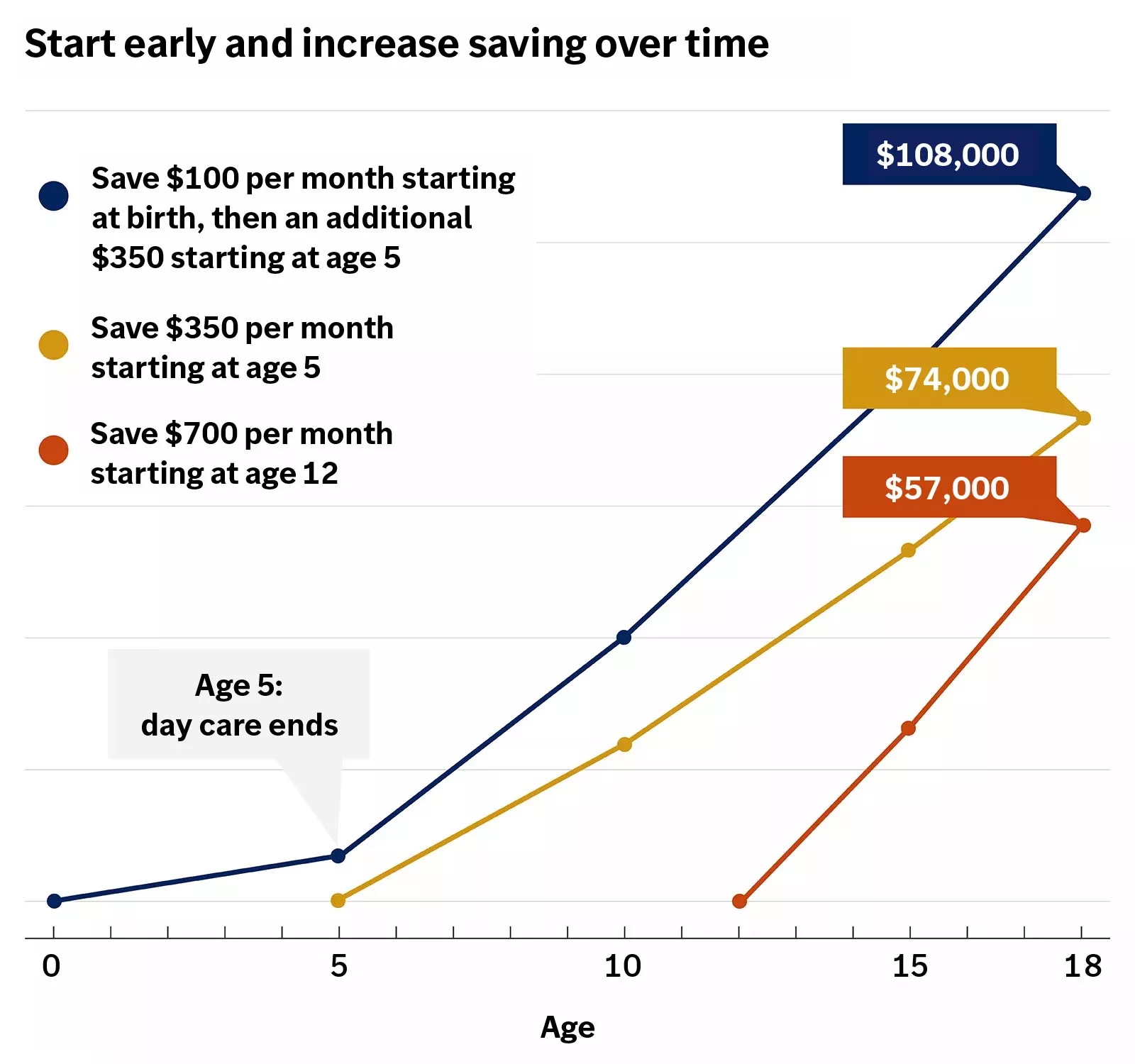

Opening an education savings account, saving early and saving often are great ways to help earmark money for your child’s tuition costs.

A 529 Plan, or the variety of other available education savings options, can offer tax benefits, too. Some families worry that saving for college may hurt their chances of receiving financial aid. In reality, 529 plans and many other education savings options are considered parent-owned assets, meaning only a small percentage of the savings (less than 6%) are reflected in the financial aid calculation. The key is to identify which account is right for you and when to start saving, while keeping your other financial goals on track.

How much should I save in a college fund for my kids?

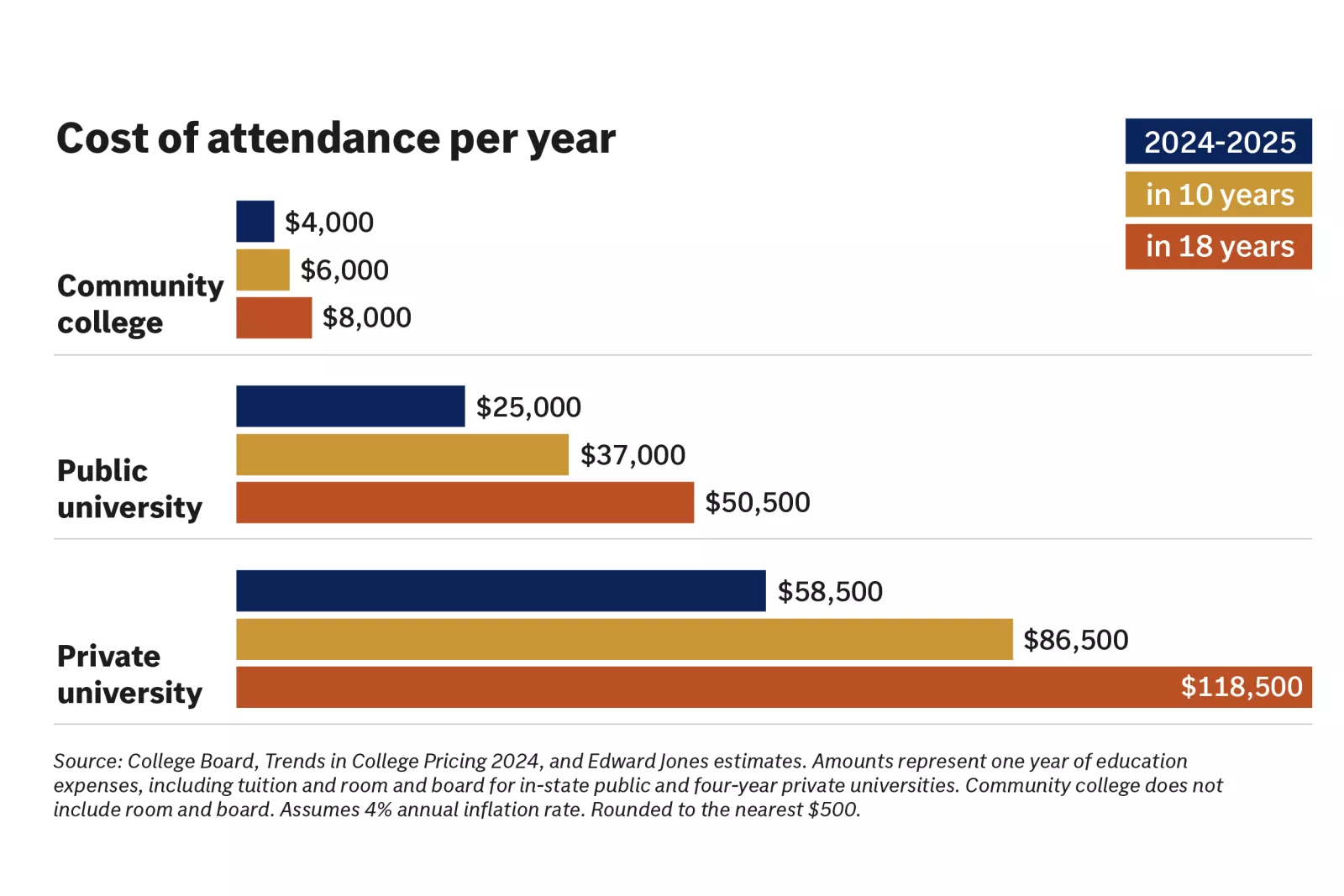

Before diving into what college savings approach is best for you, think about what type of school you want to plan for (private, public, vocational, postgraduate), the associated costs (see the chart below) and how much you want to cover.

Will you pay for:

- All your child’s college expenses?

- Half of everything?

- Tuition but not room and board?

While there isn’t one right answer, you should decide what works best for your family’s personal and financial situation. The table below outlines the cost of attending three types of institutions forecasted 10 and 18 years into the future. Understanding ballpark costs depending on which type of school you want your children to attend can help drive the amount you need to save each month to meet your goals. Your financial advisor can help you determine how much college may cost, as well as how the savings may affect your other goals.