Saving for retirement? Saving for college?

This doesn’t have to be an either/or proposition.

It can be overwhelming to think about how much you should save for college and retirement — but it doesn’t have to be. Your financial advisor can help you understand how the choices you make today about college savings may have an impact on your retirement.

We start by defining your savings goals for education and retirement, then determine if you’re likely to be able to fund them both completely. If you can, great. If not, we can revisit your goals and options for saving.

Outlining your priorities and understanding the trade-offs

A dollar put toward college is one less dollar saved for your retirement. So, how do you strike the right balance? It’s all about priorities and trade-offs. Depending on your values and priorities, you may be more willing to revisit:

- The amount you plan to provide for your child’s education: Explore if more affordable education (such as community college or in-state public school) would be acceptable alternatives. Or if you’re committed to a particular school or path for your student, consider partially funding it, with your student taking on responsibility for the remaining cost.

- When you retire: Would you be willing to work for a few more years? Delaying retirement gives you additional years to save, and means you have less to save for (because you have fewer years of retirement to fund).

- Your vision for your retirement: What would retirement look like with less saved, and would it meet your lifestyle standards? You could reduce your savings goal for retirement if funding a larger portion of your child’s college is a priority.

- The amount you’re saving: If you don’t want to compromise on your future goals, you can revisit your current spending to see if there’s an option to save more.

Your financial advisor can help talk through these options and how each affects your goals and the likelihood of achieving them.

Consider the following example

Jim and Mary Thompson are 32 years old and plan to save for retirement and start a college fund for their newborn, Lillian. Based on their financial situation, they determine they can save $1,100 a month, which will be divided between the two goals. Their financial advisor calculated the following required monthly savings to achieve each of their goals:

Possible savings scenarios

Retirement goal | Education goal |

|---|---|

| Retire at age 65 with $50,000 in annual income from the portfolio. | Provide $110,000 toward Lillian's education (estimate to cover two years of community college and two years at a public university). |

| Required monthly savings: $1,000 | Required monthly savings: $325 |

To cover both goals, the Thompsons would need to save almost $1,325 per month. However, because they can save only $1,100 per month, they are discussing options and trade-offs.

Retirement, education or both?

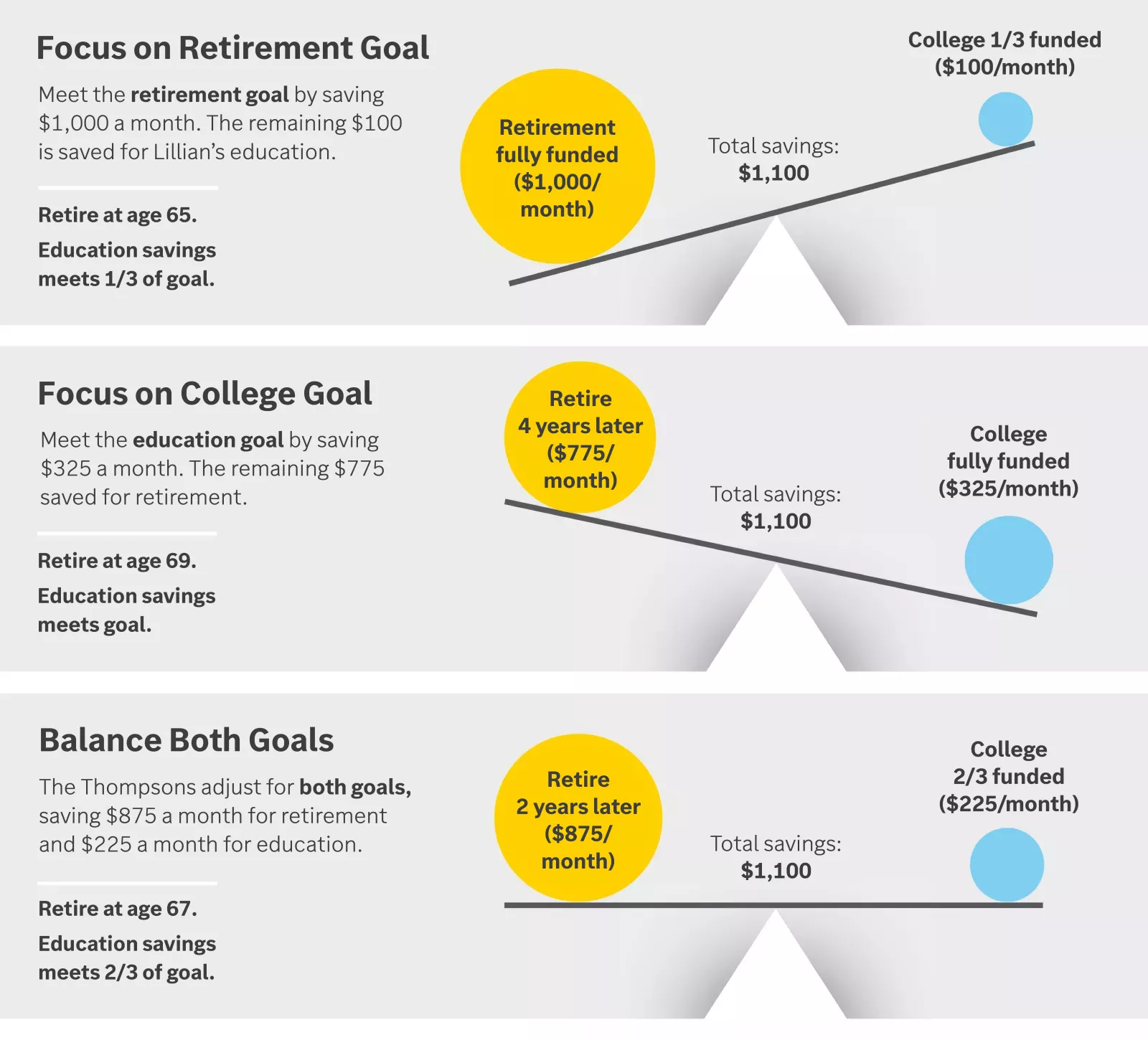

These charts illustrate three savings scenarios. The total monthly savings in each scenario is $1,100, but the difference is how that money is split between retirement and education. In the first scenario, retirement is a priority, so $1,000 goes to that goal while $100 is saved for education. The goal of retiring at age 65 is met, while approximately one-third of the $110,000 education goal is met. In the second scenario, education is a priority, so $325 goes to that, while $775 is saved for retirement. The $110,000 savings goal for education is met, while retirement is delayed until age 69. The third scenario aims to balance retirement and education. So, $875 is saved for retirement and the rest, $225, goes to education. Retirement comes a little later (age 67) and two-thirds of the original $110,000 is saved for education.

Assumptions: Retirement portfolio must provide $50,000 in income, using a 4% initial withdrawal rate. Retirement savings assume 6% annual return. Education savings assume 5.5% annual return through age 8, then 4.5% through age 16, and then 3.5% through age 18. Past performance is not a guarantee of future results. Graphic is for illustrative purposes only and does not reflect any currently available investments. Results rounded to the nearest $5,000.

These charts illustrate three savings scenarios. The total monthly savings in each scenario is $1,100, but the difference is how that money is split between retirement and education. In the first scenario, retirement is a priority, so $1,000 goes to that goal while $100 is saved for education. The goal of retiring at age 65 is met, while approximately one-third of the $110,000 education goal is met. In the second scenario, education is a priority, so $325 goes to that, while $775 is saved for retirement. The $110,000 savings goal for education is met, while retirement is delayed until age 69. The third scenario aims to balance retirement and education. So, $875 is saved for retirement and the rest, $225, goes to education. Retirement comes a little later (age 67) and two-thirds of the original $110,000 is saved for education.

Assumptions: Retirement portfolio must provide $50,000 in income, using a 4% initial withdrawal rate. Retirement savings assume 6% annual return. Education savings assume 5.5% annual return through age 8, then 4.5% through age 16, and then 3.5% through age 18. Past performance is not a guarantee of future results. Graphic is for illustrative purposes only and does not reflect any currently available investments. Results rounded to the nearest $5,000.

In our example, the Thompsons had to make some trade-offs. You may or may not need to do the same. Your answer lies with how you prioritize your goals.

Importantly, we don’t recommend putting off saving for retirement because you’re putting money away for college. This could put your retirement goal in jeopardy. Remember, loans and grants exist for college but not for retirement.

How we can help

At Edward Jones, we understand your life is a series of overlapping decisions. Your financial advisor will ask questions and really listen to understand your situation and develop a strategy to address what’s important to you.