3 reasons we don't see a credible threat to U.S. dollar leadership

Angelo Kourkafas,CFA

Mona Mahajan

U.S. economic growth has proved resilient despite aggressive Federal Reserve interest rate hikes in 2023. Strong growth and higher U.S. interest rates have led to the U.S. dollar index hovering toward the high end of its 20-year range.* But there have been headlines around the BRIC economies (Brazil, Russia, India, China) seeking to create a competing currency and calling for de-dollarization, particularly in oil and commodity trading.

While headlines around the collapse of the dollar emerge every so often, we continue to see the U.S. dollar maintaining its role as the preeminent reserve currency to the world. Some marginal declines in dollar trade could occur. But an outright demise of the dollar does not seem credible for three key reasons:

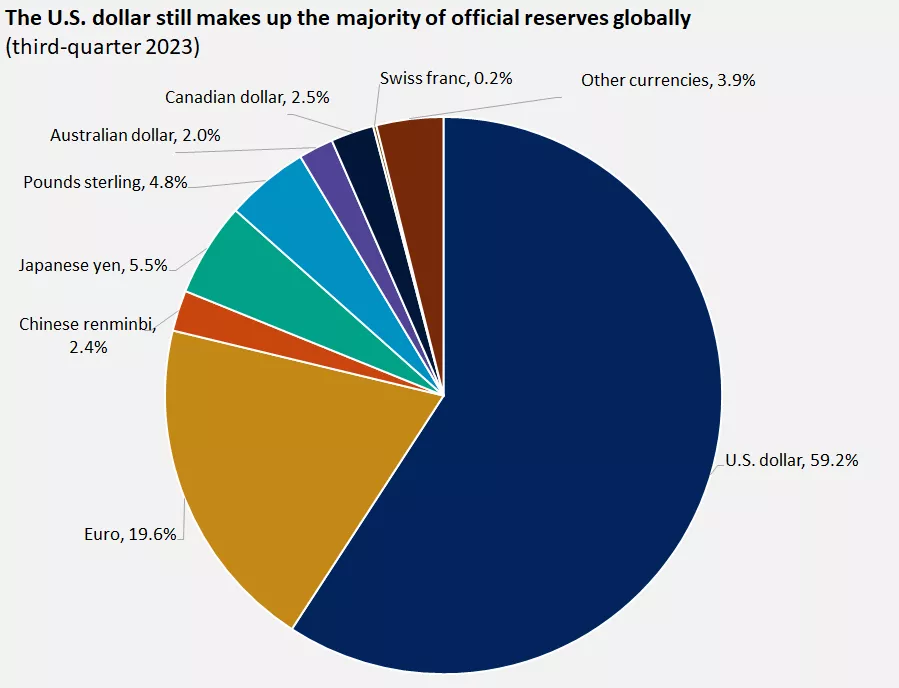

- The U.S. dollar still accounts for the majority of global reserves.

The U.S. dollar dominates foreign exchange reserves, which are assets held by global central banks in foreign currencies. These reserves are often used for trade payments or to support a currency if needed.

The percent of reserves held in U.S. dollars has moderated over the past few decades, as the U.S. economy accounts for a somewhat smaller share of global activity. However, the dollar remains the most held currency by far, comprising nearly 60% of global reserves. The euro, which is the next largest currency held in reserves, makes up about 20% of reserves.

Beyond these two currencies, the remaining currency reserves are relatively small in comparison. For example, the Chinese renminbi makes up only 2.4% of global reserves as of 2023.

This graphic highlights that the U.S. dollar is still the dominant reserve bank currency globally.

This graphic highlights that the U.S. dollar is still the dominant reserve bank currency globally.

- Global trade, including oil trade, is still largely conducted in dollars.

The Fed estimates that between 1999 and 2019, the dollar accounted for 96% of trades in North America, 74% in the Asia-Pacific region, and 79% for the rest of the world. The only region where trade was not dominated by the U.S. dollar was Europe, where the euro remained the preferred trade currency.

In addition, global oil trade, which accounts for about 6% of overall trade, is still largely conducted in U.S. dollars. While the dollar may become less of a force here, this sector remains a relatively small part of overall trade and may still use the U.S. dollar in some transactions.

- The U.S. dollar is backed by deep, liquid and regulated financial markets.

Perhaps a key reason the U.S. dollar has been the dominant currency globally is the strength and stability of the U.S. economy, as well as the deep and liquid financial markets the U.S. offers. The U.S. has by far the largest bond markets and stock markets globally. Importantly, the financial markets are highly regulated and offer borrowers and lenders access to a large set of counterparties. Overall, the U.S. is still the world’s largest economy with the deepest capital markets.

There are no realistic alternatives to replace the dollar anytime soon. The euro has faced political risk in the past, and the renminbi has significant capital flow restrictions from the Chinese government. These factors have allowed the U.S. dollar to maintain its dominant position in international trade and finance. In our view, the dollar will continue to do so for the foreseeable future.

Bottom line: While headlines around the U.S. dollar may raise questions or concerns for investors, we continue to see no credible threat to its leadership position globally. The dollar’s value may fluctuate relative to other currencies, driven by factors such as central bank interest rate policy, inflation regime and economic growth. But these are within the norm of financial market volatility.

During times of turbulence, such as with the pandemic or more recent inflation concerns, we have seen investors move foreign currency into the U.S. dollar as a flight to safety. This points to continued investor confidence in the stability of the dollar into the future.

Action for investors

We would not recommend any portfolio shifts based on fears around the U.S. dollar. But we continue to recommend investors consider diversifying their portfolios with exposure to markets and currencies outside the U.S. This includes international equities and bonds, and sectors with global exposure such as industrials and materials. All of these could provide diversification to U.S. dollar exposure.

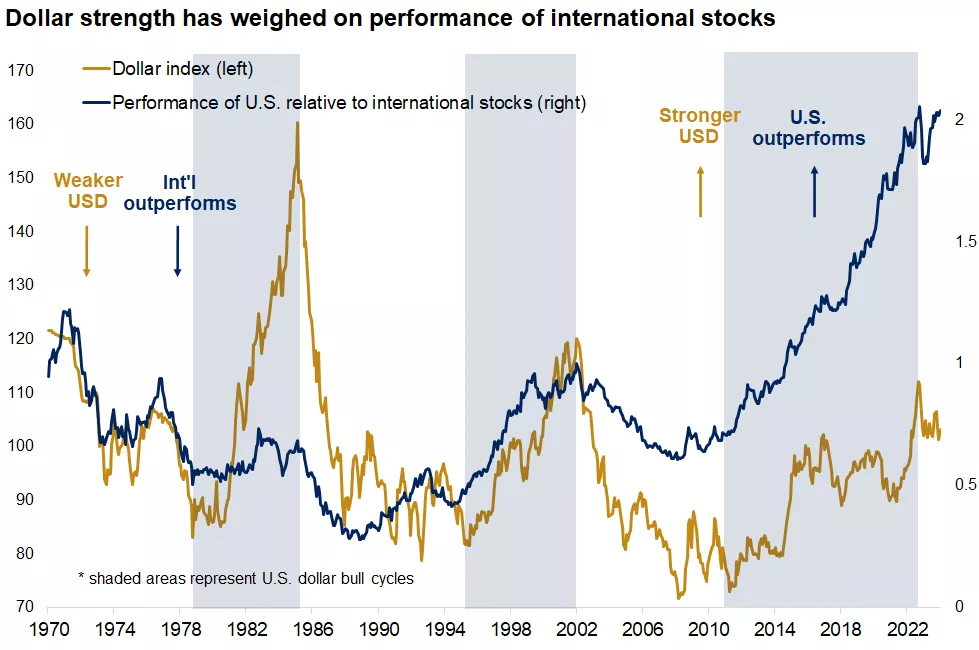

Historically, international equities tend to perform well when the dollar is weaker against other currencies. Conversely, U.S. investments typically outperform when the dollar is stronger, as the chart below illustrates. The rise in the dollar over the past decade has weighed on international returns, but even a modest shift lower in the dollar could be a catalyst for improved relative returns. Therefore, an appropriate international allocation is likely to benefit from any dollar softness, which could occur as central bank policies diverge or global growth rebounds.

In 2022 and 2023, for example, the Fed raised interest rates earlier and more aggressively than most global central banks, putting upward pressure on the U.S. dollar. But with inflation moderating in the U.S., the Fed has paused rate hikes and, in our view, will pivot to rate cuts later in 2024. If the Fed cuts rates more aggressively than other central banks, this could put downward pressure on the dollar.

More broadly, international equities (as measured by the MSCI World Ex USA) rose over 15% in 2023, yet still trade at a significant discount to U.S. equities. This suggests there is more room for global indexes to continue to perform relatively well, and a potential softening of the U.S dollar may support this position.

We recommend you work with your financial advisor to help ensure your portfolio is adequately diversified across markets and currencies, according to your personal financial goals and risk preference.

This chart shows the recent strengthening of the dollar, which has been a headwind to international returns.

This chart shows the recent strengthening of the dollar, which has been a headwind to international returns.

*Source: FactSet

This is for informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.

Investors should understand the risks involved in owning investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates, and investors can lose some or all of their principal.

Past performance does not guarantee future results.

Market indexes are unmanaged, cannot be invested into directly and are not meant to depict an actual investment.

Diversification does not guarantee a profit or protect against loss in declining markets.

Systematic investing does not guarantee a profit or protect against loss. Investors should consider their willingness to keep investing when share prices are declining.

Dividends may be increased, decreased or eliminated at any time without notice.

Special risks are inherent in international investing, including those related to currency fluctuations and foreign political and economic events.