Facundo Abraham, CFP®

Analyst, Advice & Planning

Whether it’s a large-scale natural disaster or a smaller incident (like a fallen tree or burst pipe), dealing with property damage can be overwhelming. From finding contractors and replacing belongings to navigating insurance, decisions (and costs) can quickly pile up. If your home has been damaged and you’re unsure what to do next, these steps can help begin your recovery.

Ensure your family is safe

Start by making sure your family’s basic needs are covered. This can range from securing food or dealing with a power outage to finding temporary housing or ensuring access to medical care.

Lean on family, friends or neighbors who can support you. Local charities and volunteer organizations can also help cover some needs such as food and clothing.

Hit by a natural disaster? Where to get help

Your city/county will likely create a centralized webpage with key resources and updates (e.g., food banks, water advisories, utilities restoration plans). Your state emergency management agency’s and FEMA’s websites (for federally declared disasters) might also publish important information and links to local resources. You could also follow local agencies and other trusted social media accounts for timely updates.

Determine whether your insurance can help

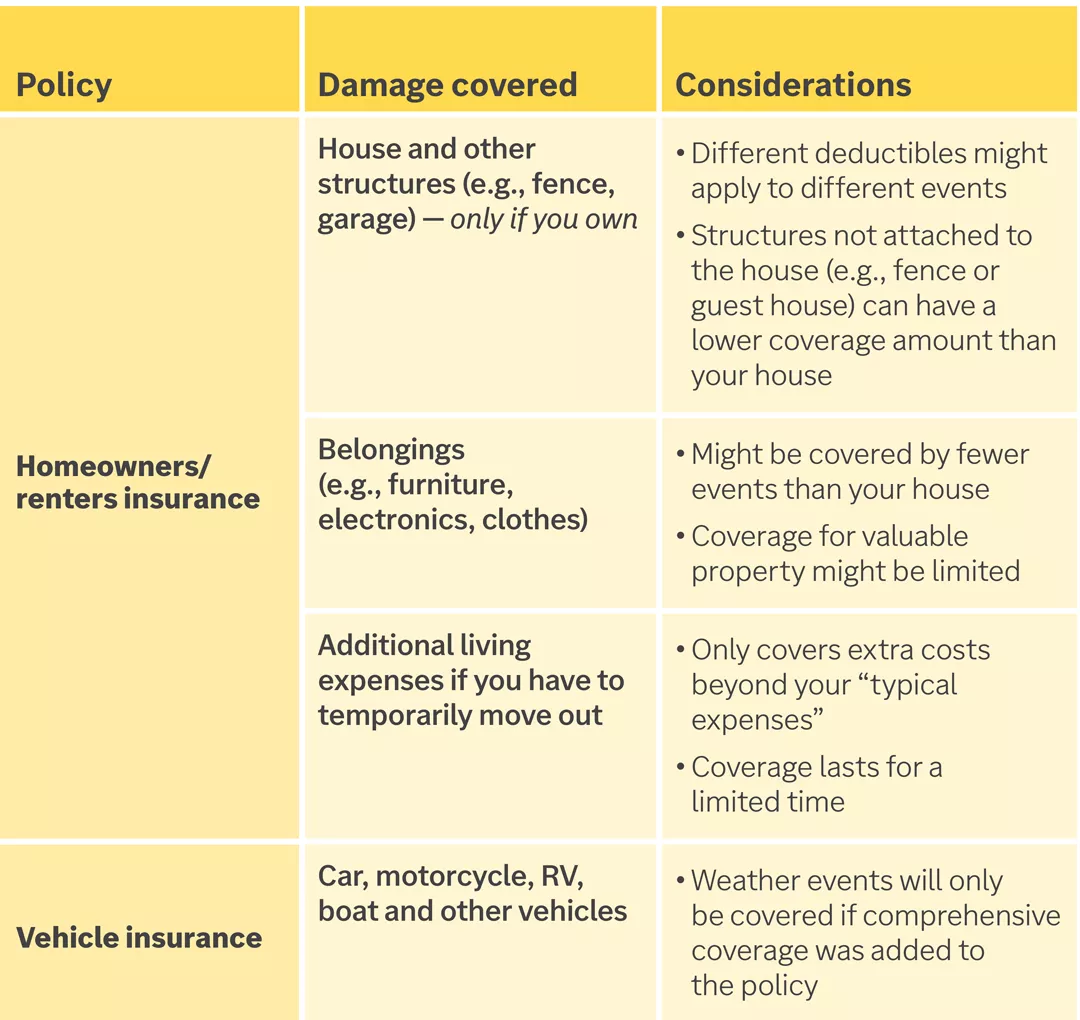

Understand whether losses may be covered by your homeowners/renters and vehicle insurance. The chart below provides an overview of what these policies can help pay for. If you need assistance reviewing your policy, your insurance agent or broker can help.

Keep in mind that your insurance will only pay for damages caused by events that are specifically covered, and some policies are more comprehensive than others. Some disasters such as flooding or earthquakes are never covered by standard policies. For these events, insurance will only pay if you bought a separate policy or add-on.

If you conclude your insurance can cover part of the costs, here are some tips to file a claim:

- Decide if making a claim is actually worth it. Because your premiums might go up, it might not make sense to do so if you expect to receive a small payout.

- Document everything. Thorough documentation can help support your claim and expedite payments.

- Contact your insurance as soon as possible. If the event is widespread, your insurance might need to process multiple claims.

- Review the payout before accepting. If you aren’t satisfied with the amount offered, you can typically dispute your insurance’s settlement offer.

Government assistance during natural disasters

FEMA and other federal aid programs

Federal agencies might provide assistance during federally declared disasters. For example, FEMA may provide money to help rebuild/repair your home and cover other disaster-related expenses. Other types of federal assistance can include SBA disaster loans (even if you aren’t a business owner) or IRS tax relief. For more information on federal assistance options, visit www.disasterassistance.gov.

State aid programs

While not all do, some states manage their own disaster relief programs (such as providing monetary aid or tax benefits). Unlike federal aid, this type of assistance might be available even in non–federally declared natural disasters.

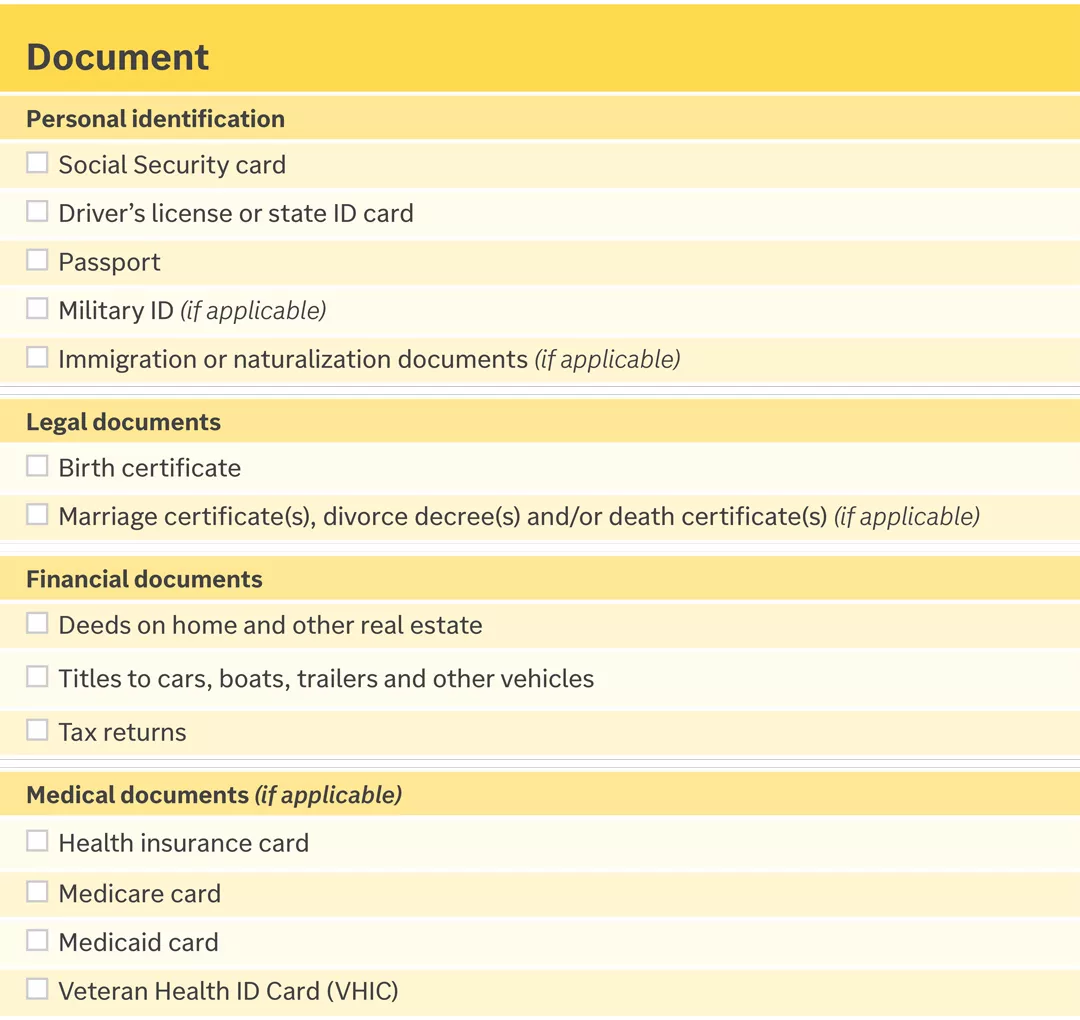

Replace lost documents

If your home gets damaged, important documents might get lost or ruined. Here’s a list of physical documents you might need to replace.

For more information on how to replace these documents, visit www.fema.gov/disaster/recover/replacing-vital-documents and www.usa.gov/request-documents.

Decide how you’ll pay for uncovered costs

Once you know what your insurance and any financial aid will cover, determine your out-of-pocket costs and how you’ll pay for them.

Start with any excess cash (e.g., from a checking account or uninvested cash in taxable investment accounts) and then use emergency savings. If that’s not enough, you’ll have to look into other options, such as using taxable investments, taking out a private loan, tapping into retirement accounts or life insurance policies, or receiving support from loved ones. Your financial advisor can help put together a plan to cover costs.

Explore assistance programs

Companies you make regular payments to (e.g., mortgage, credit cards, auto lender, utilities) may offer temporary relief after a hardship. Make sure you understand any downsides (such as being reported to a credit agency) before agreeing to anything.

During natural disasters, some companies can proactively provide financial relief to customers in the affected area. For example, mortgage lenders may temporarily suspend payments without late fees or negative credit reporting. Or utility companies might void late fees and suspend disconnections. You might also want to check whether your employer has any resources to assist employees.

Beware of scams

Scammers often take advantage of natural disasters to spread misinformation and prey on vulnerable individuals. They may pose as FEMA or disaster workers, charities, lenders or contractors. Common scams include third parties asking for money to help with aid or loan payments, individuals posing as government officials to get personal information, price gouging and fake donation campaigns.

Damage to your home can be stressful and may create unexpected financial challenges. But by having a clear plan and working closely with your Edward Jones financial advisor, you can start regaining your financial footing and move forward with greater confidence.

Money and Meaning: Understanding Financial Fulfillment

What do Americans really think about their finances today? Discover what our 2026 Gallup research reveals about how values and emotions shape our relationship with money.