other hand, active portfolio managers may have a greater opportunity to outperform with small-cap, mid-cap or international equities. Information on stocks in these asset classes is likely to be less widely available, creating an opportunity for managers to conduct deeper analysis to outperform, although that outcome is certainly not guaranteed.

Performance may move in cycles — not only does the outperformance of active or passive management often vary by asset class, but it can also vary based on the market environment. For example, when the market has momentum and is showing strong returns, it might be more difficult for actively managed funds to keep up with the index. This is because these funds hold different securities from the index, as well as small amounts of cash. However, in weak or declining markets, active managers’ funds might have the potential to hold up better, perhaps by becoming more conservatively positioned when markets become choppy.

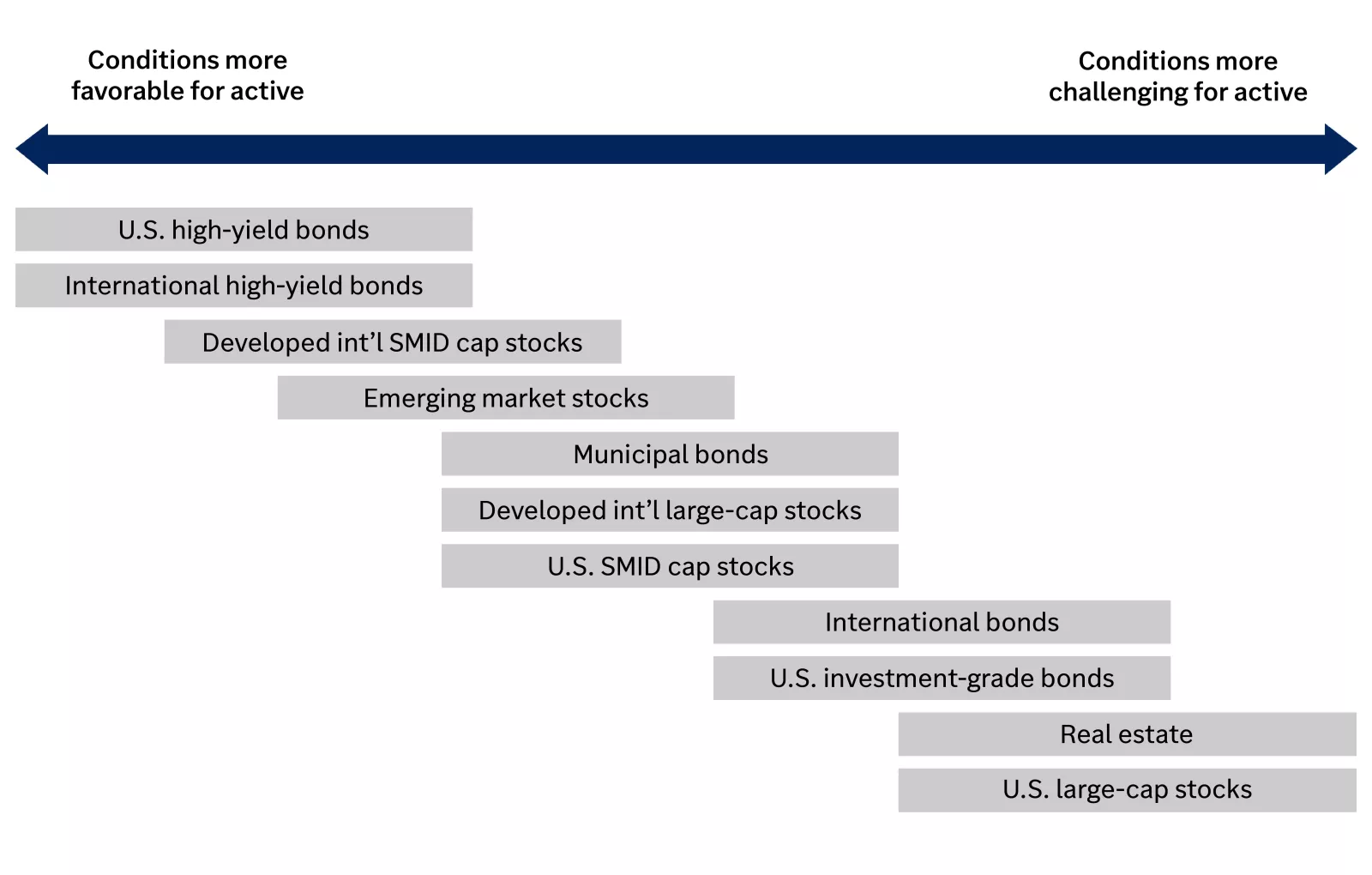

Does active perform better than passive in some asset classes?

The graphic below illustrates our assessment of the range of conditions over a market cycle for the average active manager in each asset class. Some areas of the market, such as international small- and mid-cap (SMID cap) stocks or international high-yield bonds, tend to offer more favorable conditions for active management compared with asset classes such as U.S. large-cap stocks or U.S. investment-grade bonds. Active managers in international SMID caps are more likely to select stocks that will outperform. Why? Because with fewer research analysts covering each stock in the sector, less information is incorporated into each stock’s price, leaving room for upside surprises. In other asset classes, such as international high-yield bonds, the index may not represent the entire opportunity set in the asset class, which allows active investment strategies to benefit from investing in bonds not included in the index.

When building your portfolio, you may want to consider active approaches in the asset classes that provide more favorable conditions for active management. In turn, consider passive investments in the asset classes that are more challenging for active management.

This chart shows a range of conditions that are more favorable for active investing (starting on the left) through conditions that are more challenging for active investing (on the right). Beginning with the most favorable conditions for active investing moving to the least favorable conditions for active investing, they are (in order): U.S. high-yield bonds, international high-yield bonds, developed international SMID cap stocks, emerging market stocks, municipal bonds, developed international large-cap stocks, U.S. SMID cap stocks, international bonds, U.S. investment-grade bonds, real estate and U.S. large-cap stocks.

How should you allocate your assets?

Consideration | Lean Passive | Lean Active |

|---|---|---|

| Performance objectives | Want to match the returns of the market | Want to try to outperform the market |

| Sensitivity to costs | Focused on minimizing costs of investment products | Willing to pay a relatively higher cost to pursue a higher return |

| Tax situation | Taxable accounts | Tax-deferred accounts |

Determine what’s most important to you

We believe active and passive management can play a role in your portfolio. It’s really about evaluating what you want from an investment and prioritizing what is most important to you. We recommend you talk with your financial advisor to help determine which investments are most appropriate for you. Exchange-traded funds and mutual funds are offered by prospectus. You should consider the investment objective, risks, charges and expenses carefully before investing. The prospectus contains this and other information, which your Edward Jones financial advisor can provide; please read it carefully before investing. Your investment return and principal value will fluctuate, and you may lose money.

If you do not have a financial advisor with whom to discuss your investment objectives, take the Edward Jones Match Quiz to match with financial advisors who are available to answer your questions.

Investment Policy Committee

The Investment Policy Committee (IPC) defines and upholds Edward Jones investment philosophy, which is grounded in the principles of quality, diversification and a long-term focus.

The IPC meets regularly to talk about the markets, the economy and the current environment, propose new policies and review existing guidance — all with your financial needs at the center.

The IPC members — experts in economics, market strategy, asset allocation and financial solutions — each bring a unique perspective to developing recommendations that can help you achieve your financial goals.

Important Information:

* “The Case for Indexing,” Vanguard Investment Counseling & Research. Copyright 2009, The Vanguard Group.

Diversification does not guarantee a profit or protect against loss.