For a program almost every retiree will use, Medicare can be puzzling. There can be penalties or gaps in coverage if you don’t sign up on time, there’s an alphabet soup of parts and plans to try to navigate, and some decisions — once made — can be difficult to reverse. Here are some key considerations to keep in mind as you prepare to enroll for Medicare the first time.

Understanding the parts of Medicare

Before enrolling, it helps to understand the various parts of Medicare and how they fall into essentially two paths for Medicare enrollees: Original or Advantage.

Original Medicare starts with government-provided plans through Part A (hospital insurance) and Part B (medical insurance). Unless you have other coverage (such as retiree insurance through a former employer), we recommend supplementing this coverage with private plans: a Medigap policy, a Part D prescription plan and dental and vision insurance plans, if possible.

Medicare Advantage takes many of these components and bundles them in a private plan known as Part C. Most of these plans include prescription coverage, and many include benefits like dental and/or vision. If you don’t otherwise qualify for prescription coverage, we recommend selecting a plan that includes it.

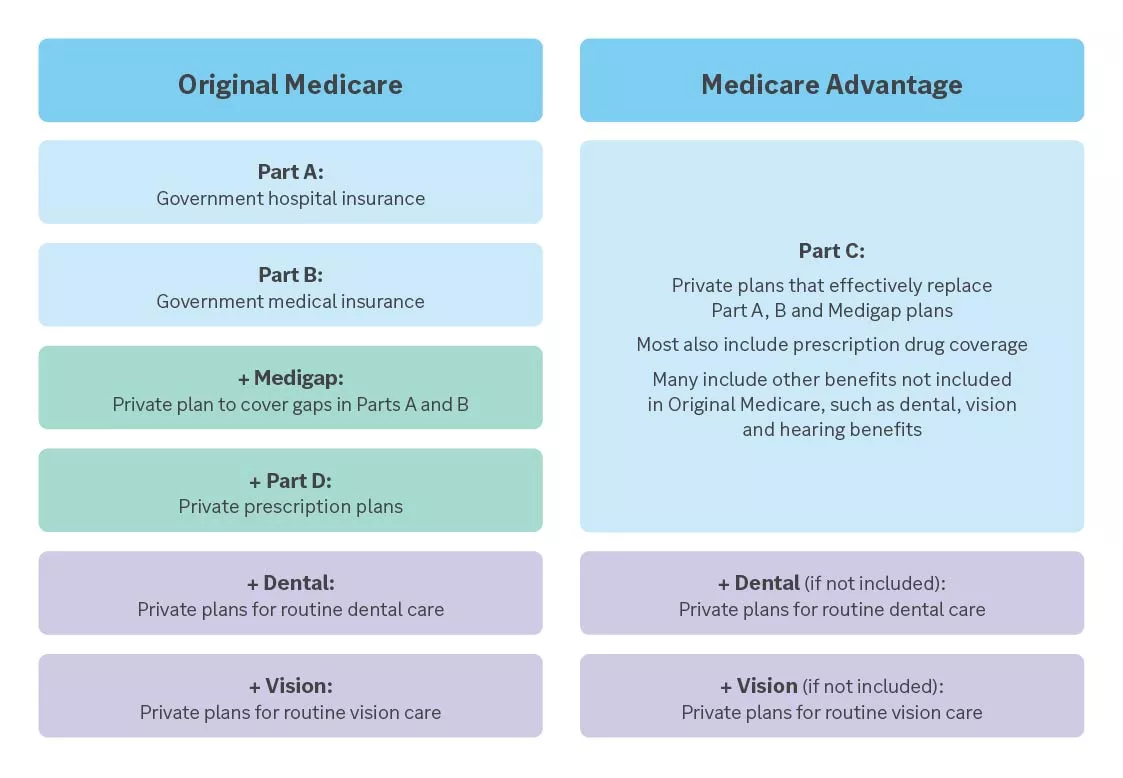

The above table shows two paths for Medicare coverage:

The first path is Original Medicare, which consists of Parts A (government hospital insurance) and B (government medical insurance). To be adequately insured with Original Medicare, we believe you need to add a Medigap plan to cover the gaps in Parts A and B, and a Part D plan for prescription drug coverage. To be fully insured, we believe you also need to add a dental and vision plan for routine dental and vision care.

The second path is Medicare Advantage, which (when it includes prescription drug coverage) is meant to replace Parts A and B as well as a Medigap plan and Part D plan. This may also include other benefits not included in Original Medicare. We believe you still need dental and vision coverage, which can be purchased as private plans if not included, to be fully insured with Medicare Advantage.

The above table shows two paths for Medicare coverage:

The first path is Original Medicare, which consists of Parts A (government hospital insurance) and B (government medical insurance). To be adequately insured with Original Medicare, we believe you need to add a Medigap plan to cover the gaps in Parts A and B, and a Part D plan for prescription drug coverage. To be fully insured, we believe you also need to add a dental and vision plan for routine dental and vision care.

The second path is Medicare Advantage, which (when it includes prescription drug coverage) is meant to replace Parts A and B as well as a Medigap plan and Part D plan. This may also include other benefits not included in Original Medicare. We believe you still need dental and vision coverage, which can be purchased as private plans if not included, to be fully insured with Medicare Advantage.

Steps for enrolling in Medicare

- Understand when you should sign up for the different parts of Medicare.

- Determine which path of Medicare (Original or Advantage) you want to choose.

- Determine which plans/policies within that path you want enroll in.

- If contributing to a health savings account (HSA), understand how Medicare impacts eligibility.

- Use your enrollment windows to enroll in the different parts of Medicare.

Understand when you should sign up for the different parts of Medicare

Those who delay signing up for Medicare can potentially face lifelong penalties as well as gaps in coverage. It’s critical to know your enrollment windows and whether you can delay without penalty.

When to sign up for Parts A and B

If you’re receiving Social Security benefits at least four months before you turn 65, you’ll be automatically enrolled in Parts A and B.1

If you aren’t receiving Social Security benefits at least four months before you turn 65, you should sign up for Parts A and B in the three months before turning 65 unless:

- You or your spouse is actively working for an employer with 20 or more employees AND

- You’re receiving health insurance from that employer

If you or your spouse is actively working past age 65 for an employer with 20 or more employees and you're getting health insurance through that employer, you can delay signing up for Parts A and B past age 65 (although you may not want to). Once you retire (or your spouse does, if that’s where you’re getting coverage), you’ll have an eight-month special enrollment period to enroll in Parts A and B.

If you’re enrolling in Original Medicare:

Part D:

- If you don’t have creditable drug coverage (drug coverage as good as or better than the minimum requirements for a Part D prescription drug plan), you should sign up in the three months before turning 65.

- If you have creditable coverage and want to delay enrolling, you’ll qualify for a special enrollment period that lasts two months after you lose creditable coverage.

Medigap:

- If you enroll in Parts A and B at age 65 and want a Medigap policy, you should enroll during your Medigap Open Enrollment Period. It lasts for six months starting the first month you have Medicare Part B and are 65 or older.

- If you have employer (working, retiree or COBRA) or union coverage and want to delay enrolling, you’ll qualify for enrolling in a Medigap plan without answering health questions for 63 days after you lose coverage or receive notice that your coverage is ending, whichever is later.

If you’re enrolling in Medicare Advantage (Part C):

- If you want to enroll when you turn 65, you should sign up in the three months before turning 65.

- If you have employer (working, retiree or COBRA) or union coverage and want to delay enrolling, you’ll qualify for a special enrollment period that lasts two months after you leave that coverage.

- If you miss those windows and don’t otherwise qualify for a special enrollment period, you’ll be able to sign up during the annual Medicare Open Enrollment Period (Oct. 15 – Dec. 7).

Determine which path of Medicare (Original or Advantage) you want to choose

If you don’t have additional coverage (such as retiree insurance through a former employer), we recommend you supplement Original Medicare with a Medigap policy or opt for Medicare Advantage. There are many differences between Original Medicare and Medicare Advantage and no perfect answer as to which is best for everyone. As you think through what’s most important to you, make sure you’re considering not just your health today but how that might change as you age. It can be difficult to get more comprehensive coverage once you’ve opted into a less comprehensive option.

| Original Medicare: A, B, D, Medigap | Medicare Advantage: C |

| Have to buy multiple policies | Largely bundled into one policy |

| Less ongoing review required (don’t need to revisit your supplemental plan if you’re happy with the coverage; should revisit Part D annually) | More ongoing review required (need to revisit Advantage plan selection annually) |

| Less restrictive networks2 | More restrictive networks |

| Generally higher premiums | Generally lower premiums |

| Less restrictive coverage | May require pre-authorizations for certain services |

| Generally lower cost sharing | Generally higher cost sharing |

| No extra benefits | May include extra benefits such as dental, vision and hearing |

| Generally more ability to customize prescription drug coverage | Generally less ability to customize prescription drug coverage |

The above table outlines the numerous differences between Original Medicare, when combined with Part D and a Medigap plan, and Medicare Advantage.

Determine which plans/policies within that path you want enroll in

If you’re enrolling in Original Medicare:

- Choose a Part D plan by searching plans at medicare.gov/plan-compare.

- Pick a Medigap plan (which letter plan best meets your needs). For new enrollees, we generally recommend starting with Plan G (the most comprehensive plan for new enrollees) and adjusting if it’s unavailable, unaffordable or you prefer a different plan type.

- Once you've decided on a letter, pick a Medigap policy (which insurance company will provide that plan) by searching policies at medicare.gov/medigap-supplemental-insurance-plans.

If you’re enrolling in Medicare Advantage (Part C):

- Keep in mind that while Medicare Advantage replaces the coverage in Parts A and B, you still must enroll (and stay enrolled) in Parts A and B to sign up for a Medicare Advantage plan.

- Most Medicare Advantage plans include prescription coverage. If you don’t otherwise qualify for prescription coverage, we recommend selecting a plan that includes it.

- Be aware there is significant variation in coverage and costs among Medicare Advantage plans.

If contributing to an HSA, understand how Medicare impacts eligibility

Once you receive coverage from any part of Medicare, you’ll no longer be eligible to contribute to an HSA. Consult with a tax professional to determine the amount you can contribute in the year (or year before) you sign up for Medicare.

Use your enrollment windows to enroll in the different parts of Medicare

Parts A and B:

If you won’t be enrolled automatically, you’ll sign up for Parts A and B through the Social Security Administration.

If you're enrolling in Part D and Medigap:

To sign up for Part D and Medigap, you’ll apply with the respective insurance company offering the plan of your choice. If you’re using a Medicare agent/broker, they should help with this process.

If you’re enrolling in Medicare Advantage (Part C):

To sign up, you’ll apply with the insurance company offering the plan of your choice. If you’re using a Medicare agent/broker, they should help with this process.

Meagan Dow

Meagan Dow is a senior strategist on the Advice & Planning Research team at Edward Jones. The Advice & Planning Research team develops and communicates advice and guidance for financial planning needs, including retirement, healthcare, preparing for the unexpected and leaving a legacy. Meagan has over 15 years of financial services and investment experience. She is a contributor to the Edward Jones Perspective newsletter and has been quoted in various publications.

Important information:

This content is intended as educational only and should not be relied on for other than broadly informational purposes. The information has been prepared from sources and data we believe to be reliable, but we make no guarantee to its accuracy or completeness.

1 Residents of Puerto Rico are not automatically enrolled in Part B; they must apply.

2 While most Medigap plans cover any provider that accepts Medicare, there are Medicare SELECT Medigap plans in some states that require you to use in-network hospitals and doctors to be eligible for full insurance benefits, except in an emergency.